Written Commentary

OPENING COMMENTS

GEOPOLITICS:

The Russian Ukraine war has become politically charged, more-so than previous conflicts between Russia and Georgia in 2008 and Russia and Ukraine in 2014. Following the 2016 election of Donald Trump, and the media’s push to group him and Putin together, many progressive or left-leaning groups made Russia the ultimate villain and put Trump in that category. Once Russia attacked Ukraine in 2022, the first reaction from the democratic party was to support Ukraine. I don’t know if Putin, Zelensky or Biden thought the war would last this long, but there has been enough death and destruction to consider a land deal with Russia. They took Crimea in 2014. Trump’s administration has already made it clear that Ukraine will not be joining NATO and we will not provide them nukes. Russia now controls two of Ukraine’s largest ports Mariupol and Berdyansk. Trump is now forced to go over Zelensky’s head and make a deal with Russia, something Biden would not do because his base took Ukraine’s side in this conflict. Zelensky will have to be dragged to this peace deal kicking and screaming, even though this is his only option, because he can’t be seen happy with a deal where he loses territory after all the sacrifices his country and soldiers made for him so far. Ukraine will still have access to the Black sea market through the port of Odesa and others.

MACROECONOMICS:

The Dollar reacted lower to news of tariffs yesterday. The dollar is now below 107.00 and hitting a 2-month low against multiple currencies overnight. Reciprocal tariffs wont take effect until April, but news of them was enough to shave nearly 2 points off the index in the last 5 days. This week’s CPI and PPI inflation data has pushed any expectations of another rate cut this year back to October or December. Some traders are not counting on a cut at all the rest of 2025. Retail sales this morning came in lower than expected. Retail sales were expected at +0.3% but was reported at -0.4%. Some are calling that a “holiday hangover”.

AG FUNDAMENTALS:

Grain markets are finding support heading into the weekend. It will be interesting to see where funds end up in this afternoon’s COT report. Tariff news yesterday dropped the dollar giving commodities a possible short lived boost. Both CPI and PPI data has inflation higher than expected and will keep interest rates unchanged longer. South American weather regarding Brazil’s harvest and Argentina’s crop recovery, any new global trade policy developments, US weather effecting the dormant wheat crop, the reaction of the dollar, and the funds activity are on my radar. Monday is Presidents Day and markets will be closed Sunday night through Monday at 7pm when grain markets will reopen. Long weekends offer more time for headlines to effect trade coming back on Tuesday morning. Mexico has been a major part of our corn demand that has lead the commodity rally higher. Their President Claudia Sheinbaum is pushing back on Trump and any news of their resistance to business with the US may shake the corn market.

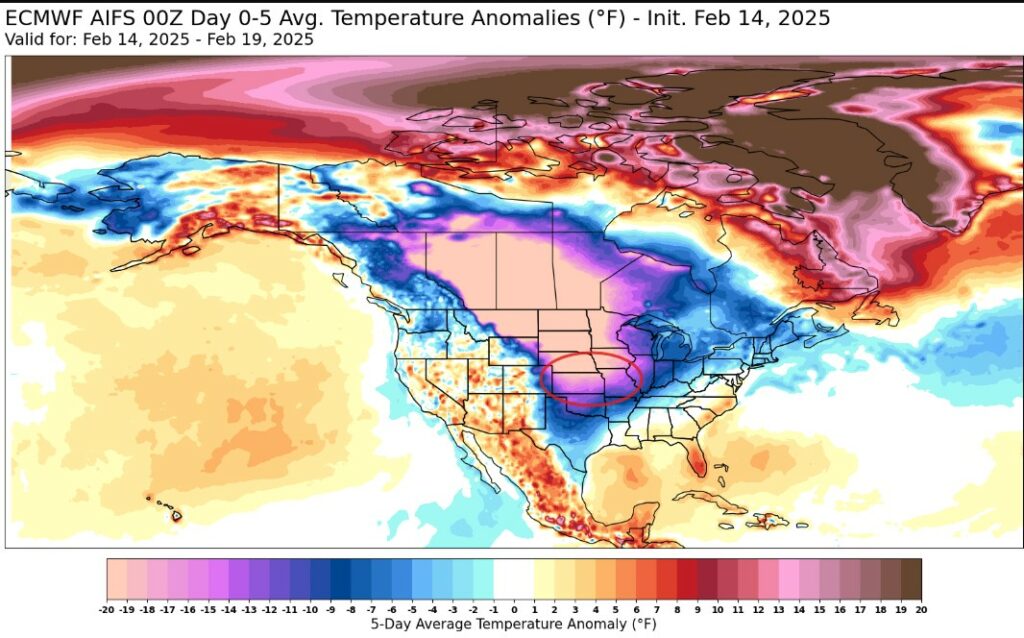

The Next 5 Days have a major portion of the wheat belt in lower than normal temps.

EXPORT & WORLD NEWS

The USDA reported Colombia bought 100K MT of corn this morning in a flash sale. South Korea bought 132K Mt of animal feed corn yesterday.

Malaysian palm oil futures were up 38 ringgit overnight, at 4592.

Daily Trading Limits: Corn $0.30 (expanded $0.45); Soybeans $0.85 (expanded $1.30); Minneapolis Wheat $0.60 (expanded $0.90); KC Wheat $0.40 (expanded $0.60); Chicago Wheat $0.40 (expanded $0.60)

>>Interested in more commentary by Joe Mauck? Go HERE

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.