Written Commentary

by market analysts Stephen Platt and Mike McElroy

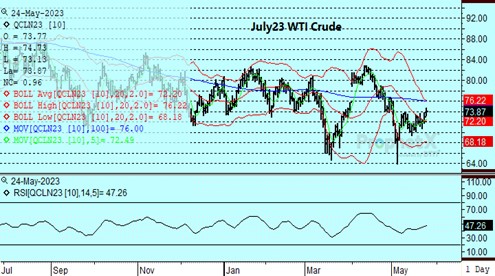

Price Overview

The petroleum complex traded higher on a larger than expected draw in crude inventories compared to estimates of a small build. Crude settled up $1.43 at 74.34 basis July, while gasoline closed up 6 cents and ULSD rose 4.94. The rally developed despite ongoing strength to the dollar and continued uncertainty over the debt ceiling negotiations, which undermined global equity values. Fear of low gasoline stocks into the seasonably strong summer driving season along with Saudi warnings to short sellers to “watch out” ahead of an OPEC meeting scheduled for June 4th also influenced the upside sentiment.

The DOE report released this morning showed commercial crude inventories falling by 12.5 mb, while Cushing stocks rose by 1.7. In products, gasoline stocks fell 2.1 mb while distillate declined by .6. Total stocks of crude and products fell 10.8 mb. Refinery utilization fell .3 to 91.7 percent. A key aspect of the report was total disappearance, which rose to 20.7 mb, an increase of 1.7 and compared to 19.7 mb last year. Gasoline rose to 9.4 mb compared to 8.9 last week while distillate rose to 4.2 mb from 3.7. Net export levels for crude and products rose moderately to 2.2 mb, from 1.9 in the prior week.

Today’s report is the first validation that the supply/demand balance will get increasingly tighter as we move into the second half of the year. Given the production problems in Alberta, Canada due to forest fires along with disruptions to Kurdish exports to Ceyhan, we are doubtful that OPEC+ will curb output at their meeting in June despite their comments. Although this might be a source of disappointment near term, a steady economic recovery in China will underpin values on setbacks tied to US economic uncertainty, a stronger dollar, and no change in policy by OPEC+. The potential for a supply deficit of up to 2 mb/d during the second half of 2023 on the back of strong gasoline demand and current OPEC+ production cuts should remain a bullish influence. Resistance should surface near the 100-day moving average at 76.22 basis July crude.

Natural Gas

This week’s settlement prices have varied by less than 8 cents as the market awaits signs of summer heat. The 15-day forecasts have shown little recent variation, which has helped to reign in volatility. Poor wind generation levels again this week helped prices recover some of Monday’s losses as the July contract gained 7.7 cents to settle at 2.566 on low volume. Tomorrow’s storage report is expected to show a 100 bcf build in stocks compared to the 5-year average increase of 96. With improved production levels and a recovery in Canadian imports in the background as negative influences, the market will have difficulty mounting a substantial upside move unless heat begins to surface as we enter the summer. The settlement below the 9-day moving average yesterday was a negative near-term signal, although prices recovered today. Another push below 2.50 could lead to a quick test of the lows ahead of any warming in temperatures. If today’s strength can follow-through there is not any obvious resistance until the 2.70 area.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.