Written Commentary

by market analysts Stephen Platt and Mike McElroy

Price Overview

Crude oil traded on the defensive in advance of the OPEC+ virtual meeting on June 2nd and following the unexpected movement of both crude and product stocks in yesterday’s DOE release. The July contract settled 92 cents lower at 76.99. The primary focus remains on the meeting and the expectation that voluntary cuts of 2.2 mb/d will be rolled over into the third and possibly 4th quarter of 2024. Discussions are also occurring on whether earlier reductions totaling 3.66 mb/d, which have been in place since late 2022 and are valid until the end of 2024, will be rolled over into 2025. The decisions and allocations will be controversial and could lead to a decision being delayed pending further discussions and assessment.

The use of the production capacity of member countries for the calculation of output targets will complicate an agreement. Previously, members had reported their own capacity figures. To diffuse disagreements over targets, the group has tasked three independent consultants to assess member capacity by the end of June, which could have a bearing on future production allocations after current cuts expire at the end of 2024. While it is unlikely to have a bearing on the extension of current voluntary cuts at their meeting on June 2nd, it could affect how long cuts are in effect.

The DOE report provided little in the way of confidence that the stock situation had tightened. Although the decline in crude stocks of 4.2 mb was more than expected, it was offset by the larger than expected build in gasoline of 2 mb and in distillate of 2.5, reflecting a sharp increase in refinery utilization of 2.6 to 94.3 percent. Total stocks of crude and products rose 12.7 mb to stand at 1,263.2 mb compared to 1,242.8 last year. Total disappearance rates were disappointing at 19.4 mb compared to 20.0 last week, with gasoline disappearance at 9.1 mb/d falling short of last weeks’ 9.3 despite the expected pickup ahead of the Memorial Day weekend. Net exports of crude and products were 1.8 mb/d.

Given the increase in global inventories, price increases will be contingent upon OPEC+ deliberations and how intent they are on balancing the market. Demand concerns linked to rising EV use and slower than expected economic growth in China remain in the background as limiting factors. A rolling over of current cuts will help stabilize values in the low 80.00 area as the market assesses the degree of stock drawdowns in the second half of the year, with Middle East tension still not having an appreciable impact on supplies.

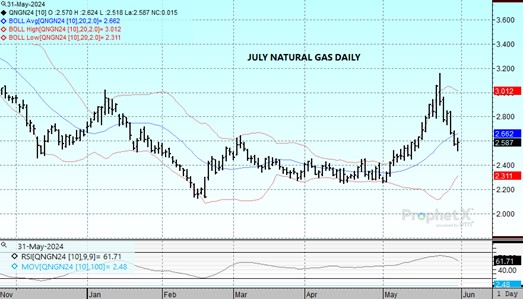

Natural Gas

The streak of new lows continued for the fifth straight session, with the July reaching down to 2.518 before short covering into the weekend lifted values to a settlement at 2.587 for a gain of 1.5 cents. The market has been weighed down by the recent recovery in production, which has been maintained above 98 bcf/d since May 22nd, which marked the beginning of the pullback. Yesterday’s storage report did little to help the situation as the 84 bcf build was above pre-release estimates near 78, leaving total stocks 26.5 percent above the 5-year average. Demand is running near seasonal norms, although moderation in the South Central region over the weekend has weakened cash prices and helped drag down the market. The break has now retraced 68 percent of the May rally. Forecasts for a warm June will need to materialize in the coming weeks to stabilize the market, with today’s lows near 2.50 a key area to maintain in order to avoid any further downside extension, with help from the 50 and 100-day moving averages just below there in the 2.47-2.48 range. Improvement in LNG flows would go a long way toward aiding a recovery, with minor resistance near 2.66 and then 2.80. A settlement above the 200-day moving average currently near 2.82 is necessary to rekindle technical interest and any hope of another attempt at a summer rally.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.