Written Commentary

MORNING COMMENTS

Geopolitics:

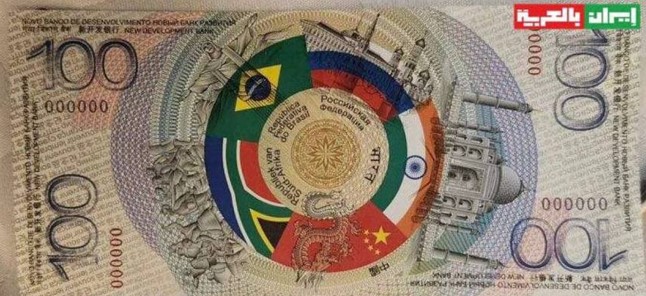

There is a picture of Russia’s President Putin holding a bank note handed to him at the BRICS summit in Kazan Russia yesterday. The note has an image of all the flags that make up the BRICS coalition (Brazil, Russia, India, China, and South Africa). I have not found any credible sources to confirm the movement towards a new currency, but it seems that it is a topic of discussion amongst leaders. Leaders like China’s President Xi Jinping urging the other present to strengthen their financial ties.

Macroeconomics:

Unemployment claims came in below expectations this morning. The trade expected 243K new claims, and 227K were reported. Thousands of Walgreens and Seven Eleven locations announced future closings, there is still a hit to areas effected by both Helene and Milton, and Boeing strike is going on 5 weeks. Existing home sales were 40K less than expected last month. This morning’s report showed 3.84M existing homes were sold last month which is -44% down from the peak of COVID property grab in November 2020 (6.85M).

Ag Fundamentals:

Export data this morning was favorable for both corn and beans. Corn data reporting 300K MT above the high end of the estimate range at 3.602M MT sales last week. December corn board is now trading above the 100-day moving average. The Dec corn high since July is 434’2 set in early October. The 200-day moving average is at $4.45 which would be a big hurdle to jump. It’s possible we test those levels if we continue to see export sales and ethanol production numbers beat expectations. The SX/SF (Nov/Jan) bean spread continues to firm this morning as domestic demand clashes with a low board price and a tight gripped farmer.

Weather:

Showers are expected to cross Iowa, Minnesota, Wisconsin and northern Illinois between now and Friday. The US growing regions have seen one of the driest September/October on record. Hoping these rains are not soaked up and evaporate too quickly. The river system and the moisture across the corn belt could use more.

Existing Home Sales are as low as 1995 on the annual basis. Below is a monthly chart and it shows the difference between today’s report and previous highs.

Image (not confirmed) of the BRICS Note that was presented to Putin at the BRICS summit. The leaders of many countries attending the summit in Russia this week expressed the need to move away from the US dollar and reinvent the global financial architecture. This would effect exports in the US and around the world.

Weekly Export Sales

|

Export & World News

The US announced 389K MT of soybeans sold to both China and unknown destinations. US Corn exports for the US have been better than expected for the last 2 weeks. Indonesia is looking to buy up to 340K MT of rice. Bangladesh is also in the market fro 50K MT of rice.

Malaysian palm oil futures were up 116 ringgit overnight, at 4602.

>>Interested in more commentary by Joe Mauck? Go HERE

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.