SOYBEANS

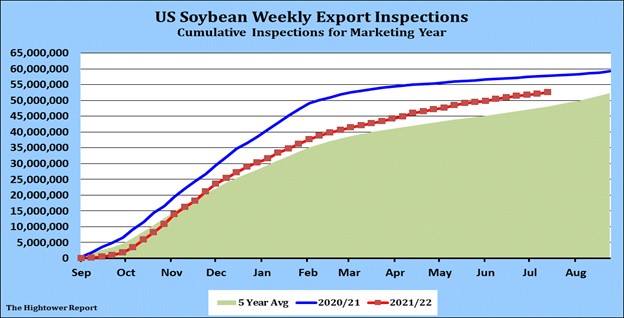

Soybeans ended higher. Weather is back in the news. Over the next few week US north and east Midwest should see normal temps but normal to below rains. SE Midwest, south plains and Delta could be warm and dry. This could raise question about corn yields in the driest area. Our weather guy could see less rain in August which could lower final soybean yields. Our weather guy put out a special report suggesting July 15- August 14, SD, NE, W IA, MO, KS, OK, TX and AR drier and warmer than normal. A wider area including IA and IL could be dry a warm Aug 15-Sep 14. Weekly US soybean exports were 13. Season to date exports were 1,930 vs 2,128 ly. Key is China demand. Trade expects US soybean crop to be 62 pct G/E vs 62 last week. SU may have found support near 13.50. Next resistance is 14.25 then 15.00. Market volatility is expected to continue until more is known about US crop, China demand and money flow. Inflation topping or recession.