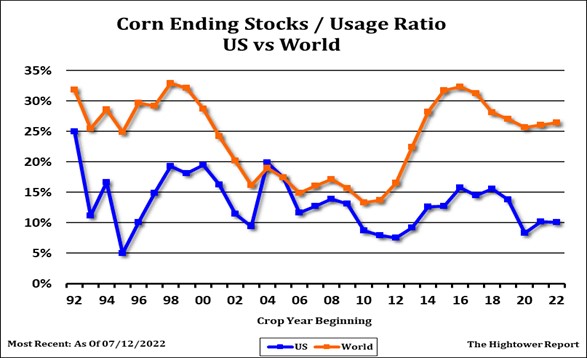

CORN

Corn futures may be also adding an US weather premium. Starting Monday, US Midwest 14 day weather forecast is warm and dry. One crop watcher dropped US yield 3.5 bpa to 173.5. They traveled through IA and MN and suggest US yield could drop to 170 if IA, NE, KS, MO, TX and OK are warm and dry over next 3 weeks. EU weather is warm and dry. Some estimate EU corn crop closer to 50 mmt than USDA 68. CU tested key resistance is near 6.32 but backed off on talk of increase Ukraine corn exports. Some feel 20 vessels of mostly corn will be shipped soon out of Odessa port. Key will be how much additional corn can be loaded and shipped. Most look for Mondays USDA corn crop rating to drop especially in US SW corn states. IA and IL crop weather and size to of CU is worth 7.00 or 5.50. CU may be trying to establish a trading range between 6.00 and 6.50 until more is known about US weather and impact on US final carryout. Assuming US harvested corn acres stay near 82.0 million and demand near 14.570, (14,865 this year)1 bpa drop in yield would drop US carryout 82 mil bu. A 7 bpa drop would drop carryout 575 mil bu or to only 895. USDA est World 2022/23 corn stocks at 312 mmt vs 312 this year. Of the total China is 204. Of the 108 left US is 37, Ukraine 12. Brazil 8 and EU near 8.5. Noon weather maps were mixed. One map added rains next week as ridge moves far enough east to allow gulf moisture to move across the Midwest. The one map that has been suggesting warm and dry Midwest weather over the next 2 weeks is still warm and dry.