Written Commentary

Price Overview

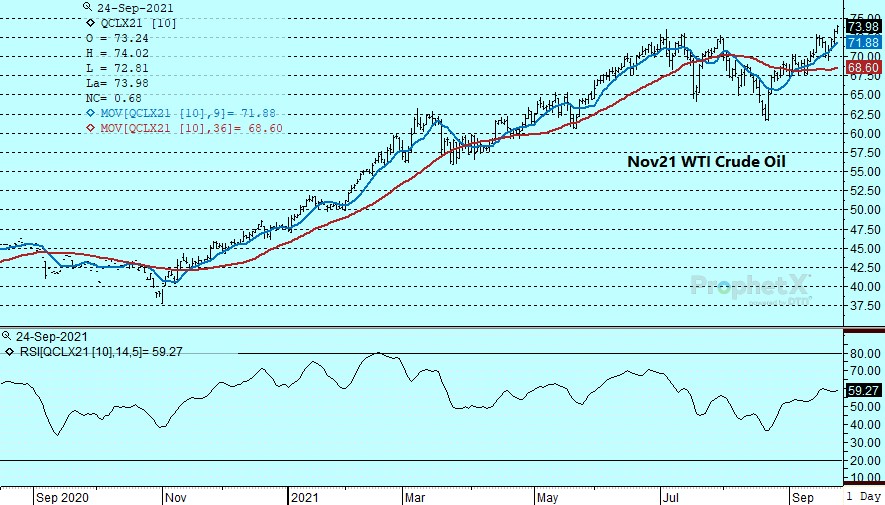

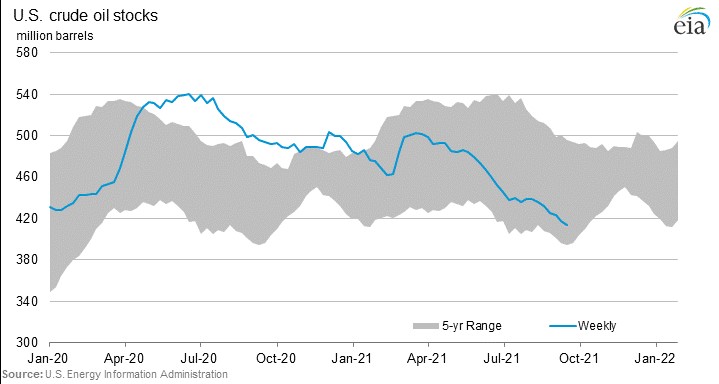

The petroleum complex continued to attract good underlying buying interest ahead of the weekend. Both Nov Crude oil and Heating Oil reached new highs for the move reflecting a stable economic environment and growing concerns over the adequacy of supplies given the ongoing decline in US inventory levels and higher than expected compliance rates with the OPEC+ output pact and growing fears over the ability of some OPEC+ producers to meet their output targets. In addition support was also provided by reports that damage to an offshore transport facility will limit Mars sour crude supplies into early next next year by as much as 250 tb/d. Although reports that China had sold crude oil from their Strategic Reserves encouraged selling early it did not attract follow-through on ideas the amounts were insignificant relative to their consumption.

The market still appears to have a bullish bias and given the new highs for the move today November Crude might be poised to trend up toward the 77.00 level basis November. Strengthening demand at a time when stocks are declining along with uncertain production prospects should underpin buying interest for the foreseeable future. Although some uncertainty might exist into the OPEC+ meeting on Oct 4, the appearance that OPEC+ is unwavering in the current agreement along with the challenges being experienced with the supply chains and the adverse impact on production levels in some areas, should limit price setbacks.

Natural Gas

Nat Gas prices continued to follow through on yesterday’s strong rebound as a pickup in heating demand offset the impact of weaker demand for cooling. In the background remain fears of growing shortages overseas as winter approaches and the need for quick adjustments in demand patterns and a shift back to coal which remains politically unpopular for electrical power generation. The slow pick up in domestic production to 90.7 bcf /d in September from 92.0 in August and a monthly record of 95.4 bcf/d in August of 2019 has also been in the background. Another bullish influence has been prospects for high export levels of LNG due to the high premium of international prices to those in the US which likely assures the optimization of production capacity at LNG plants limiting availability for domestic uses. The EIA report which showed a build of 76 bcf/d appeared to have been ignored in favor of the longer term concerns over the adequacy of stocks as we move toward winter. For next week the potential exists for values to retest the 5.25 area basis November particularly if fears of regional shortages particularly in the North East grow.

Charts Courtesy of DTN Prophet X, EIA, Reuters

The authors of this piece do currently maintain positions in the commodities mentioned within this report.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.