Written Commentary

CORN

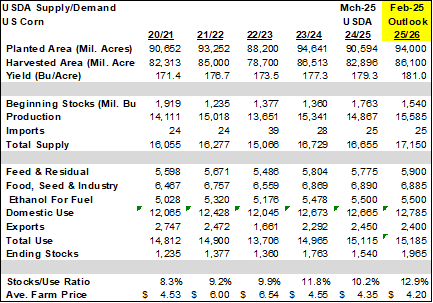

Prices were not able to hold the higher trade from midday setting back to close $.01-$.02 lower led by old crop. Spreads weakened into the close. Next support for May-25 is the 100 day MA at $4.64 ½, followed by last week’s low at $4.42 ½. Central and southern growing areas of Argentine will continue to dry down following 2 weeks of heavy precipitation. Look for corn harvest to accelerate the 2nd half of March after holding at just below 7% late last week. While drought still persists across the NE growing areas, cooler temperatures have provided modest relief. US ending stocks were left unchanged at 1.540 bil. bu., 25 mil. above expectations. Global stocks were cut 1.4 mmt to 288.9 mmt. There were no changes to Brazil or Argentine production forecasts holding at 126 and 50 mmt respectively. Brazil’s exports cut 2 mmt to 44 mmt as a greater portion of their crop is being used domestically for biofuel production. Chinese imports were cut 2 mmt to 8 mmt. Mexico’s imports held steady at 24.5 mmt.

SOYBEANS

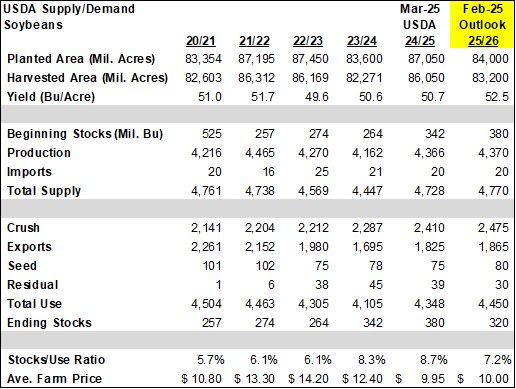

Prices slipped late closing slightly lower across the complex. Beans were down $.02-$.03, meal less than $1 lower while oil was 30-35 lower. Spreads were weaker across the complex as well. Support for May-25 beans is at LW’s low at $9.91 with overhead resistance at its 100 day MA at $10.28 ½. May-25 oil closed into new 2 month lows with next support at 41.44. May-25 meal seems stuck between $300 and its 100 day MA at $307. Spot board crush margins slipped another $.02 to $1.14 bu. while bean oil PV reached a 2 ½ month low at 41%. Mostly favorable conditions in SA. Much of Brazil will see a good mix of rain and sunshine over the next week to 10 days. East central into NE growing areas will continue to experience a net drying trend. US ending stocks were left unchanged at 380 mil. bu. however the Ave. farm price was cut $.15 to $9.95 per bu. Stocks were in line with expectations. Bean oil usage for biofuels was cut 150 mil. lbs. to 13.450 bil. while exports rose 200 mil. lbs. to 1.80 bil. lbs. Global stocks were cut 3 mmt to 121.4 mmt, vs. expectations of no change. Argentine and Brazilian production forecasts held steady at 49 and 169 mmt respectively. Argentine crush was increased 1 mmt to 42 mmt, while meal exports were increased 3.5% and oil up 8%. Chinese crush was raised 2 mmt to 105 mmt however no change to the supply side of the equation.

WHEAT

Inside trading session as prices finished $.05-$.07 lower across the 3 classes. Spreads were steady to slightly weaker. US ending stocks rose 25 mil. to 819 mil. bu. vs. expectations for no change. HRS and durum stocks both rose 10 mil. bu. while SRW was up 5 mil. Imports were revised up 10 mil. while exports were trimmed by 15 mil. Global stocks rose 2.5 mmt to 260 mmt vs. expectations of no change. Australian production was increased 2.1 mmt to 34.1 mmt while their exports were up 1 mmt. Russian exports were cut .5 mmt to 45 mmt while Chinese imports were cut 1.5 mmt to 6.5 mmt. In the US, precipitation this week will favor the SE and to a lesser extent the Northern plains. Record high temperatures are expected for the Southern plains several days this week. With little rain and wind speeds between 50-75 mph late this week drought conditions are expected to expand rapidly. Headlines after the close of trade indicate peace talks in Saudi Arabia between the US State Dept. and Ukrainian officials were constructive with a cease fire offer on the table. Pres. Trump went on to state he would welcome Pres. Zelenskiy back to the White House to discuss plans for lasting peace and a critical mineral deal. Trump also stated he’s considering reducing tariffs on Canada now.

Charts provided by USDA.

>>See more market commentary here.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.