Written Commentary

CLOSING COMMENTS

Macroeconomics:

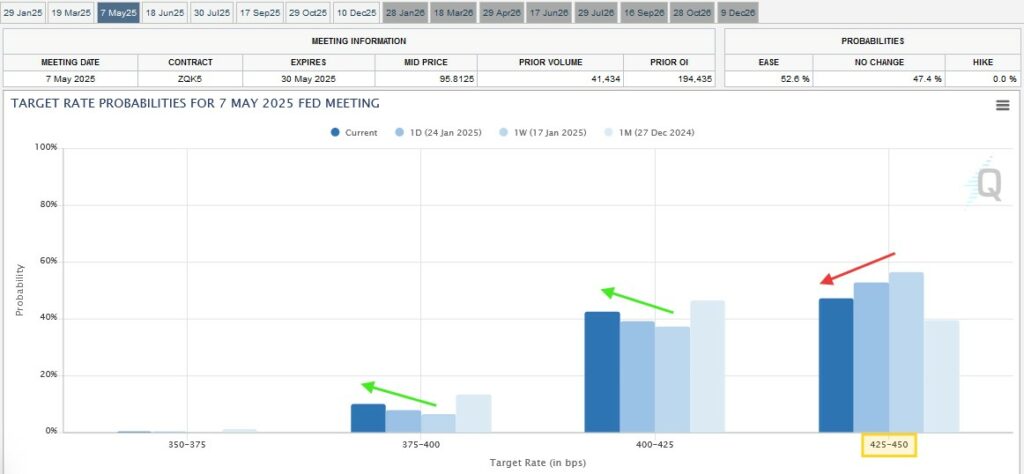

The dollar is weaker today, but gold is retreating as an AI tech sell off hits the equity markets today. NVIDIA is on pace to see the largest one-day drop in market cap in history. Sell offs like this are great opportunities for safe money to move into the high performing spaces. Traders are pricing in a 99% chance the Fed will not cut interest rates this week. The fed has been facing pressure from President Trump to continue to cut rates. Since the start of the new year, expectations of 4 cuts in 2025 has weakened to 2 or less. The next cut is most likely coming in June, but odds of the Fed cutting rates sooner (May 25th) have recently increased.

Ag Fundamentals:

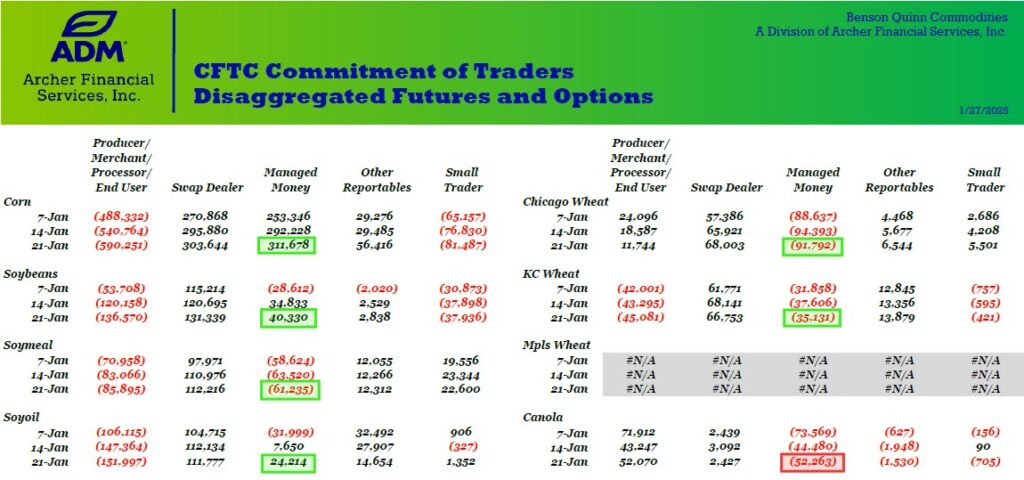

Export inspections for last week were in line with expectations for both wheat at 261K MT and soybeans at 973K MT. Corn export inspections were above the range estimates, at 1.541 million MT. Recently notable corn buyers have been Mexico, South Korea, Taiwan, Japan and Spain. Mato Grosso’s 2nd corn crop planting progress is behind the average pace. It is not raising too much concern yet because it is still very early; planting there typically finished up in the last half of March. The last time Mato Grosso was this far behind pace was 2021, subsequently their 2021 yields were recorded as some of the lowest in recent history. Friday’s CFTC commitment of traders report showed managed money adding to their corn and bean length. Today estimates suggest managed money sold nearly 6K contracts of corn and 3400 contracts of soybeans. Corn prices bottomed last summer when MM positions were near -350K contracts short, and we saw a reversal rally leading us to almost the same number of contracts long.

The CFTC COT Disaggregated Futures and Options Report showed managed money increasing their corn, soybean and soyoil length. Managed money also covered shorts in soybean meal, and wheat while increasing their short position in only canola.

The Probability of Federal Rate Cuts have increased for the May 25th Fed meeting. It is still most likely that the fed will wait until June to cut rates again, but that could change if inflation and labor market reports show weakness between now and then. This month’s meeting announcement is scheduled for Wednesday afternoon.

CALENDAR SPREADS

Spread | Last | Chg | Full | % of FC |

CH25/CK25 | -10 1/4 | – 1/4 | -21 1/4 | 48% |

SH25/SK25 | -13 1/2 | -1 | -27 1/4 | 50% |

SK25/SN25 | -11 3/4 | – 1/2 | -27 1/2 | 43% |

SH25/SN25 | -25 1/4 | -1 1/2 | -54 1/2 | 46% |

MWH25/MWK25 | -11 | – 1/2 | -20 1/4 | 54% |

WH25/WK25 | -14 1/4 | +1/2 | -16 | 89% |

KWH25/KWK25 | -9 1/2 | +1/2 | -16 | 59% |

COST OF CARRY

Regarding corn spreads weakening nearby: expectations of slower ethanol production pace, exports expect to remain steady as commercials are still buying grain below delivery, and the farmer still has 30-40% left to sell. Soybean spreads are in a similar situation with the commercial long and Brazilian beans expecting to hit the market in less than a month.

Daily Trading Limits: Corn $0.30 (expanded $0.45); Soybeans $0.85 (expanded $1.30); Minneapolis Wheat $0.60 (expanded $0.90); KC Wheat $0.40 (expanded $0.60); Chicago Wheat $0.40 (expanded $0.60)

>>Interested in more commentary by Joe Mauck? Go HERE

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.