Written Commentary

CORN

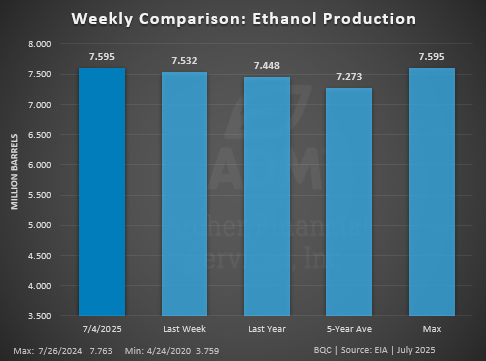

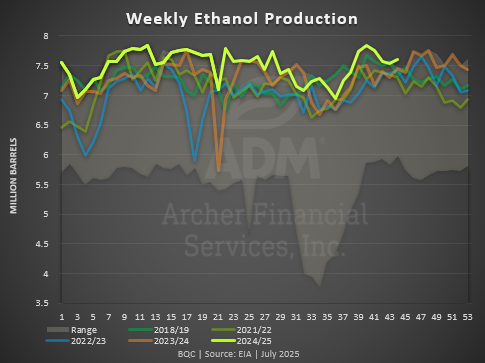

Prices closed $.03-$.06 higher in choppy 2 sided trade led by old crop. Spreads also firmed. Mch-25 was not able to penetrate LW’s high at $4.97 ½. The next major resistance is at $5.08 ¼, the high from last May. While imposing retaliatory tariffs on some US goods, China spared agricultural commodities perhaps suggesting they are willing to negotiate with the Trump Administration on a new trade agreement. Pres. Xi and Trump were expected to speak by phone today, however at midday the WSJ reported the 2 global leaders would not speak today. Rains are expected to start filling in over some of the dryer areas in EC Argentine this week with coverage and overall totals crucial in providing relief from recent drought stress. The USDA announced the sale of 132k mt (5.2 mil. bu.) to South Korea. Corn used in the production of ethanol in Dec-24 rose slightly to 473 mil. bu. however, was down 2.3% YOY. The Nov-24 usage figures were revised up by 7 mil. bu. Usage in the first 4 months of the MY has reached 1.860 bil. bu. up 1.5% from YA, vs. the USDA forecast of up less than 1%. The USDA is currently est. production at 127 mmt. EU 24/25 corn imports as of Feb. 2nd have reached 11.92 mmt, down 4.6% from YA.

