Written Commentary

SOYBEANS

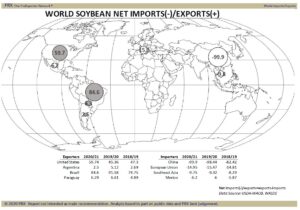

Soybeans closed higher. Overnight trade was higher in anticipation that USDA would drop South America soybean crops, raise US soybean demand and lower US soybean carryout. They did increase US soybean exports 20 mil bu but failed to lower South America crops. Most feel final US demand could even be higher and that futures need to trend higher to slow demand. Higher palmoil prices and fact USDA lowered US soyoil end stocks due to higher biodiesel demand helped rally soyoil futures. USDA estimated US soybean carryout near 120 mil bu versus 123 expected and 140 last month. USDA also estimated World soybean carryout near 83.3 mmt versus 83.3 expected and 84.3 last month. Some feel final South America soybean crop could be 5-6 mmt lower than USDA Feb guess. USDA left average on farm soybean price near 11.15 versus 8.57 last year.

CORN

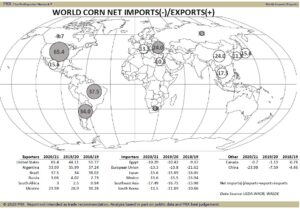

Corn futures traded lower after the USDA Feb report. Many analyst and traders were left confused after US dropped US corn carryout only 50 mil bu, raised China corn imports but at the same time, raised China corn end stocks. USDA numbers did little to reflect where the market is as far as US supply and where prices need to trade to ration demand. Some now even doubt USDA will increase US corn exports, domestic demand and lower the carryout on their March guess. They may wait for more South America harvest data, China demand and March US 2021 acreage and stocks report to make changes. USDA estimated US corn carryout near 1,502 mil bu versus 1,392 expected and 1,552 last month. USDA estimated World corn carryout near 286.5 mmt versus 279.8 expected and 283.8 last month. USDA estimated China corn imports at 24.0 versus 20.0 expected. USDA raised China corn end stocks to 196 mmt versus 191 previous and UN FAO last estimate of 139. Some feel final South America corn crop could be 6-7 mmt lower than USDA Feb guess. USDA raised average on farm corn price to near 4.30 versus 3.56 last year.

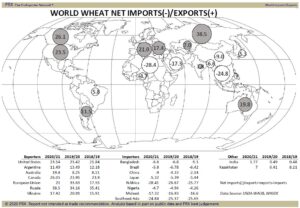

WHEAT

Wheat futures traded lower. USDA did drop World wheat end stocks due to lower China end stocks but kept US carryout unchanged. Wheat futures have seen resistance due to increase Russia farmer selling and increase Russian offers for exports. Both are trying to get ahead of new Russia export tax policy which could slow Russia exports and the intent is to preserve domestic supplies and lower domestic prices. USDA estimated US wheat carryout near 836 mil bu versus 834 expected and 836 last month. USDA did raise US HRW end stocks from 334 mil bu to 362 and 506 last year, left US SRW end stocks near 100 mil bu and lowered HRS end stocks to 258 from 279 and 280 last year. USDA estimated World wheat carryout near 304.2 mmt versus 312.8 expected and 313.2 last Month. USDA raised average wheat farm price to 5.00 from 4.85 and 4.58 last year.