Written Commentary

BONDS:

Certainly, the much stronger than expected US nonfarm payroll gain and decline in the US unemployment rate was justification for the pummeling of treasury prices last Friday. However, the treasury markets have been absorbing positive economic readings without significant weakness, and therefore today’s action might be a sign of a fundamental shift in the bond and note markets. In other words, today’s nonfarm payroll report clearly ratchets up the potential for a 75-basis point rate hike by the Fed next month, but the treasury markets now have justification to consider the ability to achieve a soft landing.

CURRENCIES:

Obviously, the much stronger than expected jump in US July nonfarm payroll readings and the downtick in the US unemployment rate provided the buying impetus in the dollar index last Friday. We suspect a shift up in the dollar combined with a large jump in US treasury yields will yield additional dollar buying week. In the near term, we expect the Pound, Canadian dollar and the euro to suffer more declines than the Swiss franc. However, going forward, the markets will be presented with a global sweep of CPI/PPI readings and those readings could be just as important to the currency markets as the US nonfarm payroll report.

The very positive US nonfarm payroll reading from last Friday likely thickened recent consolidation resistance in the euro at 1.024 with many traders potentially discouraged from the long side of the euro ahead of the German CPI reading early Wednesday morning which is expected to post a hot 0.9% month over month gain. With the breakdown/reversal on the charts last week in the Yen, the currency appears to be back under pressure from the dollar. The Yen is also being undermined by fears of a hot Japanese PPI reading on Wednesday fostering the extension of the slowing economy/rising rates conundrum. While the Pound respected the 1.20 level last week the pattern of lower highs and lower lows gives the bear camp a technical edge. The sharp failure in the Canadian dollar last Friday in the face of a disappointing Canadian jobs report and optimistic US July jobs figures, highlights Canadian dollar vulnerability.

STOCKS:

With US equities reversing course last Friday after the much better-than-expected US nonfarm payroll reading for July, it is clear the markets remain concerned that over-tightening by the Fed will trip up the US economy into recession. However, given the massive jump in jobs gained and the decline in the US unemployment rate, economic anxiety and concern for softening future earnings should be tempered which in turn should discourage massive washout days.

Dow futures at the start of this week sit just below an upside breakout following 6 days of sideways consolidation and a lack of upside momentum. While the Dow has stood up to fresh fears of another aggressive US rate hike next month, the bull camp should be emboldened by the sign of life in US economy from the monthly jobs report. Like other stock index futures, the Dow remains significantly net spec and fund short. The August 2nd Commitments of Traders report showed Dow Jones $5 Non-Commercial & Non-Reportable traders reduced their net short position by 4,153 contracts to a net short 22,931 contracts.

GOLD, SILVER & PLATINUM:

In general, October gold remains in a slightly bullish chart position with the potential for significant price volatility later this week following a series of classic global inflation readings. In retrospect, gold stood up to the significant jump in treasury yields and a strengthening in the dollar in the wake of a much stronger than expected US nonfarm payroll reading for July. However, investment interest remains bearish with gold ETF holdings on Friday posting an outflow of 86,048 ounces bringing the weekly disinvestment tally up to 383,461 ounces. While silver ETF holdings dropped by 1.1 million ounces on Friday, last week silver ETFs overall saw a net inflow of 633,577 ounces.

While the platinum market is significantly overbought from the July August rally of $135, the net spec and fund long from last Tuesday (prior to the big rally was a mere 1,762 contracts. Therefore, the market might not be as vulnerable to Friday’s reversal on the charts. Platinum positioning in the Commitments of Traders for the week ending August 2nd showed Managed Money traders reduced their net short position by 4,082 contracts to a net short 12,120 contracts. Non-Commercial & Non-Reportable traders went from a net short to a net long position of 1,762 contracts after net buying 1,973 contracts. As in other precious metal markets, platinum ETF holdings continue to flow out, with ETF holdings Friday down 7,530 ounces, down 14,754 ounces last week and down 11% year-to-date.

Like the platinum market, the palladium market has seen consistent outflows from palladium ETF holdings with holdings last week declining by 829 ounces and holdings year-to-date down 14%. The August 2nd Commitments of Traders report showed Palladium Managed Money traders net bought 852 contracts and are now net short 1,452 contracts. Non-Commercial & Non-Reportable traders are net short 2,742 contracts after net buying 1,152 contracts.

