Written Commentary

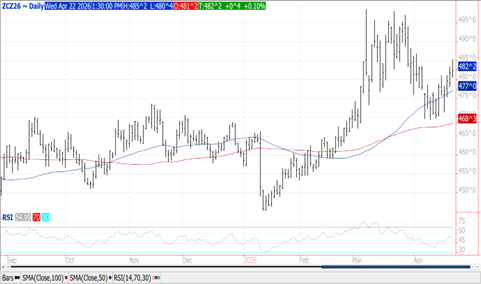

CORN

Prices were steady to $.02 higher as weakness in the soybean complex weighed on corn values. Spreads were mixed. Both July-26 and Dec-26 traded to fresh 3-week highs before pulling back. Our expected range for July-26 of $4.50-$4.75 remains intact. The USDA announced a flash sale of 130k mt (5 mil. bu.) to an unknown buyer. A group of congressional lawmakers, the E15 Rural Domestic Energy Council, is expected to submit legislation that would allow the year-round sale of higher ethanol gasoline while also restricting exemptions for smaller refineries. If ultimately passed, domestic corn demand could grow by 2-2.5 bil. bu. over the next several years. Ethanol production fell to 306 mil. gallons LW, down from 329 mil. the previous week, however still up 1% from YA. Production was at the low end of expectations. There was 103 mil. bu. used in the production process, or 14.66 mil. bu. per day, below the 15.4 needed to reach the USDA forecast of 5.6 bil. Ethanol stocks jumped to 26.7 mil. barrels, well above the 25.5 mb from YA. Implied gas usage LW fell .4% to 9.055 tbd, and was off nearly 4%YOY. EU corn imports as of April 19th at 14.14 mmt are down 17% YOY. Tomorrow’s export sales are expected to range between 40-75 mil. bu. Despite huge production forecasts in Argentine, their FOB offers remain above US Gulf offers.

SOYBEANS

Prices turned lower at midday while making new lows in late trade. Soybeans finished down $.10-$.11, meal was $3-$5 lower while oil was down 50-65 points. July-26 beans rejected trade back above the $12 level. Nov-26 stalled just below its March high at $11.74 ¼. Early strength saw new contract highs in soybean oil with the spot contract trading to a 3 ½ year high before pulling back. Crush margins back up a few cents to $3.29 ½ bu. while bean oil PV improved to a new all-time high at 52.8%. Improved demand for biofuels combined with surging D4 RIN values has increased biodiesel and RD profit margins. Speculative traders bought nearly 13k contracts of bean oil yesterday, however O.I. increased only 1,100 contracts. The price surge however has left bean oil less competitive compared to other feedstocks for biofuel production. The early strength in energy prices was largely attributed to President Trump extending the ceasefire agreement with Iran. While the length of the extension is not clear, the Administration felt it was warranted due to Tehran’s “seriously fractured” government. The US military blockade of Iranian ports will continue until “their leaders and representatives can come up with a unified proposal”. Wire services are reporting at least 10 vessels are being held up at Argentine ports as a trucker protest over increased costs is preventing supplies from reaching key export hubs. EU soybean imports at 10.24 mmt are down 11% YOY. Meal imports at 14.22 mmt are off 7.5%. Tomorrow’s export sales are expected to range from 8-26 mil. bu. of beans, 150-500k tons of meal and -10-14k tons of oil.

WHEAT

Prices were steady to $.06 lower in choppy 2-sided trade. Spreads were mixed and little changed. CGO July-26 traded to a fresh 3-week high before pulling back. KC July-26 has resistance at LW’s high of $6.63 while MIAX July-26 held within yesterday’s range. EU soft wheat exports as of April 19th at 19 mmt are up 8% YOY. Rusagrotrans reports Russian exports in April will likely reach 3.8 mmt, well above the 2.4 mmt shipped in April-25. SovEcon raised their Russian wheat production forecast 2.1 mmt to 89.7 mmt however warned that a potential frost may threaten production yet this spring. Early ideas on US winter wheat production is just below 1.20 bil. bu. which would be the lowest since 2022. Export sales are expected to range from 6-18 mil. bu. For HRW futures (KC) to test the $7.00 level would likely take production falling below 600 mil. bu. vs. 804 mil. YA.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.