Written Commentary

SOYBEANS

The soybean complex finished lower across the board with beans off $.30 – $.32, meal was $6 – $9 lower, while oil was down 30 – 60. I look for Nov-23 soybeans to find support before reaching the $13 to $12.90 (100 day MA) area. Ahead of today’s reports the USDA announced the sale of 105k tons of new crop 23/24 soybean meal to an unknown buyer. Old crop soybean ending stocks rose 25 mil. bu. to 255 mil. vs. expectations for a 5 mil. bu. increase. As we expected exports were cut 20 mil. bu. to 1.980 bil. however virtually no change to residual/seed usage. Imports were increased 5 mil. to 25 mil. bu. As we expected the USDA made no change to their 2023 yield forecast of 52 bpa. Production fell 210 mil. to 4.30 bil. as a result of the lower acres. The USDA was aggressive in cutting new crop demand by 135 mil. bu. with exports down 125 mil. and crush down 10 mil. The Ave. Farm price rose only $.30 to $12.40 bu. Ending stocks fell only 50 mil. to 300 mil. bu. vs. expectations of 205 mil. We were estimating ending stocks at 225 mil. No significant changes to either the meal or oil balance sheets. Global 2022/23 ending stocks rose 1.6 mmt to 103 mmt, above expectations. Chinese imports were increased 1 mmt to 99 mmt, however new crop imports were cut 1 mmt. The USDA made no production changes to either Argentina or Brazil leaving their est. at 25 mmt and 156 mmt respectively. New crop global stocks fell 2.3 mmt to 121 mmt, however still a record high. US production losses were the reason for the global supply drop. The USDA lowered Chinese imports 1 mmt for the 2023/24 MY. Export sales tomorrow expected to range from 10 – 30 mil. for soybeans, 100 – 300k tons meal, and 0 – 10k tons oil.

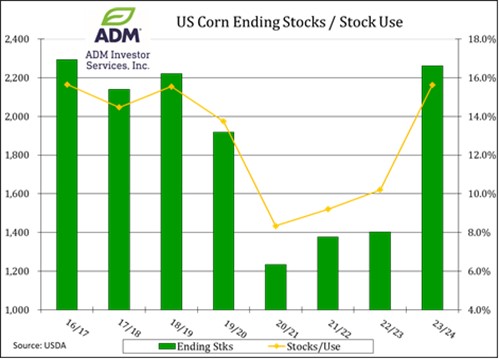

CORN

Prices finished $.16 – $.18 lower with Dec-23 closing at its lowest level since Oct-21. Next support is $4.62 ½. Ahead of today’s USDA reports weekly ethanol production slipped to 1,032 tbd, down from 1,060 tbd the previous week. Production was below expectations helping justify the USDA usage reduction. Implied gasoline consumption last week was down 8.8% from the previous week, however up 8.6% from same week YA. US 2022/23 corn ending stocks were cut 50 mil. bu. to 1.402 bil. slightly below expectations. As expected feed/residual usage rose 150 mil. bu. which was partially offset by a 75 mil. bu. cut in exports and 25 mil. drop in usage for ethanol production. Pretty much what we expected with the exception we were looking for only a 50 mil. bu. cut in exports. 2023 production rose 55 mil. bu. to a record 15.320 bil. as the 2.1 mil. more acres more than offset the 4 bpa drop in yield to 177.5 bpa. We were looking for a 5 bpa yield reduction. New crop demand was left unchanged with ending stocks at 2.263 bil., roughly 100 mil. above expectations. If realized new crop ending stocks and stocks/use ratios would be the highest in 7 years. The new crop 23/24 Ave. Farm price held steady at $4.80 bu. Old crop global stocks fell just over 1 mmt to 296.3 mmt, slightly below expectations. A 1 mmt cut in Argentine production was offset by a 1 mmt increase in Brazil. Exports were increased by 1 mmt for both Brazil and Ukraine, with Argentina’s exports falling another 1 mmt. New crop 2023/24 global stocks rose fractionally, in line with expectations. Export sales tomorrow are expected to range from 10 – 25 mil. bu. Corn needs to find a price level that stimulates better demand. Conditions are likely to continue to improve with Dec-23 slipping below $4.60. Continued rain across the nation’s midsection will continue to ease drought concerns in the highest yielding areas. Still too dry across the northern Midwest and northern plains. Threats of above to MA normal temperatures next week will be monitored closely.

WHEAT

Prices were lower across all 3 classes with MGEX down $.08 – $.10, KC $.13 – $.15 lower, while Chicago was off $.24 – $.28. Chicago Dec-23 traded down to the lowest level in a month. KC Dec-23 closed back below 50 and 100 day support, however held above the July low of $7.91. Dec-23 MGEX held above 100 day MA support at $8.48 ¼. We look for MGEX to perform best among the 3 classes. All wheat production rose 74 mil. bu. to 1.739 bil., 56 mil. bu. above expectations. Winter wheat rose 74 mil. bu. to 1.210 bil., nearly 65 mil. above expectations and above the range of est. We weren’t that far off with our est. at 1.187 bil. By class changes were HRW up 52 mil., SRW up 20 mil. and white down 2 mil. Spring wheat production at 479 mil. bu. just below YA at 482 mil. and in line with expectations. We hold a lower production bias going forward for spring wheat. 2023/24 US ending stocks rose 30 mil. bu. to 592 mil. as higher feed usage partially offset the increased production. The Ave. Farm price fell $.20 to $7.50 bu. World stocks for 2023/24 fell 4 mmt to 266.5 mmt, roughly 3 mmt below expectations. Production cuts include Argentina and Canada both down 2 mmt, while EU was lowered 2.5 mmt. Export sales tomorrow expected to range from 8 – 16 mil. bu.

See more market commentary here.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.