COPPER:

While the September copper contract at the start of this week g has not taken out last Friday’s recovery bounce highs, prices look to become entrenched above $3.49 off a slightly favorable supply and demand mix. The copper market appeared to shift back into the March through July downtrend following last week’s high, but recovered from news that Chinese July copper imports jumped with buyers reportedly drawn in by cheap pricing. Even the supply side of the Chinese copper equation is supportive following headlines last week indicating up to 200,000 tonnes of Chinese copper had “gone missing”.

ENERGY COMPLEX:

While July Chinese oil imports of crude oil ticked up, that bounce left imports near 4-year lows last month with Chinese oil refiners last month drawing some supply from domestic reserves. The charts in crude oil remain bearish with the recent pattern of lower highs extended and prices likely to make a lower low early this week. In retrospect, the US nonfarm payroll reading blowout (on the upside), Nigerian exports disrupted, a general global risk on vibe from equities and residual bullish oil views from Goldman Sachs, the market does have some fundamental support.

We continue to see the ULSD market as the market most likely to bottom before other portions of the petroleum complex. However, we also expect the ULSD market to be weaker than other segments to start the trading week. I

With the natural gas market managing to consolidate and trade sideways last week in the face of a tempering of US ultrahigh temperatures, a bigger than expected EIA injection to storage and ongoing global recession talk, the $8.00 level could “eventually” become fundamental support/value. In the near term, an extension of extremely hot temperatures in the northwest of Europe should temper the downside corrective tilt to start the trading week.

BEANS:

The 6-10 and 8-14 day forecast models for the last several weeks have shown above to much above normal temperatures and below normal precipitation. However, most areas of the Midwest have received good rain amounts with scattered just-in-time rain coverage. The current weather set up is similar, with a warmer and mostly drier longer-term outlook, but the 1-5 day forecast models show more rain coverage for southern Illinois and India after the northern and eastern quadrant of Iowa, southern Minnesota, Wisconsin and northern Indiana received good weekend rains. Some areas of southern and western Iowa, Nebraska, Dakotas and northern Missouri have not received much in the way of rain in the last two weeks, but dry spots seems limited, and traders seem to believe yield might come in close to the current USDA forecast.

CORN:

December corn closed higher on the session Friday and up for the third day in a row. More talk that scattered rains across the Midwest will help ease crop stress due to mostly hot weather helped to pressure. Good rains over the weekend helped to ease crop concerns. Concerns with European crop production, which traders believe will see a loss of at least 10 million tonnes, helped to support the market. A forecast for US rainfall this past weekend raised hopes for much needed moisture. Heavy rains hit the northern half of Iowa and southern Minnesota over the weekend with many area receiving 1.5 to 3 inches.

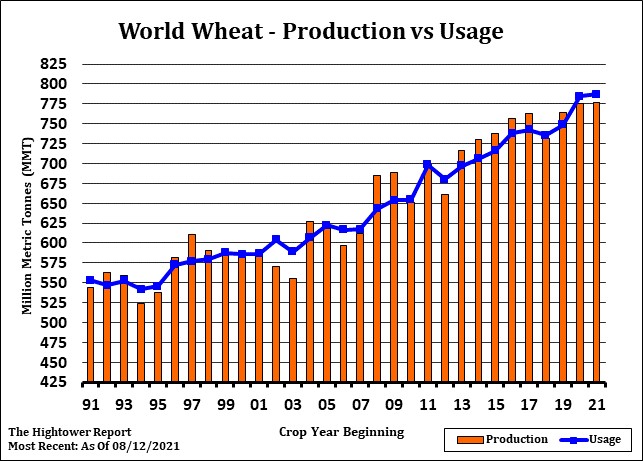

WHEAT:

September wheat closed lower on the session Friday after choppy and two-sided trade early in the day, and this left the market with a loss of 32 cents for the week. Talk of grain moving out of the Black Sea for export plus a surge higher in the US dollar plus continued talk of good weather for spring wheat crops in the US and in Canada helped to pressure. South Korea was a noted buyer of near 120,000 tonnes of animal feed wheat expected to be sourced from Australia. For the week, Chicago wheat was down 4%, KC down 2.9% and Minneapolis wheat down 2%.

