Written Commentary

CLOSING COMMENTS

Macroeconomics:

The US Dollar saw another boost to end this week with the GDP data from Europe coming in lower than expected by -0.25%. The Market was expecting a +0.15% change and they saw -0.1% reported. Additionally the Swiss national bank cut interest rates by-50 basis points alongside the European Central Bank cutting rates by -25 basis points yesterday. The US Federal Reserve Bank is expected to cut -25 basis points next Wednesday following a neutral CPI report a couple days ago. The US dollar has seen a surge in the last couple months due to the global optimism behind change in US executive leadership. AKA Trump puts the US first, making the US an attractive investment compared to anywhere else in the world.

Ag Fundamentals:

Two flash sales of soybeans in the last two days gave a whisper of support against the South American supply head winds. Totaling 634K MT of soybeans sold to Unknown destinations, or 23.293 million bushels of beans. The largest flash sale since the 840K MT sold to unknown on November 29th. Argentina corn planting should be about 60% complete by this weekend and Argentina is also nearing 60% for their soybean planting progress as well. Brazil will begin their second corn crop planting in January, so uncertainty around their largest corn crop supply is still in the conversation. Growing conditions in South America remain neutral, and precipitation is expected to be average to slightly below average for the next couple weeks. Production estimates for both Brazil and Argentina feels optimistic and could increase over the next 2 months. Thinking about planted acres for next year, corn looks a lot better than beans today. Despite the cost to plant corn being higher than beans from a cash-on-hand perspective, corn pencils much better than beans from a production/value outlook and could offer better cash flow opportunities for farmers next fall. it will be interesting to see how the commitment of traders report shapes up later this afternoon. Many expecting to see the funds adding to their corn length and possibly short covering wheat.

Weather:

The Midwest will see a relief from the cold weather for the next 5 days. Rains are expected to spread moisture from Arkansas and Missouri east toward Indiana and Ohio. This should allow for river levels to improve enough to revert barge drafts back to max levels for a few days at least. Water levels have still not fully recovered in the US river systems and could become an issue over the next few months if conditions do not improve.

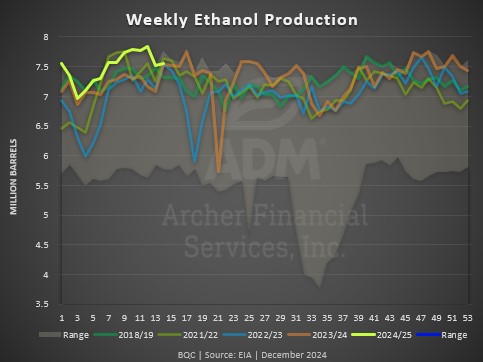

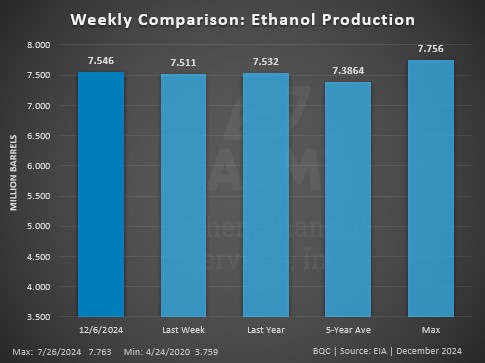

Ethanol Production was slightly higher week over week to 1,078K barrels per day. Ethanol production was in line with expectations. Usage was 560K bu more than the needed pace to hit the revised USDA projection of 5.5 billion bushels. Ethanol and corn exports continue to be the driver behind price support for corn. Ethanol stocks came in slightly lower at 22.65 million barrels.

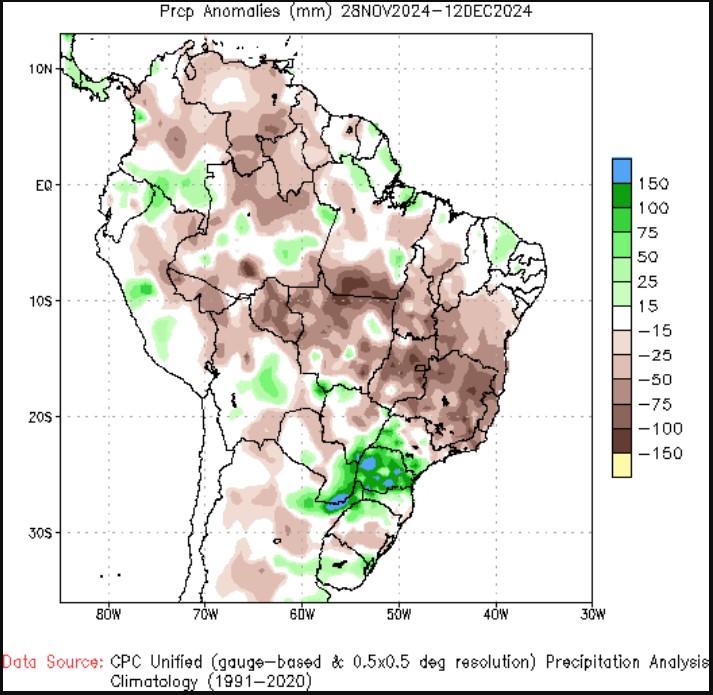

The 15-Day Precipitation Anomaly Map shows most of Brazil’s growing regions receiving less than normal rainfall over the next 15 days. This may continue into the first week of January as well. Parana (13% of production) will see above normal precip in the next 2 weeks.

Calendar Spreads

Spread | Last | Chg | Full | % of FC |

CH25/CK25 | -7 1/4 | +1/4 | -20 3/4 | 35% |

SF25/SH25 | -6 3/4 | +3/4 | -25 3/4 | 26% |

SH25/SK25 | -10 1/2 | – 1/4 | -26 3/4 | 39% |

SF24/SN25 | -27 3/4 | +1/4 | -79 1/4 | 35% |

MWH25/MWK25 | -7 | +1/4 | -20 1/2 | 34% |

WH25/WK25 | -10 | – 1/4 | -16 | 63% |

KWH25/KWK25 | -8 1/4 | – 3/4 | -16 | 52% |

Cost of Carry

no current data available

Daily Trading Limits: Corn $0.30 (expanded $0.45); Soybeans $0.85 (expanded $1.30); Minneapolis Wheat $0.60 (expanded $0.90); KC Wheat $0.40 (expanded $0.60); Chicago Wheat $0.40 (expanded $0.60)

>>Interested in more commentary by Joe Mauck? Go HERE

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.