CORN

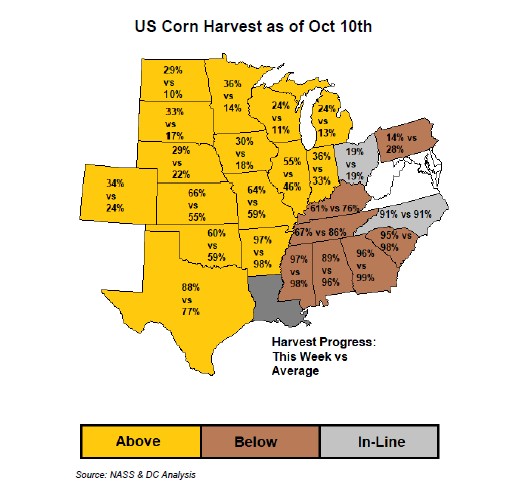

Corn futures closed lower. Managed funds increase selling below the 200 day moving average near 5.17. CZ ended near 5.12. Range was 5.02-5.25. Open interest has dropped from a high near 1,978,000 in Feb 2021 to near 1,400,000. Some of this is due to slowdown in US export traded and farmer selling. US Domestic cash basis is firming on a slowdown in farmer selling. Fact USDA estimated US 2021/22 corn carryout near 1,500 bu suggested to some that and harvest could limit new buying of futures. USDA estimates total US supply near 16,280 mil bu vs 16,055 last year. USDA did announce 161 mt US corn sold to unknown. Trade is still looking for additional corn sales to help support prices. USDA estimated US corn exports near 2,500 mil bu vs 2,753 last year. Some feel final exports could be closer to 2,700. USDA dropped US feed to 5,650 from 5,700. There are some that are concerned higher food and fuel inflated prices could reduce US disposable income and lower meat demand. USDA left US ethanol demand near 5.200 vs 5.032 last year. Margins are positive. Key will be EPA mandate and refiners waivers. Trend to green fuel vs fossil fuel should help ethanol demand. USDA est World corn trade near a record 202 mmt vs 178 last year. Still they raised end stocks from 297 mmt to 301 and vs 290 last year. USDA rated the US corn crop 60 pct G/E vs 59 last week. 41 pct of the crop is harvested vs 39 last year. Rains in the west could slow harvest. Drier weather in east could help harvest there.