Written Commentary

by market analysts Stephen Platt and Mike McElroy

Price Overview

Crude oil prices failed to respond dramatically to weekend events in Russia in which Putin survived a threat to his rule from the mercenary Wagner group. Although the subsequent negotiations and withdrawal of the group helped calm the situation, the grip on power by Putin and his supporters in Russia is being questioned along with its impact on the War in Ukraine. While there did not appear a direct threat to the Russian Oil industry, risk premium on Geo-political concerns appeared to rise and attracted support to the petroleum complex.

While questions over Putin and the prospects for his rule will persist and how it might impact relationships with China and even members of OPEC+ including Saudi Arabia, we suspect that unless something materially changes the focus will revert back to the main issues that had been dominating the oil market in recent weeks. These include the economic prospects for China, the impact of higher interest rates in the OECD economies including the US along with Russian and Iranian availability. Inventory levels in key markets in both Asia and the US will likely be assessed to see if forecasts of an impending stock decline in the second half of the year materializes to the level currently envisioned.

Despite the uncertain outlook, we still look for an expansion in oil demand, and marginal increases in supply for the remainder of the year to provide support to values. Steady growth in demand from key non-OECD consumers such as India and China should offset the lackluster demand in OECD countries. Reports that availability from Russia has declined in June might provide background support if true. On the other hand, the appearance that discussions between the US and Iran aimed at limiting their nuclear program have been reopened have potential to shade values to the downside if progress is made. Saudi efforts to support values with additional production cuts in July will help limit downside pressures. Look for stock declines to gain momentum with support in the 67-68 range. An accommodative monetary policy in China and strength to India’s economy will help tighten inventory levels and underpin valuations later this summer with potential to push values toward the 75-76 level basis prompt crude.

The DOE report is expected to show crude inventories -1.5, distillate +.7 and gasoline -.3 with refinery utilization +.3 percent to 93.4 percent.

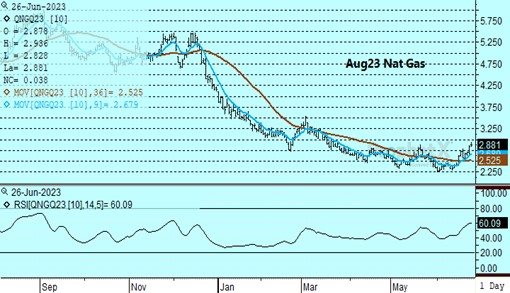

Natural Gas

Prices gapped higher coming out of the weekend but settled back ending with a gain of 4.9 cents at 2.892. Extensive heat in the South Central region, and specifically Texas, continues to be the main driver of the recovery, with over a week of extensive heat still in store for the region. Overall US forecasts remain above normal, adding to the bias. LNG flows crept up near 11.4 bcf over the weekend, further emboldening bulls as Sabine Pass appears to be coming out of an extended maintenance period. A push above the 2.885 area will target 3 dollars as the next resistance. The extended weakness experienced over the last year makes a spike in volatility likely as we head into summer with early signs of warmer trends in the US and Europe. If the market can pierce the 3 dollar level, a quick bounce to the March highs just above 3.50 would not be surprising assuming continued warmth. Support now rests at the 100-day moving average near 2.77 and below there at 2.65.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.