Ontario puts a new 25% tariff on electricity going into New York, Michigan, and Minnesota. This could effect 1.5 million homes in the three states, and may cost Americans up to $400K/day. Reciprocal tariffs are still scheduled for April 2nd and this may be included in those changes.

Ag Fundamentals:

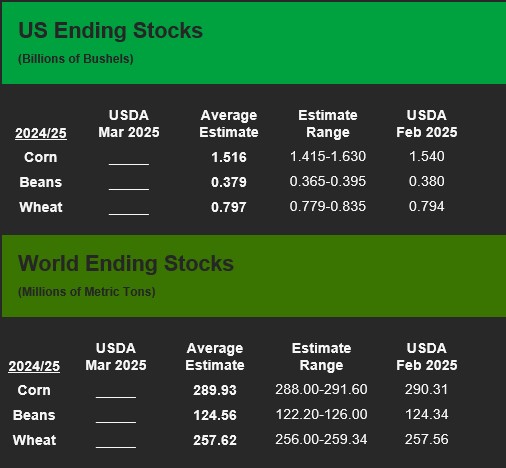

The USDA will release their World Agriculture Supply and Demand Estimates this morning at 11:00 am CST. Some of the more anticipated changes are lower Chinese corn and wheat import numbers, a drop in corn ending stocks in the US and world, and lower Argentina production numbers for corn and beans. It is difficult for the USDA to take a stance on the effects of the newest tariffs will have on US exports at this time. The US dollar is sitting on 4-month lows below 103.5 on the index, supporting commodities. Corn exports yesterday impressed, but many are not expecting USDA to revise their corn export estimate higher. Corn usage should see an improvement in demand as ethanol production has been above expectations. South American production may be the main focus today as they are now on the back half of their soybean harvest.

Weather:

Higher than normal temps are expected for much of the Midwest this week, and the wheat belt may experience high winds causing concerns for the dormant wheat crop. Wheat conditions in Kansas and Texas fell while Oklahoma has recently improved their wheat crop conditions. North/East Brazil will receive a bit more rain than previously forecasted which will help their corn crop, but may cause delays in bean harvest. Argentina is see dryer weather toward the tail end of their first soybean crop expected to start harvesting in the next couple weeks.

March WASDE Report Estimates:

The Volatility Index (VIX) is hitting highs again this morning after rallying over 80% in the last month. The 52 week high was in August last year when the Japanese yen carry trade rocked the markets here in the US. There was a second spike in mid-December too when Jerome Powell spoke at the Fed meeting stating there may not be as many cuts to interest rates in 2025. It has not been below 14 points since July 2024.

EXPORT & WORLD NEWS

The USDA’s flash sale yesterday was 195K MT of soybeans to unknown destinations, and 126K MT of corn to Japan. South Korea is looking to buy up to 138K MT of animal feed corn.

Malaysian palm oil futures were down only 11 ringgit overnight, now at 4488

>>Interested in more commentary by Joe Mauck? Go HERE

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.