Written Commentary

by market analysts Stephen Platt and Mike McElroy

Price Overview

The petroleum complex traded in a choppy fashion before settling lower, with crack margins also remaining under pressure. Nervousness in advance of the OPEC meeting along with high refinery utilization rates kept the overall tone negative.

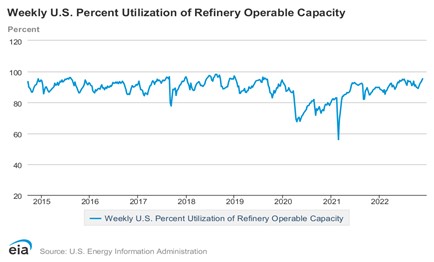

For the week basis January crude values are settling as much as 2.00 higher while product gains were far smaller at near 1 cent per gallon, or .5 per barrel for both diesel and gasoline. The increase in refinery throughput has taken refinery utilization up to the 95.2 percent in the week ended Nov 25th. This was the highest since August of 2019 when it reached 96.4 percent. With some refineries closed since then due to Covid, it will be interesting to see how high refinery utilization will reach this time around as export levels remain high for products but have recently been tempered for middle distillates.

Stock levels overall remain tight due to the heavy exports. The absence of additional SPR sales will continue to strain available supplies, keeping pressure on stocks. Although secondary inventories have built in anticipation of a contraction in Russian supplies as the embargo on Russian crude and the price cap go into effect, the recent improvement in availability is likely to be temporary as the Northern Hemisphere winter sets in. No help is likely to come from OPEC+ at their meeting on Dec 4th. Prices appear satisfactory, suggesting OPEC under-compliance will persist, with a rollover of the current agreement likely. We see further inventory declines leading to higher valuations in the intermediate term that could provide the basis for a retest of the 100.00 area in crude oil.

Natural Gas

Selling pressure remained steady over the last two sessions as the January contract lost 19 cents yesterday and followed that up with a drop of 45.7 cents today to end the week at 6.281. Recent forecasts calling for cold in the back half of 15-day outlooks have not materialized, with the 1-5 day showing significant HDD losses overnight to extend the downside bias. Model revisions this afternoon continued the bearish trend and pushed prices to end near their lows. Reports from Freeport that they were moving back their expected restart date to late January added to the weakness as it pushes 2 bcf/d of potential exports back onto the domestic market. Despite the extended shutdown, LNG flows have been solid, with yesterday’s nearly 13 bcf number the highest since before the Freeport fire. A pullback in production over the last to days to the 99 bcf area was another underlying supportive factor. Yesterday’s storage report was also seen as slightly positive, with the 80 bcf drawdown below expectations near 84. The decisive move through 6.50 brings the next level of support to the November lows near 6.13, with a settlement below there pointing to a target at the October lows at 5.645. A bounce higher will find initial resistance at 6.50 and beyond there in the 6.80-6.85 range.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.