Written Commentary

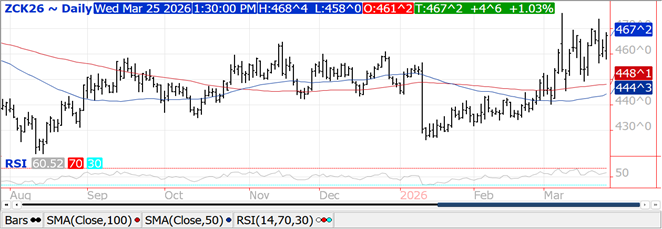

CORN

Prices were $.04-$.05 higher closing near session highs. Spreads also firmed. Both May-26 and Dec-26 contracts held support above this week’s low in early weakness. A midday announcement from the EPA issuing a waiver to allow the sale of E-15 during the summer months to help offset higher gasoline prices brought on by the war in Iran provided a boost. I’ve got Mch. 1st stocks pegged at a record 9.074 bil. bu. up from 8.147 bil. YA. USDA Sec. Rollins stated US farmers had secured 80% of their fertilizer needs for 2026 while the remaining 20% aren’t seeing much disruption due to the closure of the Straits of Hormuz. The EPA reported ethanol production rebounded to 328 mil. gallons LW, up from 321 mil. the previous week and up 6% YOY. There was 110 mil. bu. used in the production process, or 15.73 mil. bu. per day, just above the pace needed to reach the USDA forecast of 5.6 bil. Ethanol stocks rose to a 51-week high at 27.2 mil. barrels. Implied gasoline consumption rose 2.2% LW to 8.924 tbd and was up 3.3% YOY. Export sales tomorrow are expected to range between 28-32 mil. bu.

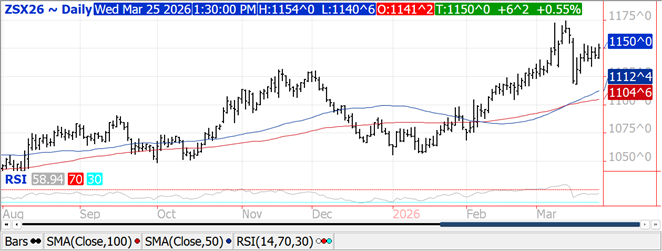

SOYBEANS

Prices were mostly higher but sharply mixed. Beans finished $.06-$.16 higher making new highs late after news the President Trumps trip to Beijing has been rescheduled for mid-May. Meal was $1-$2 lower while oil was 100-135 points higher. Bean and oil spreads firmed while meal spreads weakened. May-26 beans rejected trade into new lows for the week while trading into new highs late. May-26 meal slumped to new lows for the week with next support at the 100-day MA at $314. May-26 oil has jumped out to new highs for the week anticipating supportive news from the EPA. Moderate speculative buying this week will likely show MM’s holding a record long position in soybean oil at roughly 137k contracts. Spot board crush margins fell $.07 ½ to $2.70 per bu. with bean oil PV jumping to 51.2%. Anec forecasts Brazil will export 15.9 mmt of soybeans in Mch-26, while down from their previous forecast of 16.3, it would still represent an all-time high and above the 15.3 mmt shipped in Mch-25. My Mch. 1st stocks forecast is 2.116 bil. bu. vs. 1.911 bil. YA. . With Trump’s trip to Beijing being rescheduled for mid-May certainly improves prospects for additional purchases, however I feel will likely wind up as new-crop sales. It will take higher energy prices or old crop purchases from China to drive spot soybeans back to $12 bu. Export sales are likely to range from 8-22 mil. bu. of beans, 150-400k tons of meal and -15k – 25k tons of oil.

WHEAT

Prices ranged from $.07 higher in CGO to $.13 higher in KC. Spreads also firmed as fund buying took over. Both CGO and KC held support just above this week’s low in early weakness. The 6-10 and 8-14 day outlooks show above normal precipitation across the US plains, which would be of great benefit to the winter crop emerging from dormancy. Algeria is tendering for 50k mt of milling wheat with the deadline tomorrow. Historically they tend to purchase much more than the announced tender volume. Acres have fallen from January to March 3 of the past 4 years. SovEcon raised their Russian export forecast for 25/26 MY 1.1 mmt to 46.5 vs. the USDA est. of 43.5 mmt. They also raised their forecast for 26/27 MY 2.1 mmt to 43.8. Export sales are expected to range from 5-22 mil. bu.

Charts provided by CQG

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.