Written Commentary

OPENING COMMENTS

GEOPOLITICS:

President Trump is expected to implement 25% tariffs on all steel and aluminum imports starting today. both Canada and Mexico will feel the effects of this change. Canada makes up 39% of US aluminum imports and Mexico take 7%. Regarding steel, Canada makes up 24% of US imports and Mexico covers 15%. Indiana produces the most steel in the US followed by Ohio, Michigan, and Pennsylvania. The dollar is reacting slighting higher this morning and has consistently reacted to new tariff announcements. Trump met with Japan’s prime minister Shigeru Ishiba on Friday to discuss the potential $1 trillion investment in the United States as well as Japan’s Nippon Steel’s attempt to purchase U.S. Steel last year, which Biden blocked. The last Japanese prime minister Trump worked with was Shinzo Abe , who was assassinated in 2022. Also mentioned was Ishiba’s hope that Trump would continue to have a good relationship with North Korea’s Kim Jong Un.

MACROECONOMICS:

The US unemployment rate came in better than expected on Friday, now at 4.0% (lowest unemployment since June 2024). January’s non farm employment change came in -26K jobs cooler than estimates at +143K new jobs. December non-farm employment was also revised +51K jobs higher so net increase of +25K jobs. The dollar is slightly stronger this morning. We will have some important inflation data coming out on Wednesday this week (CPI and Core CPI).

AG FUNDAMENTALS:

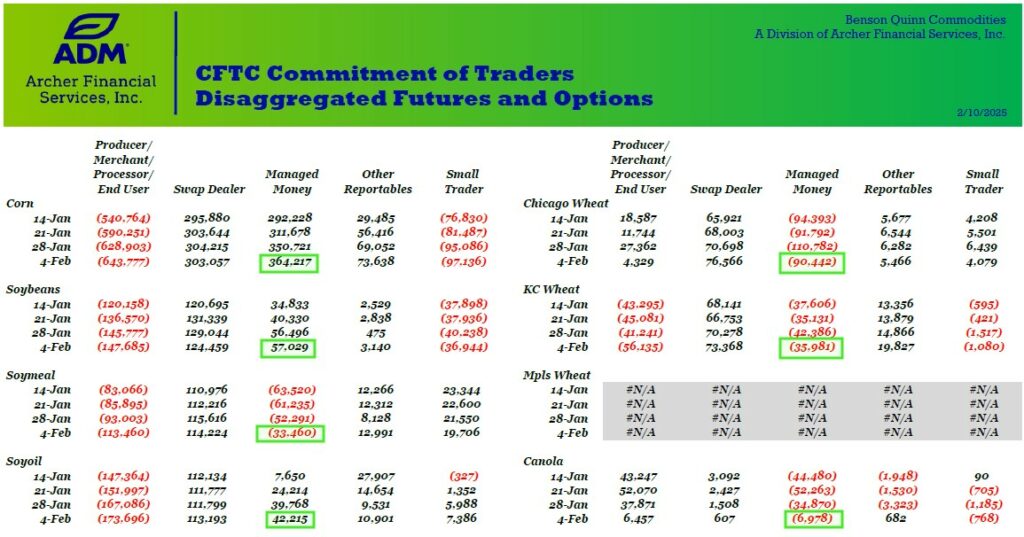

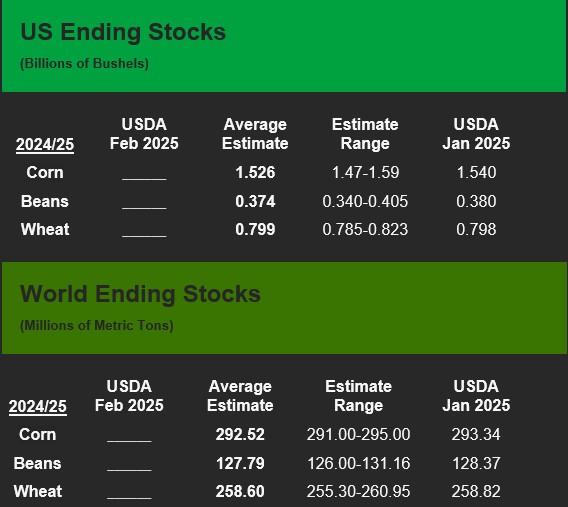

Funds now hold the longest corn position we have seen since 2022. Managed Money is holding over 364K contracts long corn as of Friday’s commitment of traders report. South American weather continues to be the main focus aside from tomorrow’s USDA WASDE report. February WASDE reports are not typically huge market movers, but most expect ending stock numbers to be cut on both corn and beans. The changes to global ending stocks will mostly be effected by any cuts to Argentina’s production estimates. China has been quiet since returning from their holiday week and retaliating to Trumps 10% tariffs. Their corn and wheat stocks are high, but US exporters are looking for new Chinese business between now and March.

