Written Commentary

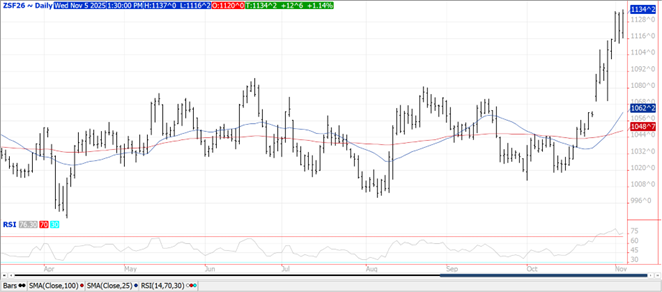

CORN

Prices were $.04-$.05 higher with spot Dec-25 posting its highest close in 4 months. Prices did however hold below last week’s low at $4.37. Chart support rests at the 100 day MA near $4.20. Spreads weakened. Ethanol production surged to a record high 1,123 tbd, or 330 mil. gallons in the week ended Fri. Oct. 31st, up from 321 mil. the previous week and up 1.6% from YA. Production was well above expectations. There was 112 mil. bu. of corn used in the production process, or 16 mil. bu. per day, well above the 15.36 mbd needed to reach the USDA corn usage estimate of 5.60 bil. bu. In the MY to date there has been 930 mil. bu. used, or 15.25 mbd, an annualized pace of 5.57 bil. Ethanol stocks rose to 22.7 mil. barrels, slightly above expectations while above YA at 22.0 mb. No USDA export sales tomorrow however traders est. sales last week to have ranged from 35-80 mil. bu. Sales should be holding up well as US FOB offers remain $5-$10 per ton below Brazil out to Feb-26.

SOYBEANS

Prices were higher across the complex with beans and meal making session highs in late trade. Beans were up $.10-$.14, meal was $7 higher while bean oil was up 15 points. Bean spreads weakened while product spreads firmed. Jan-26 beans traded to a fresh 16 month high. Dec-25 meal held just below Monday’s 9 month high at $325.20. Inside day for Dec-25 oil as it consolidates just below $.50 lb. While China has not confirmed the soybean volume figures the Trump Admin. has indicated they would purchase, they have announced the lowering of reciprocal tariffs on US imports including agricultural goods to 13% effective Nov. 10th. This still leaves the US at an economic disadvantage to Brazil who face only a 3% tariff, likely preventing large purchases of US beans. Deliveries against Nov-25 beans fell to only 4 contracts after holding at just over 200 contracts the previous few sessions. Spot board crush margins rebounded $.06 ½ to $1.41 ½ bu. while bean oil PV slipped back to 43.3%. Even without the tariff disadvantage US FOB offers are slightly higher than Brazil. Perhaps China is willing to buy US commodities at a premium as part of last week’s trade deal. Time will tell on that. Markets seem to be assuming they will. Markets are also bracing for a potential Argentine port workers strike, which may be contributing to the recovery in soybean meal. Lack of clarity on the Trump Admin. ability to reallocate lost biofuel demand onto Big oil due to SRE continue to cloud the demand picture for soybean oil.

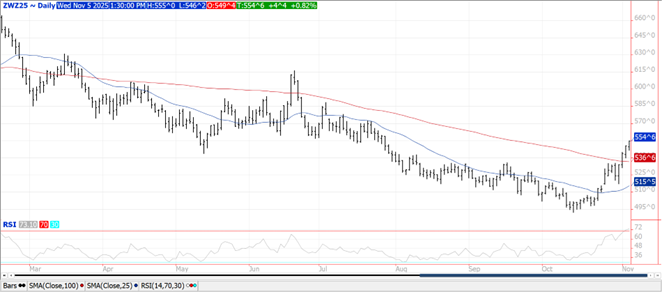

WHEAT

Prices were mixed today with CGO and KC $.04-$.05 higher while MIAX was off $.01. The Dec-25 contracts for both CGO and KC traded to fresh 3 month highs while also closing at session highs. The 100 day MA for both now serves as support after being overhead resistance for months. Dec-25 MIAX did hold 50 day MA support at $5.54 ¼. Speculative buying continues to fuel recent gains. Yesterday’s reported purchase of US SRW wheat by China brings their total purchases in the past week to nearly 500k mt. Perhaps weighing on prices in early trade were reports Russia’s Grain Union is considering doubling their grain export quota for the 2nd half of the 25/26 MY to 20 mmt, vs. only 10.6 mmt YA.

Charts provided by QST.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.