Written Commentary

by market analysts Stephen Platt and Mike McElroy

Price Overview

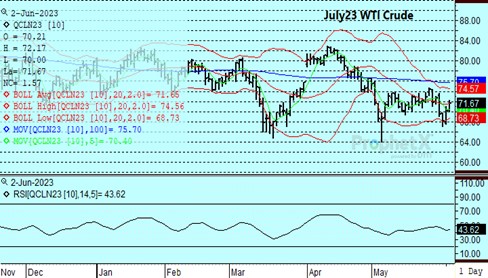

The petroleum complex traded higher following approval of a bipartisan deal to raise the limit on the US government debt ceiling. Additional support was provided by dollar weakness along with the strength in equity markets ahead of the OPEC+ meeting on June 4th. Although many are suggesting a further cut by OPEC+ is unlikely, caution ahead of the meeting and the sizable spec short position attracted buying given the surprise cuts announced in April. Additional support was provided by the stronger than expected jobs report which helped temper recessionary fears, but also showed wage gains at modest levels. We still have not ruled out the potential for a production cut, but currently it looks like OPEC will wait for additional data, particularly into summer when demand is still expected to exceed supply.

Economic uncertainty in China and the US remains a key driver of bearish sentiment, but offsetting that negative tone is the potential for an increasing pace of economic recovery in Europe, Japan, and other Asia countries. Look for steady support to global oil demand as we move through summer as driving and air travel pick up. Any move to cut production by OPEC+ or purchases to rebuild the SPR in the US would exacerbate a decline in stocks and the prospects have potential to lead to a recovery back toward the 76.00 level basis July crude.

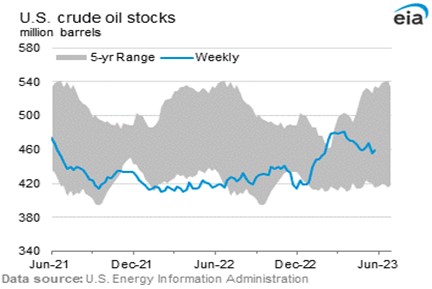

Despite the unexpected rise in commercial crude inventories of 4.5 mb and from the SPR of 2.5 mb reported yesterday by the DOE, the market failed to respond on the downside, suggesting other influences at work, The crude build in Cushing of 1.6 mb needs to be watched with stocks back to normal levels of 38.9 mb. Total stocks of crude and products rose sharply by 11.3 to 1,242 mb. Refinery utilization surged to 93.1 compared to 91.7 percent last week. Disappearance levels weakened from the prior week for all products to 19.4 compared to the strong level last week of 20.7 mb. While gasoline disappearance fell by .3 mb to 9.1 mb, jet kero rose to 1.78 mb compared to 1.43 the prior week. Disappearance levels and particularly gasoline will be watched closely in the weeks ahead to see if a strong driving pattern emerges.

Natural Gas

The market continued to see weakness as the July contract traded down to a new low yesterday at 2.136 before seeing some minor upside action today, gaining just over a penny to end the week at 2.172. Production hit a new record at midweek just above103 bcf/d, enforcing the negative tone that was amplified by the weekly storage report showing a 110 bcf injection that was well above most estimates. LNG flows remained below capacity, coming in under 13 bcf/d the last two sessions and further pressureing values. Minor end-of-week short covering and buying tied to signs of warming into the middle of June helped support prices today. With recent support taken out, the next target on the downside is 2 dollars, which could be reached early next week in the absence of developing heat. A move higher on any signs of improved demand potential will find little resistance until the 2.38-2.43 range.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.