Written Commentary

by market analysts Stephen Platt and Mike McElroy

Price Overview

The petroleum complex settled firm at 82.82 basis Sept up 1.27 following yesterday’s announcement by Saudi Arabia that they would extend the voluntary production cut of 1 mb into September and the Russian move to reduce exports by 300 tbd. In addition, a weaker than expected US jobs report also tended to provide background support on dollar weakness and weaker interest rates.

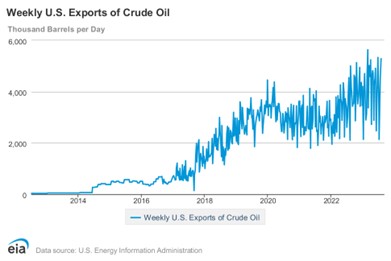

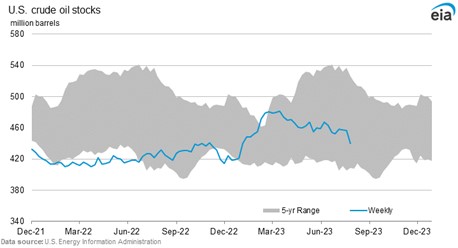

In the background, remains the sharp decline in US crude stock levels reported Wednesday. The failure to respond to the decline was surprising particularly ahead of the Saudi announcement the following morning. The decline in inventories, reflected heightened demand for US crude in the world market following the inclusion of Midland in June to set the price of the Dated Brent Benchmark assessed by S&P. This has helped spur rising crude exports that have displaced other crude grades in the world market. These US exports which reached 5.28 mb/d in the latest reporting week and have averaged 4.8 mb/d in 2023 against an average of 3.53 mb/d in 2022 are growing in importance. The widening exports show the increasing influence of crude from the US by easing the loss of supply from Saudi Arabia and Russia and increasing US market share on the world market in the pricing of North Sea blends

The declining market share of OPEC and particularly of Saudi Arabia might have consequences for the future by limiting their ability to respond to market movements that might be linked to other countries ability to expand production given higher price levels along with unforeseen economic forces, that might adversely impact demand.

Nevertheless, in the near term the sharp decline in US inventories given the buoyant demand for US crude does provide a tailwind to prices particularly in the US if it persists. Even modest declines in inventories will take us down toward historically low levels which should provide the basis for a move toward the 86 level basis prompt crude.

Natural Gas

Nat gas prices continued to attract light support to both cash markets and futures following the smaller than expected injection reported by the EIA yesterday of 14 bcf compared to an injection of 37 bcf last year and settled up 1.7 cents at 2.577 basis Sept. For next week, a larger injection is expected between 15-35 bcf but the appearance it should fall short of the five year average build of 46 bcf suggests the surplus is being eaten into which should provide support in the 2.50-2.55 range basis Sept. Given the uptick in crude and other commodities, continue to look for support to emerge and setbacks to be limited with potential to test the 20 day moving average near 2.716 basis Sept and potentially the 100 day moving average near 2.87 as cooling demand remains high into mid-month.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.