Written Commentary

by market analysts Stephen Platt and Mike McElroy

Price Overview

Crude oil prices recouped early losses to close sharply higher at 72.70 basis February, a gain of 2.32 on the day. The strength was linked to reports of a shutdown at the Sharara field in Libya which produces as much as 300 tb/d. The news helped magnify nervousness over Houthi attacks in the Red Sea along with Lebanese tension and increased Russian operations in Ukraine. Despite the strength, the market appeared cautious, awaiting further supply threats to pursue an upside test of 76.00 resistance.

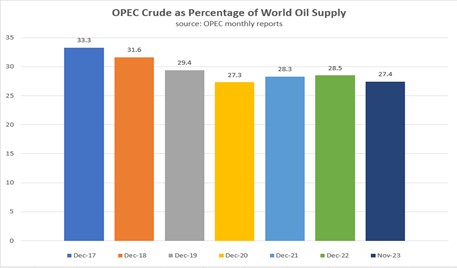

Unless additional supply threats occur, the market will remain cautious reflecting other macro influences related to the ability of OPEC to further support prices and the appearance that demand growth will continue to soften, particularly in China. Recent weakness in the nearby verses back months into contango has been symptomatic of better supply availability and will be watched closely given attempts at supply restraint by OPEC. Currently, OPEC production as a percentage of global supply has fallen to levels not seen since 2020 as non-OPEC production expands. This along with slowing demand growth is proving to be a challenge, with Angola showing its displeasure by withdrawing from the cartel because it did not serve their national interest. How OPEC+ navigates these turbulent waters remains to be seen and will be a key consideration for prices in the weeks ahead. Shipping data will be monitored to discern how effective the current agreement is at restraining supplies consistent with demand. The uncertain environment and fear of a broader conflict should limit selloffs despite weaker consumption trends on a seasonal and outright basis, suggesting a consolidative trend between 72 and 76 basis February might be apparent in the coming weeks. Signs that OPEC+ is taking more coordinated action to support values or an expansion in Red Sea hostilities could carry values up toward the 78-79 range

The DOE report to be released tomorrow is expected to show a draw in crude stocks of 3 mb and a build in distillate of .9 and in gasoline of .7. Refinery utilization is expected to fall .1 to 93.3 percent.

Natural Gas

Since our last report, prices have continued their steady push higher predicated on a normalization of temperatures in January that has lead to a recovery in demand expectations. The long term forecasts updated yesterday saw a substantial increase in HDD expectations as well, which added underlying support. Production being maintained near record levels over the holidays had offered overhead resistance, but a small drop under 108 bcf the last three days has been mildly supportive. Last week’s storage report showed an 87 bcf withdrawl, which was above estimates at 79, which firmed prices into the New Year’s weekend. With the 2.60 level violated today on the February settlement at 2.668, the 2.80 area becomes the target for bulls, which would achieve a 38 percent retracement of the November-December break. Decent support doesn’t arise until the 9-day moving average near 2.50. Tomorrow’s storage report estimates point to a 40 bcf withdrawl compared to the 5-year average decrease of 97.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.