Written Commentary

|

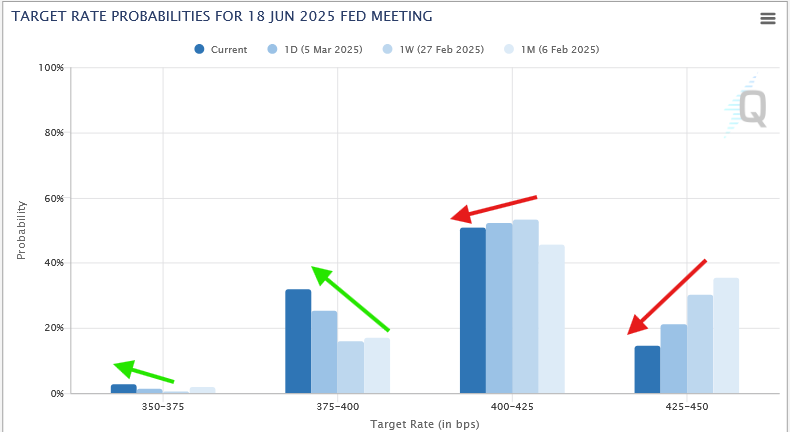

The Change in Probabilities of the Fed’s Interest Rate Cuts can be seen below. Over the last 4 weeks, the market has shifted it’s opinion of the timing of the Fed’s next rate cut. A -0.25% rate cut is now over 50% likely by the June 18th meeting and could possibly come earlier or be as high as -0.50%.

CALENDAR SPREADS

Spread | Last | Chg | Full | % of FC |

CK25/CN25 | -6 3/4 | +3/4 | -21 | 32% |

CN25/CU25 | 25 | +2 3/4 | – | – |

SK25/SN25 | -12 1/4 | +1 | -27 | 45% |

SN25/SQ25 | 5 1/4 | +1 1/4 | – | – |

SN25/SX25 | 18 3/4 | +3 1/4 | – | – |

MWK25/MWN25 | -14 | – 1/4 | -20 1/4 | 69% |

WK25/WN25 | -14 | – 1/4 | -16 | 88% |

KWK25/KWN25 | -13 3/4 | +1/2 | -16 | 86% |

COST OF CARRY

Near by spreads firming the last two sessions as tariffs are pealed off the initial Tuesday announcement. Nearby prices have rallied back stronger with hopes of continued participation from our neighboring trade partners.

Daily Trading Limits: Corn $0.30 (expanded $0.45); Soybeans $0.85 (expanded $1.30); Minneapolis Wheat $0.60 (expanded $0.90); KC Wheat $0.40 (expanded $0.60); Chicago Wheat $0.40 (expanded $0.60)

Futures Settlements & Technicals

Symbol | Close | Chg | High | Low | Support | Resist | 20-Day | 50-Day |

CK25 | 464 | +8 1/4 | 473 1/2 | 452 3/4 | 458 | 474 | 491 3/4 | 485 1/2 |

CN25 | 470 3/4 | +7 1/2 | 479 3/4 | 459 1/2 | 468 | 480 | 496 1/2 | 488 3/4 |

SK25 | 1027 1/4 | +15 1/2 | 1036 1/2 | 1013 3/4 | 1022 | 1036 | 1044 1/4 | 1041 1/2 |

SN25 | 1039 1/2 | +14 1/2 | 1047 1/4 | 1026 1/2 | 1033 | 1055 | 1059 1/4 | 1054 3/4 |

SQ25 | 1034 1/4 | +13 1/4 | 1041 1/4 | 1022 | 1029 | 1042 | 1056 1/2 | 1051 |

MWK25 | 594 | +6 | 598 | 586 | 590 | 604 | 624 1/4 | 613 |

MWN25 | 608 | +6 1/4 | 612 | 600 1/4 | 604 | 617 | 637 1/4 | 623 3/4 |

WK25 | 554 | +5 3/4 | 562 | 544 3/4 | 550 | 563 | 583 1/4 | 569 |

WN25 | 568 | +6 | 574 3/4 | 558 1/2 | 564 | 577 | 596 | 580 |

KWK25 | 565 3/4 | +8 3/4 | 570 3/4 | 554 1/2 | 562 | 578 | 599 3/4 | 582 1/2 |

KWN25 | 579 1/2 | +8 1/4 | 584 | 568 1/2 | 573 1/2 | 590 | 611 1/4 | 592 1/2 |

SMK25 | 304.9 | +5.10 | 307.6 | 300.5 | 302.00 | 309.00 | 302.90 | 309.30 |

BOK25 | 43.17 | +0.18 | 43.59 | 42.91 | 42.95 | 43.75 | 45.72 | 44.65 |

>>Interested in more commentary by Joe Mauck? Go HERE

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.