Written Commentary

CORN

Prices were $.02-$.03 higher today consolidating within this week’s range while adding some weather premium ahead of tomorrow’s USDA data. Spreads were little changed. Above to much above normal precipitation pattern for central and northern growing areas of Brazil may delay the early start to soybean harvest while pushing back corn plantings. Wire services are reporting that Algeria made no significant purchase of corn from their recent tender for 240k mt. History has shown a bit of a bullish bias on January report day. Since 2000 spot March futures have closed higher 14 times (58%), while closing lower 11 times. The last time we had a limit move was 2012 when corn broke $.40. Export sales tomorrow are expected to range from 28-55 mil. bu.

SOYBEANS

Prices were mixed across the complex with beans $.02-$.03 higher in 2 sided trade. Meal was down $2-$3 while oil was up 80-90 points. Beans spreads were steady while product spreads rebounded. Hot/dry conditions are likely to continue from Central Argentina into Southern Brazil for another week. By late next week and weekend some relief appears likely in the form of scattered showers. Moisture totals of .50-1.0” are likely with some areas picking up 1-2” totals. Midday forecasts however seemed a bit less confident in rainfall coverage than the overnight models. Weakening basis levels in Brazil continue to limit the upside potential. Mch-25 bean oil surged thru its 100 day MA resistance at midday stopping just shy of its 50 day MA at 42.96. Mch-25 meal continues to consolidate near the $300 level and its 50 day MA. Spot board crush margins rebounded $.05 to $1.29 3/4, bu. while bean oil PV jumped to 41.7% a fresh 4 week high. History has shown a bullish bias on January report day for soybeans. Since 2000 spot March futures have closed higher 15 times (60%), while closing lower 10 times. Export sales tomorrow are expected to range from 15-45 mil. bu. for soybeans, 200-400k tons of meal, and 15-50k tons of oil.

WHEAT

Prices were $.03-$.04 lower across all 3 classes today. The next winter storm is bringing a mix of snow and ice across central and northern TX. All snow in OK and SE KS. As the system moves northeast, it will bring snow to the N. AR/S. MO thru the central Midwest and ECB by Friday night. With fresh news limited, prices quickly pulled back from the mini rebound stimulated by the lower US winter crop ratings earlier this week. Although the speculative trade remains fairly heavily short in wheat, the market lacks a spark needed to ignite a short covering surge. History shows wheat has the strongest upward bias on January report day. Since 2000 spot March futures have closed higher 17 times (68%), while closing lower 8 times. Export sales tomorrow are expected to range from 6-20 mil. bu.

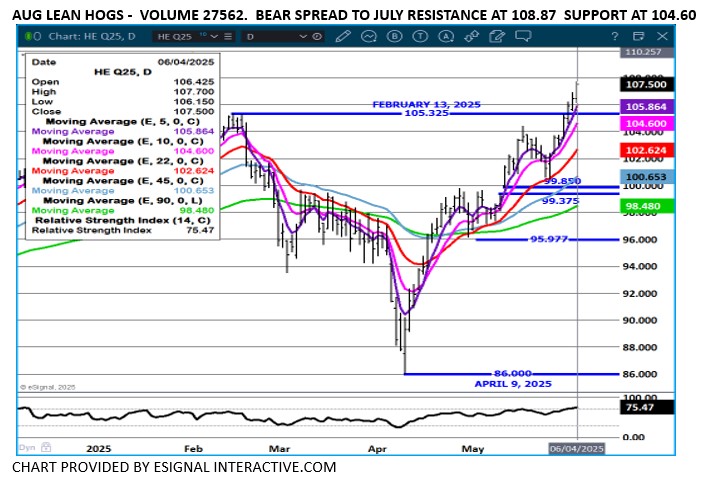

Charts provided by QST.

>>See more market commentary here.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.