Written Commentary

OPENING COMMENTS

Geopolitics:

The European Commission President Ursula von der Leyen announced 25% counter tariffs on $28 billion worth of mostly steel and aluminum. The duties also include other industrial and agriculture products – poultry, beef, seafood, nuts, eggs, sugar and vegetables. . This will go into effect on April 1st (not a joke). Corn may fall under the April 1st round of EU tariffs, but soybeans will be included in the second round beginning April 13th.

Macroeconomics:

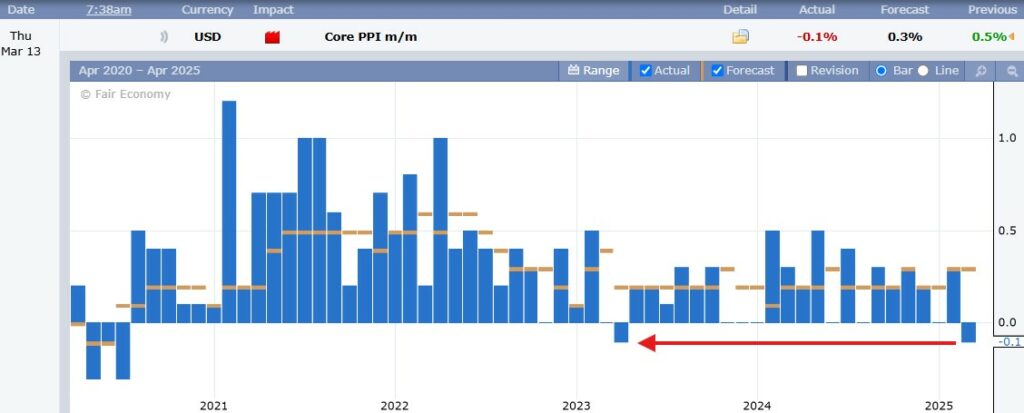

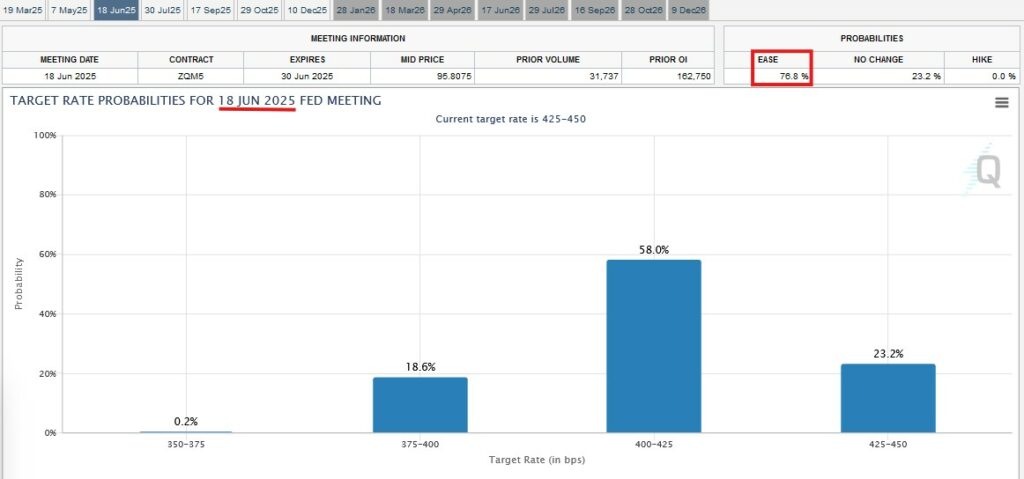

The CPI and PPI reports both offered positive news on inflation for the Month of February. Some look at the recent volatility as a huge opportunity to jump into the market while people are fearful. Warren Buffet famously said, “be fearful when others are greedy, and greedy when others are fearful”. The Fed is 76.8% likely to cut rates by the July 18th meeting according to the Fed watch website.

Ag Fundamentals:

Wheat and soybean export sales reported above the high side of the estimate ranges this morning. Corn fell within the expected range, but still strong with another +35M bushel week. Soybean meal fell short of expectations. 4500 more soybean put contracts were added to positions this morning, giving an ominous feeling to start the day but futures begin trade higher. Strikes beginning in some ports in Argentina could be part of the reason for a small price rally. EIA ethanol numbers yesterday and export sales again this morning show corn usage and export values on the USDA balance sheet still need revision higher. Wheat getting a boost this weak by news of high Kansas winds and dry weather across the major growing regions. The dollar has also remained below 104.00 on the index. the Drought monitor did improve week-over-week in Illinois, Iowa, and Missouri.

Core Producer Price Index (PPI) was negative -0.1% for the first time since April 2023. Month-over-month PPI reported a flat 0.0% change in wholesale prices.

The Fed Watch Tool Probability shows a 76.8% chance of the Federal Reserve easing by the June 18th Meeting.

WEEKLY EXPORT SALES

| Sales 24/25 | Est Range | Sales 25/26 | Est Range |

Wheat | 783,400 | 275K-650K | 82,600 | 0-100K |

Corn | 967,300 | 700K-1.4M | 13,400 | 0-100K |

Beans | 751,700 | 300K-700K | 43,100 | 0-100K |

Meal | 184,800 | 190K-400K | 1,600 | 0-10K |

Soyoil | 68,500 | 40K-75K | 0 | 0-10K |

EXPORT & WORLD NEWS

South Korea bought about 133K MT of animal feed corn in an international tender yesterday.

Malaysian palm oil futures were basically unchanged overnight, up 1 ringgit at 4489.

Daily Trading Limits: Corn $0.30 (expanded $0.45); Soybeans $0.85 (expanded $1.30); Minneapolis Wheat $0.60 (expanded $0.90); KC Wheat $0.40 (expanded $0.60); Chicago Wheat $0.40 (expanded $0.60)

>>Interested in more commentary by Joe Mauck? Go HERE

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.