Written Commentary

OPENING COMMENTS

Macroeconomics:

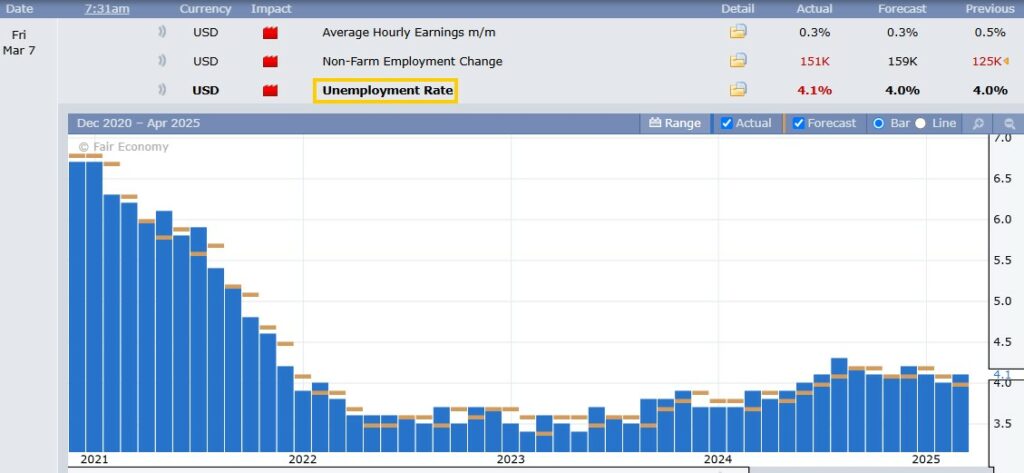

Today’s job report was not as bad as some had feared. +151K Jobs were added in February, just -8K less than estimate. December’s added jobs were revised up by +16K and January revised down by -18K for a net adjustment of -2K jobs. Crude oil hit 21 month lows on Wednesday and is still sitting below $68/barrel. Wednesday’s crude inventory report showed stocks at a 7-month high. Crude oil values are feeling pressure from tariff news, lack of energy demand and a large global supply.

Ag Fundamentals:

China has announced tariffs against US agricultural products as high as 15%, effective on March 10th. Specific agriculture products mentioned were chicken, pork, soy, and beef. The US dollar filled the gap left back on November 5th (gap:103.5-103.8) by dropping down to 103.43 overnight. The dollar’s weakness has only been able to generate a small response from the commodity market. The ratio between overall commodity values and the Weighted US dollar Index (+120) has widened to a spread more far-reaching than during the early 2000s tech bubble. Looking at the soybean meal chart, you could identify a double bottom at $292/ton. Managed money has the largest short in meal in the soy complex, but once South America passed the 50% harvested mark, a more focused Chinese business tightens Argentina’s balance sheet, the US farmer plants more than 2 million less acres then we could see fund cover shorts and meal rally. The COT report this afternoon is expected to show managed money shift their soybean position from long to short, a nearly -30K contract change). May wheat chart has presented support at $540 with lows from early January helping to create a floor.

Unemployment Rate rose +0.1% to 4.1% while expectations were for it to remain unchanged at 4.0%.

Payrolls rose by 151K in February, which was just 7K jobs less than expected, and hourly earnings were in line with estimated +0.3%.

South America’s Soil Moisture has a couple areas that are deficient and may not receive sufficient rain for another 10 days. Southern growing areas in Argentina will get a shower in the next few days, and rains are expected in Brazil’s central regions.

EXPORT & WORLD NEWS

South Korea is in the market to buy up to 140K MT of animal feed corn in an international tender. Tunisia is also looking to buy 25K MT of corn with a deadline of March 7th.

Malaysian palm oil futures were up 145 ringgit overnight, now at 4625.

Daily Trading Limits: Corn $0.30 (expanded $0.45); Soybeans $0.85 (expanded $1.30); Minneapolis Wheat $0.60 (expanded $0.90); KC Wheat $0.40 (expanded $0.60); Chicago Wheat $0.40 (expanded $0.60)

>>Interested in more commentary by Joe Mauck? Go HERE

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.