SOYBEANS

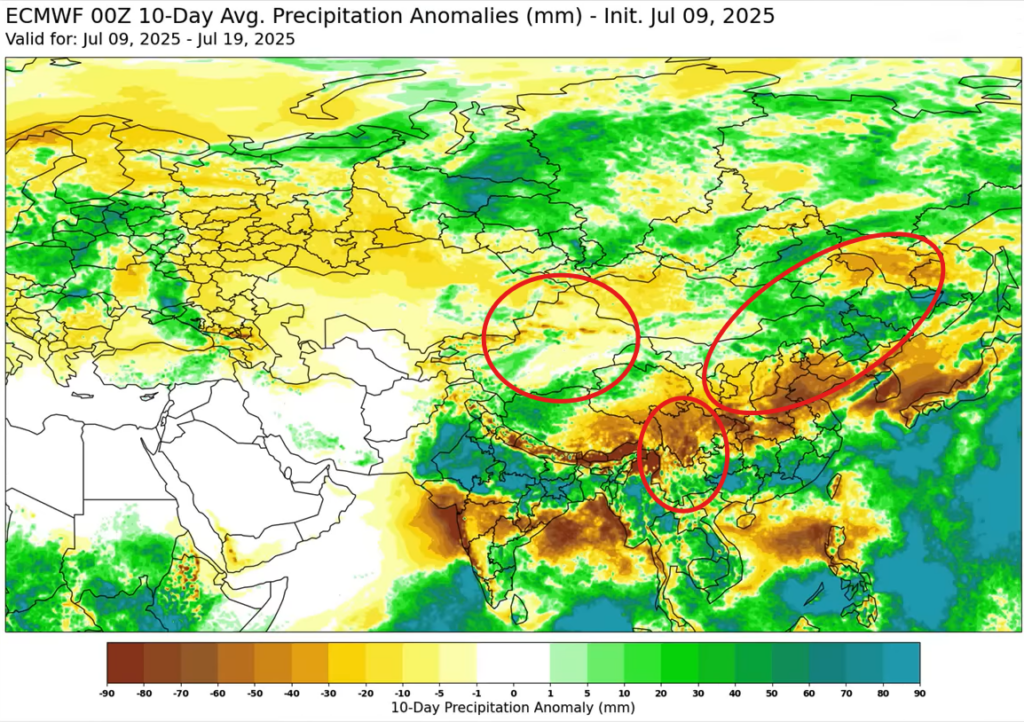

Prices were mixed today with beans $.10-$.17 higher led by old crop, meal surged $9-$10 while oil was down 65-75. Spreads firmed in beans and meal, while nearby oil spreads traded to new lows. Mch-25 soybeans seemed to stall after trading into a fresh 4 month high. The next resistance is the Sept-24 high at $11.00 ¼. Mch-25 oil plunged in overnight trade following the postponement of the Canadian tariffs and perhaps disappointment the US didn’t target UCO imports from China for higher tariffs. Prices recovered nicely by midday, rejecting trade below $.45 lb. Mch-25 meal surged thru its 100 day MA resistance while also closing a gap from late Jan-25. Next resistance is the Jan-25 high at $321.60. Spot board crush margins dipped $.02 to $1.19 ½ bu. while soybean meal PV surged to 57.8%. Central and northern crop areas in Argentina will likely experience an extended hot/dry pattern. Rains across central and WC Brazil are expected to lighten up thru the upcoming weekend allowing some bean harvest and corn plantings to resume. Normal to above normal precipitation however is expected in week 2 of the outlook. Late yesterday Celeres raised their soybean production forecast for Brazil by just over 3 mmt to 174 mmt despite harvest delays driven by wetter than normal conditions in the EC and growing regions. The USDA confirmed a record 218 mil. bu. of soybeans were crushed in Dec-24. This was in line with expectations and just above the previous record of 216 mil. bu. in Oct. of last year. In the first 4 months of the 24/25 MY cumulative crush at 830 mil. bu. is up 6.3% from YA, vs. the current USDA forecast of up 5.4%. Bean oil stocks rose to 1.696 bil. lbs. up nearly 5% from Nov-24, however slightly below expectations. EU soybean imports at 8.27 mmt as of Feb. 2nd are up 13% from YA. Meal imports at 11.42 mmt are up 28%. Overnight trade will be eagerly awaiting any breaking news from Pres. Trump and Chinese Pres. Xi phone conversation (if it happens) along with rain results in Argentina.

WHEAT

Prices closed higher across all 3 classes with Chicago and KC the upside leaders posting gains of $.08-$.10. MGEX was up $.05-$.06. Chicago Mch-25 close above its 100 day MA resistance for the first time in nearly 4 months. Mch-25 KC closed at a 3 ½ month high. Mch-25 MGEX rebounded back to close above its 100 day MA at $6.15 ½. I’ll be eager to see if open interest dropped with today’s higher trade, and indication of a short covering rally, or jumped as end users expand forward coverage. Jordan passed on making any purchases in their most recent 120k mt wheat tender. EU soft wheat exports as of Feb. 2nd at 12.5 mmt are down 37% from YA. SovEcon is projecting Russian wheat exports in 24/25 at only 42.8 mmt, well below the USDA forecast of 46 mmt. SovEcon is also reporting that the average domestic price for wheat in Russia has risen 9% in 2025 to $158/mt. Winter wheat ratings improved 3% in KS over the past month to 50% G/E, however slightly below YA at 54%. Ratings also improved in MT and SD while slipping in OK, TX, CO and NE.

Charts provided by QST.

>>See more market commentary here.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.