Corn prices are driven by demand and news of slower than normal planting progress in South America. Cattle prices are consistently making new highs (Feb closing at 208’55 today), they were up again today and many expect prices to continue until herds are rebuilt to it’s peak in 2018. The US calf crop peaked in 2018 at 36.3 million head, compared to 33.1 million head in 2024. Aviation flew has not made a huge impact on the cattle prices, but it does highlight the importance of herd health. More mainstream discussions about what is in our food and how people are dodging medications by eating healthier, offers farmers a premium intensive to raise high quality livestock. Prices are up 18-20% year-over-year and up over 100% from 2021 values. This increase should influences businesses to puss capacities and help increase supply to the market. Nearly 40% of the corn grown in the US is used for feed and the anticipation of a herd recovery due to an increase in cattle prices should add optimism for corn demand. We have a normal report schedule this week with EIA ethanol production/stock out tomorrow alongside the Fed’s interest rate decision, and export sales on Thursday alongside unemployment claims.

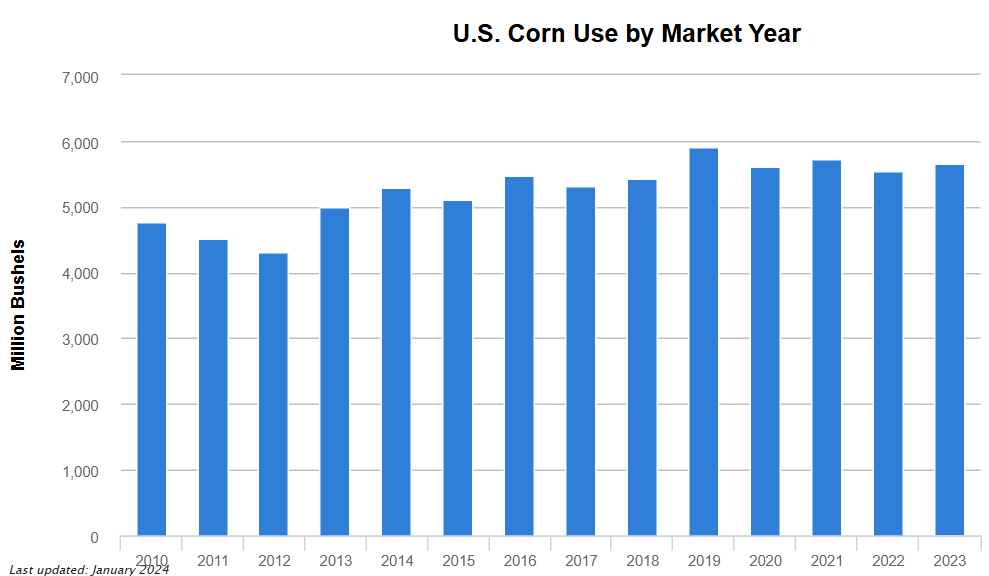

Feed and Residual Corn Use makes up for about 40% of the corn grown in the US. Cattle herds peaked in 2018 with corn usage following the increase the following year. Cattle prices continue higher, increasing the likelihood that farms will rebuild herd sizes.

Live Cattle 50-year Price Chart shows a price peak in 2014, a herd rebuild until 2018 followed by a halt in demand during the COVID pandemic. Following the 2020 COVID pandemic lows, cattle prices have charged back to new highs. Might be a good time to get into the freezer business.

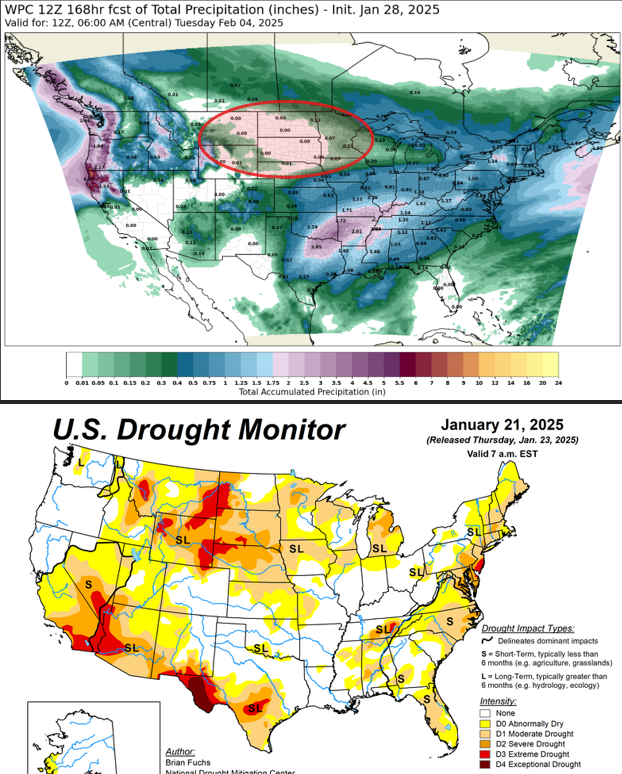

The Next 7 days of Precip and Current Drought Monitor highlight a pocket in the Dakotas and northern Nebraska that have been lacking moisture this winter.

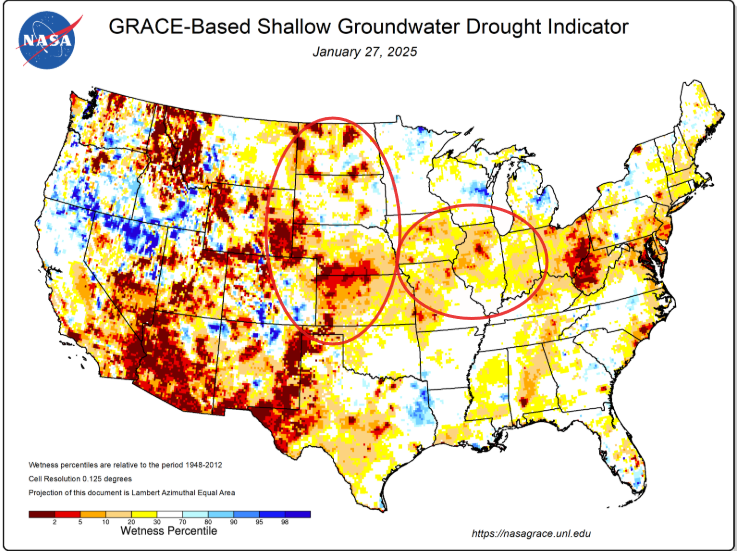

NASA’s Groundwater Drought Indicator is starting to show some concerning areas. The wheat belt is in need of a good drink before winter ends and the heart of the Midwest is also at risk of missing needed precip to replenish reserves for this coming spring.

>>Interested in more commentary by Joe Mauck? Go HERE

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.