WEATHER:

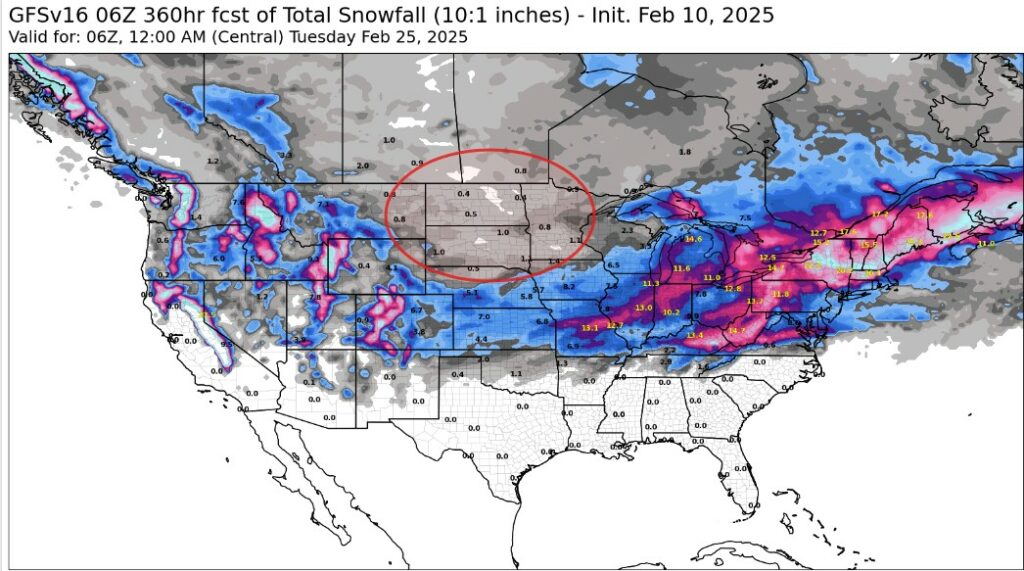

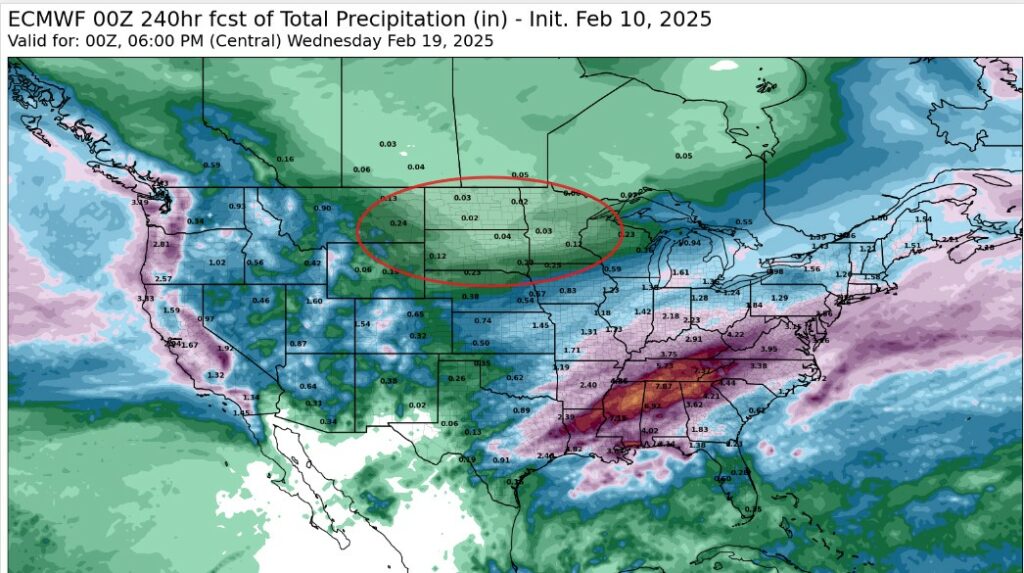

Natural gas is working back higher over the week due to an increased chance of a polar surge hitting the US by the end of February. In the next 3-5 days temps across the wheat belt are expected to be below normal, with minimum temps in Nebraska and Kansas reaching as low as -7 degrees. Snow storms will start his week across Kentucky then a large stretch of the central Midwest will get hit with 3-4 inches between Wednesday and the weekend. Then another round of snow will run from central Missouri through central Illinois, hitting northern Indiana, Michigan and Ohio. The Northeast region of the US will get the most snow in the next 14 days. Additionally the Southeast will receive heavy rains in the next 10 days, spreading mostly across northern Mississippi, northern Alabama, and eastern Tennessee.

The Commitment of Trader Disaggregated Report shows managed money either increasing their length or covering shorts in all commodities.

Ending Stock Estimates for Tomorrow’s WASDE Report

Next 14 days of Snowfall has alot of activity in the I-states and Northeastern US, but lacks action in the Central North where most of the drought concerns lie.

The Next 10 days of Precipitation gives plenty of moisture to the southeast, but the North central region of the country remains dry.

EXPORT & WORLD NEWS

Private exporters reported 365K MT of corn sold to Mexico this morning. South Korea bought about 63K MT of animal feed corn to be sourced fro the US South America or South Africa. Jordan is in the market to buy up to 120K MT of milling wheat in an international tender.

Malaysian palm oil futures were up overnight 89 ringgit, now at 4593.

Daily Trading Limits: Corn $0.30 (expanded $0.45); Soybeans $0.85 (expanded $1.30); Minneapolis Wheat $0.60 (expanded $0.90); KC Wheat $0.40 (expanded $0.60); Chicago Wheat $0.40 (expanded $0.60)

>>Interested in more commentary by Joe Mauck? Go HERE

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.