India could scrap a 40% duty on wheat imports and cap the amount of stocks traders can hold to try to dampen record high domestic prices in the world’s second biggest producer, government and trade officials told Reuters on Monday. Domestic wheat prices ended last week at a record 24,000 rupees ($301.57) per tonne, having risen 14% from lows struck after the government surprised markets on May 14 by banning exports, ending hopes that India could fill the market gap left by the missing Ukraine grain.

HOGS:

October hogs closed moderately higher on the session Friday and the buying pushed the market up to the highest level since April 22. The market experienced follow-through technical buying even with a sluggish pork market. October hogs collapsed Thursday and held key support. This is impressive technical action on decent volume and with uptrending open interest which pushed up to the highest level since April. The short term trend remains up and the rise in open interest is a positive force. The USDA pork cutout released after the close Friday came in at $124.03, up 90 cents from Thursday but down from $125.81 the previous week. The CME Lean Hog Index as of August 3 was 121.61, up from 120.94 the previous session and 120.58 the previous week. The USDA estimated hog slaughter came in at 460,000 head Friday and 61,000 head for Saturday. This brought the total for last week to 2.340 million head, up from 2.291 million the previous week and 2.327 million a year ago.

CATTLE:

The cattle market remains in a solid uptrend as a significant decline in supply for the 4th quarter and the first half of 2023 has provided underlying support. October cattle closed higher on the session Friday and the buying pushed the market up to the highest level since May 4. Cash cattle inched higher last week but nothing too impressive, and beef prices have pushed lower on the week. Cash live cattle traded in light volume on Friday. The 5-day, 5-area weighted average price last week was 140.28, up from 139.82 the previous week. The USDA boxed beef cutout was down $1.18 at mid-session Friday and closed $1.66 lower at $264.62. This was down from $269.24 the previous week and was the lowest the cutout had been since July 4. However, the technical action remains impressive even with the premium of futures to the cash.

COCOA:

Cocoa prices saw little upside follow-through from last Thursday’s outside-day higher close as they continue to have trouble sustaining a recovery move. While the market has extended a choppy price pattern since late June, cocoa has seen bullish supply developments that can help prices regain upside momentum soon. December cocoa found early support, but turned back to the downside at midsession as it finished Friday’s trading session with a sizable loss. For the week, December cocoa finished with a loss of 32 points (down 1.3%) which was a second negative weekly result over the past 3 weeks.

COFFEE:

While coffee is a “staple” for many consumers around the globe, concern over out-of-home consumption continues to put brakes on the market’s upside momentum. Although it may see downside follow-through early this week, coffee continues to have bullish supply developments that can provide underlying support to the market. December coffee found initial support, and then came under significant pressure and could not sustain a late recovery move as they finished Friday’s outside-day trading session with a sizable loss. For the week, December coffee finished with a loss of 7.40 cents (down 3.5%) which broke a 2-week winning streak and was a negative weekly reversal from Monday’s 4-week high.

COTTON:

December cotton closed higher last Friday after trading to the highest level in a week. The market approached the July 29th high of 97.65 before backing off. More talk of the precarious situation for the Texas crop lent support after the weekly Drought Monitor showed no improvement in west Texas last week. The 1-5 day forecast calls for some rainfall in the Texas Panhandle, but very little in other parts of west Texas. The 6-10 and 8-14 day forecasts call for above normal temperatures and normal or below normal chances of rain in west Texas and the Panhandle.

SUGAR:

The sugar market saw chaotic price action last month as carryover pressure from sluggish crude oil and gasoline prices weakened sugar prices since mid-June. In contrast, sugar prices have started out August with renewed strength as the market seems to have the supply fundamentals to fuel a recovery move. October sugar continued to build on early support throughout the day as it finished Friday’s trading session with a sizable gain. For the week, October sugar finished with a gain of 40 ticks (up 2.3%) which broke a 2-week losing streak and was a positive weekly reversal from Monday’s 11 1/2 month low.

Please contact us at 1.877.690.7303 or via email at sales@admis.com for any questions or comments on this report or would like more information about ADMIS research.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.