Written Commentary

CORN

Prices were $.01-$.03 higher led by old crop. Spreads are steady to higher. May-25 was not able to hold trade above LW’s high. Central and southern growing areas of Argentina are getting a break from weeks of heavy rain. Some showers have shifted into the northern growing areas, providing some relief from the heat, however overall precipitation totals are by no means a drought buster. The USDA announced the sale of 126k mt (5 mil. bu.) of corn to Japan. Export inspections at 72 mil. bu. were above expectations and a new MY high. They were also well above the 48 mil. bu. needed per week to reach the USDA forecast of 2.450 bil. bu. YTD inspections at 1.145 bil. are up 33% from YA vs. the USDA forecast of up 7%. Largest taker was Japan with 16 mil. Last week money managers sold nearly 118k contracts of corn slashing their long position to 220k. This was the 2nd largest amount ever sold in a 1 week period. Index funds also sold nearly 63k contracts, a record amount for a week. AgRural reports that Brazil’s 2nd crop is now 92% planted, up from 80% LW and just behind the YA pace.

SOYBEANS

Prices were lower across the complex with beans down $.08-$.12, meal was $1-$2 lower while oil was down 100-115 points. Spreads were weaker across the complex. Outside day down for May-25 beans with prices not able to hold above its 100 day MA. The early strength in May-25 meal was again capped near its 100 day MA at $307. May-25 oil slumped to a fresh 2 month lower however rebounded to close above the $.42 level. Spot board crush margins slipped $.06 to $1.16 per bu. with bean oil PV slipping to a fresh 2 month low at 41.1%. Conditions this week will be mostly favorable in Brazil with a favorable mix of rain and sunshine for much of the Center south region along with Mato Grosso in the WC region. Still net drying expected in the NE and very south in RGDS. The USDA announced the sale of 195k mt (7 mil. bu.) of beans to an unknown buyer. Export inspections at 31 mil. bu. were above expectations and well above the 10 mil. bu. needed per week to reach the USDA forecast of 1.825 bil. bu. YTD inspections at 1.412 bil. are up 10% from YA vs. the USDA forecast of up 8%. China took 10 mil. bu. Bean oil export commitments at 1.684 bil. lbs. already exceed the USDA forecast of 1.60 bil. for the entire 24/25 MY. Last week MM’s sold 99k contracts across the soy complex (44k beans, 33k oil, and 22k meal) the largest 1 week total ever reported. The MM position in beans has flipped back to net short 35.5k contracts. The MM long position in bean oil is back down to 10k contracts while their short position in meal has swelled back out to 85k contracts. AgRural reports that Brazil’s bean harvest advanced 11% to 61% complete as of last Thursday, vs. 55% YA.

WHEAT

Prices surged $.11-$.14 across all 3 classes today led by KC futures. May-25 KC traded to a fresh high for the month while challenging overhead resistance just above $5.80. May-25 CGO has MA resistance between $5.69-$5.74. In the US rains this week will favor the SE and to a lesser extent the Northern plains. Record high temperatures are expected for the Southern plains several days this week. With little to no rain combined with high winds between 50-75 mph late this week will likely produce blowing dust and possible power outages. Export inspections at 8 mil. bu. were below expectations and the 22 mil. needed per week to reach the USDA forecast. YTD inspections at 582 mil. are up 18% from YA, vs. the USDA forecast of up 20%. Last week MM’s sold 45k contracts across the 3 classes of wheat (18k KC, 15k CGO, 12k MGEX) the largest in 1 week in just over 7 years. Russia’s Ag. Ministry raised their wheat export tax 12% to 2,444 roubles/mt for the period ending Mch. 18th. IKAR reports Russia’s export price for wheat fell $1 last week to $247/mt. SovEcon reports Russian wheat exports last week at .31 mmt were slightly above the previous week total of .28 mmt. They est. total March exports between 1.4-1.8 mmt, well below the 4.8 mmt shipped in Mch-24 and would be the lowest for the month since 2020.

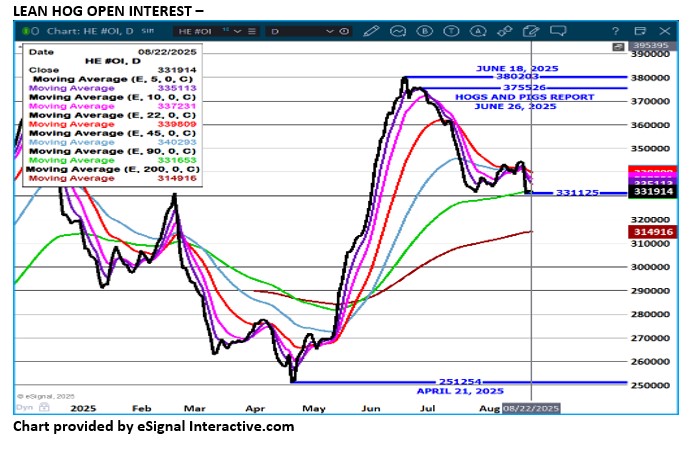

Charts provided by QST.

>>See more market commentary here.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.