Written Commentary

by market analysts Stephen Platt and Mike McElroy

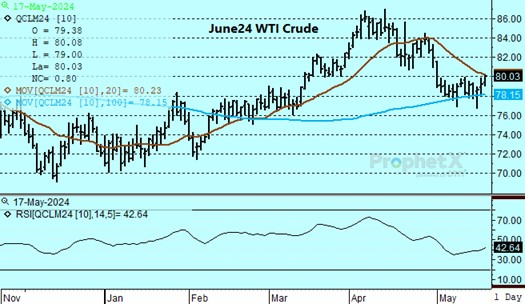

Price Overview

Crude oil settled 83 cents higher at 80.06, following through on yesterday’s gains that were traced to expectations that the US Federal Reserve will cut rates earlier than previously expected. Additional support was provided by Chinese industrial output rising by 6.7 percent year-over-year in April, and on the announcement of new steps to revitalize their property sector. In the background was another attack on Russian infrastructure by Ukrainian drones. Offsetting the strength were reports of scattered showers helping contain wildfires near Fort McMurray in Alberta Canada and the lack of damage. In addition, reports that Chinese refinery output fell by 3.3 percent in April from a year earlier due to thin profit margins for small refineries and seasonal maintenance moderated gains.

For next week, the market will be watching a variety of factors. The wildfires in Alberta and forecasts for a return of dry conditions could arouse concern over additional disruptions to production. In addition, recent declines in US stocks due to increased refinery utilization are likely to continue with the pick-up in gasoline demand into the summer. At the same time ARA stocks (Antwerp, Rotterdam, and Amsterdam) fell by 112,000 metric tonnes to 6.15 million metric tonnes in the week ending May 15th.

Look for prices to work up to the 81.50 level basis June as concerns build over Canadian wildfires affecting crude production. In addition, a weaker US dollar and lower interest rates should provide support. Caution is likely ahead of the OPEC meeting on June 1st, with expectations for voluntary production cuts of 2.2 mb/d to be rolled over into the second half of the year, keeping stocks balanced in the absence of a strong Chinese recovery.

Natural Gas

The steady climb higher continued into the end of the week as the June natural gas gained 7.9 cents yesterday and added another 13.1 today to settle at 2.626. Upward momentum was assisted by yesterday’s storage report. The 70 bcf build was well below estimates near 77 as the supply overhang, although still ample, continued to be chipped away. Prices overreacted after the release, jumping by over 10 cents to the day’s high before giving back some of those gains into the close. Today’s strength was lacking a specific cause as the market traded on the bigger picture, seemingly wanting to price in the potential for a hot summer. Expectations for substantial heat in Texas in the coming days has piqued this concern. Production dropping back under 97 bcf/d after a brief runup to the 98 area last weekend also helped support the bullish sentiment. With the RSI nearing 80 percent, the market is ripe for a pullback. A 38 percent retracement of the May rally would put prices in the 2.36 area, which also coincides with the 9-day moving average for solid support. Considering the relentless nature of the current rally and strong close, the retrenchment could be delayed until the chart gap at 2.702 is filled. The 200-day moving average near 2.66 will offer resistance in advance of that level.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.