Written Commentary

by market analysts Stephen Platt and Mike McElroy

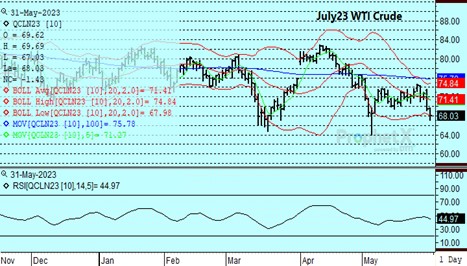

Price Overview

The petroleum complex recovered partially from sharp early losses to close lower by $1.37 at 68.09 basis July crude. Early selling was traced to weaker than expected manufacturing activity in the US and China, and the potential for an additional interest rate hike. Scattered buying and short covering developed in response to nervousness ahead of the OPEC+ Ministerial meeting on June 4th along with the possibility of SPR purchases being announced.

The weakness continues to put pressure on major oil exporting countries to support revenues by underpinning crude values through a production cut. In addition, recent attacks on Russian refineries by Ukrainian interests, strains in the Russian economy, and the potential for more stringent sanctions could move Russia away from the stance expressed last week by Deputy Prime Minister Novak, who indicated “that prices were approaching’ economically justified levels” and that he did not expect new steps by OPEC+. Instead, the price weakness might support comments by the Saudi Oil Minister for “shorts to beware” similar to what occurred in April when the market surged toward the 80.00 level on the announcement production cuts, which took effect this month.

Economic uncertainty in China and the US remains a key driver of bearish sentiment, but offsetting that negative tone is the potential for an increasing pace of economic recovery in Europe, Japan and other Asia countries. Look for steady support to global oil demand as we move through summer as driving and air travel pick up. Any move to cut production by OPEC+ or purchases to rebuild the SPR in the US would exacerbate a decline in stocks and potentially lead to a recovery back toward the 76.00 level basis July crude.

The DOE report to be released tomorrow is expected to show crude inventories off 1.2 mb, distillate up by 1.1 and gasoline down .2 mb. Refinery utilization is expected at 92.4 percent, an increase of .7 from the prior week.

Natural Gas

The break that started late last week saw good follow-through after the long holiday weekend, as the July contract tested the lows yesterday and contined to see good selling interest late in today’s session, settling with a loss of 6.1 cents at 2.266. Weekend production levels moved up to the 102.5 bcf/d area and kept downside pressure on the market, with weather offering little to get excited about. Today saw prices bounce early on signs of heat developing into the back end of the forecasts, and coupled with the oversold level of the market lead to a spate of short covering. Weakness resumed into the close as the reality of ample stocks and unreliable forecasts sapped the market’s strength. Tomorrow’s storage report is expected to show a 106 bcf injection compared to the 5-year average of 101. The poor close points to an imminent test of the lows at 2.232, with support below there at 2.15. If heat continues to be elusive, the 2-dollar level could be seen in the near term. Resistance is scattered until the 2.45-2.50 range.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.