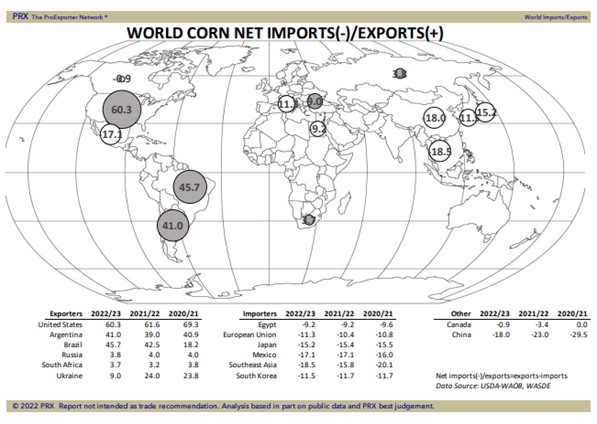

CORN

Corn futures were down sharply with CU back below 6.00. Early selling was linked to concern that this week’s US CPI data will show even higher inflation. This could force US Central Bank to increase interest rates until US is in a recession. There was also talk that tomorrow there will be a meeting in Turkey with UN, Ukraine and Russia. This to try to come up with a plan to open Ukraine grain exports. Participants are a military delegation and not diplomats. Russia is not expected to allow exports unless west sanctions are dropped and Ukraine is not expected to de-mine ports unless Russia stop attacks. There was talk of vessels heading to Ukraine port to load grain. These vessels load only 5-6,000 mt and ports can only unload 60 mt of grain per day by truck. Rail service has stopped after key bridge was bombed. Finally, noon GFS US weather turned wetter over the central Midwest over the next 7 days. Some feel the maps were overdone. USDA dropped US 2021/22 feed use 25 mil bu. This increased carryout to 1,510. USDA increased US 2022 corn crop 45 mil bu. Higher imports and higher crop resulted in an increase in carryout to 1,470. USDA increased World 2022/23 end stocks 2 mmt. USDA est Brazil 2023 corn crop at 126 mmt vs 116 this year and Argentina 55 vs 53. They est EU corn crop at 68 mmt with some closer to 62. They est World 2022/23 corn exports at 182 mmt vs 199 last year with Ukraine 9 vs 24.