Written Commentary

by market analysts Stephen Platt and Mike McElroy

Price Overview

Crude oil failed to follow through on early strength that had carried values to as high as 89.64 basis October, settling 32 cents lower at 88.52. Constructive sentiment linked to concerns over low inventory levels during the fourth quarter was dashed by the DOE inventory report.

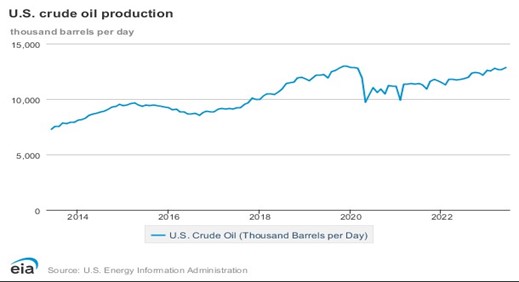

The report showed an unexpected build of 4.0 mb in commercial crude inventories along with a surprising increase in gasoline and distillate stocks of 5.6 and 3.9 mb respectively. Overall, the report was negative, but some aspects were seen as constructive given the location of the stock build, which was concentrated on the Gulf Coast while stocks in the Midwest and Cushing showed marked declines of 4.2 and 2.4 mb. Net import levels of crude surged to 4.5 mb compared to the four-week average of 2.8. Crude and products showed net imports of 431 tb compared to net exports last week of 2.6 mb. Of interest has been the recovery in US crude production, which was indicated at 12.9 mb in today’s report. As the chart shows, crude production has been steadily recovering despite the decline in rig counts as more efficient technologies are employed to increase productivity of existing wells in shale areas.

The IEA monthly report suggested that oil output cuts by Saudi Arabia and Russia into the end of 2023 will create a substantial deficit through the fourth quarter. These cuts have been offset by higher supplies from producers outside the alliance including the US, Brazil, and Iran, which is still under sanctions but exempt from output cuts. Key to the outlook will be whether curbs are extended into 2024 and the impact of higher prices on production in other countries.

The market has encountered resistance at the higher end of our target range near 90.00. With interest rates likely to remain high and uncertainty over the Chinese economy persisting, it would not be surprising to see a pullback toward the 85.00 area basis prompt crude. A stronger decline would be contingent on more dire forecasts for China. In addition, we are skeptical of Russia’s position in the Ukraine war. Recent overtures to get weapons from North Korea suggests deep problems in the Russian military.

Natural Gas

Prices oscillated higher and lower today before weakening late in the session to end with a loss of 6.3 cents at 2.68 basis October. This followed strong upside action yesterday that saw the market bust through resistance to gain over 13 cents. Explanation of the strength was lacking, as fundamentals were a mixed bag. The move above the 9 and 100-day moving averages in the 2.66-2.69 range lead to the chart gap at 2.735 from Labor Day weekend being filled. Buy stops were triggered on the move that propelled prices 12 cents higher in a 30 minute time period that saw in excess of 25 thousand contracts traded. Not surprisingly prices eased today with questions surrounding the continued drop in LNG flows to Freeport, as nominations are off 1 to 1.5 bcf/d since Saturday with little explanation. Production, which had shown signs of significant slowing with early nominations this week, saw late cycle revisions that erased the concern each time. The clearing out of the upside has moved initial resistance to yesterday’s high near 2.78, with a push through there targeting the double top from September 1st at 2.86. The move above the 9-day switches it to initial support, currently near 2.65. Below there 2.50 remains key support to avoid probing to the lows at 2.377. Tomorrow’s storage report is expected to show a 48 bcf injection compared to the 5-year average increase of 76.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.