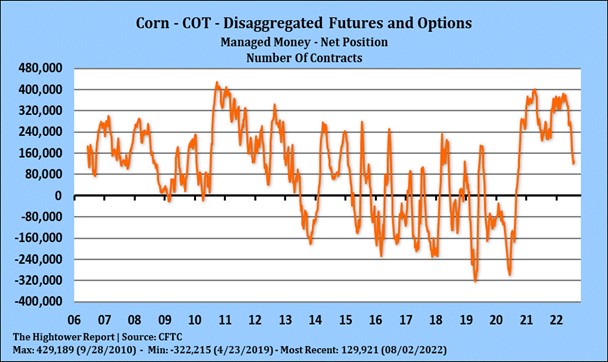

CORN

Corn futures ended slightly lower and remain in a tight range. Managed funds continue to be reluctant buyers of grains due to fear inflation will trigger US Fed to increase interest rates another 75 basis points in September after Fridays US jobs report. Funds also reluctant buyers of commodities until Crude oil chart turns higher. Weekly US corn exports were near 22 mil bu vs 35 last week. Season to date exports are 2,068 mil bu vs 2,515 ly. USDA goal is 2,450 vs 2,753 ly. Some are lowering their export estimate 50 mil bu and ethanol 40 mil bu. Key is final US 2022 corn supply and demand for US corn. EU needs corn. US prices and now a discount to Brazil. USDA reported that 105 mt of new crop US corn was sold to Italy. USDA also announced 120 mt of new crop US corn was sold to unknown rumored to be Spain. Some feel EU could imports as much as 5 mmt or 200 mil bu of US corn. This could drop US 2022/23 corn carryout below 1,300 mil bu. Italy normally buys their corn from either Ukraine or Brazil. US corn export prices are now a discount to US. First Ukraine corn export boat does now not have a home. Most of the 20 boats loaded in April, have been sold to unknown. Boat thought to be sold to Lebanon is too large to be unloaded in Lebanon. Trade est that USDA will drop US corn rating to 60 pct G/E vs 61 last week. Our weather guy is watching forecasted dryness across S/W IA, NE, KS, N MO and WC Illinois. 10 pct drop in KS, MO corn yield corn drop US corn yield 3 bpa.