Written Commentary

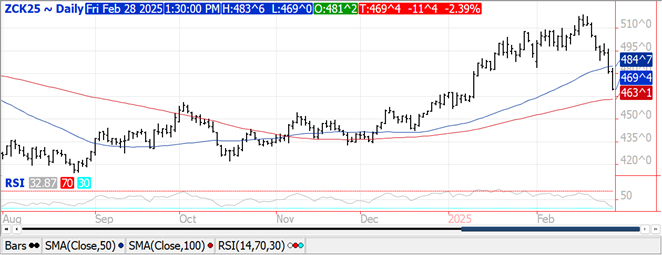

CORN

Prices plunged another $.07-$.11 today as speculators continue to shed length at month end. Spreads were choppy as Mch/May slipped to a fresh low at $.17 ½, despite the lack of deliveries, before recovering to close steady. May-25 violated support at $4.80 finishing the week down $.35 while down nearly $.25 for the month. Next support is the 100 day MA, currently $4.63. Today’s Washington drama that unfolded between Pres. Trump, VP Vance and Ukrainian Pres. Zelensky seemingly had little impact on agricultural prices. Zelensky left the White House without signing a mineral rights deal with the US while peace negotiations are seemingly on hold. Heavy rains will continue to track across Southern Cordoba and Sante Fe, Northern La Pampa and northern half of Buenos Aires over the next week. Rains total likely to vary between 4-10” with localized flooding possible. The BAGE reports Argentina conditions improved 1% LW to 71% G/E. Harvest progress is reported at 5.4% up 3% for the week and well above YA pace at 1.7%. Since July-24 Ukraine’s corn exports for the 24/25 MY have reached 14.4 mmt, down 9% YOY. US corn remains competitively priced in the global marketplace into July.

SOYBEANS

Prices were mostly lower with beans down $.12, meal was steady while oil plunged over $.01 lb. Spreads were steady to firm in beans and meal, while mostly lower in the oil. May-25 beans traded to a 7 week low, closing at session lows while violating support at both the 50 and 100 day MA’s. Same story for May-25 oil. New 2 ½ month low for May-25 meal in early trade before rebounded to closed unchanged. Spot board crush margins were little changed at $1.09 bu. while bean oil PV fell to a 5 week low at 42.7%. SA weather will still feature dry conditions across N. Argentina into Southern Brazil and along Brazil’s EC and NE growing areas for at least another week. Late season crop stress will be on the rise. The BAGE reports Argentina bean conditions improved 7% LW to 24% G/E while holding their production forecast at 49.6 mmt. Combined biodiesel and RD production fell 3.6% in Dec-24 443 mil. gallons and up only 1.7% YOY. Combined capacity has been unchanged all of Q4 2024 at 6.575 bil. gallons annually. Bean oil usage slipped 8% to 1.097 bil. lbs. in Dec-24. Usage over the 1st 3 months of the 24/25 MY at 3.516 bil. lbs. is up 7.6% YOY, vs. USDA forecast of up 4.7%. Bean oil as a % of feedstock used slipped to a 5 month low at 33.6%. Still a lot of uncertainty on biodiesel and RD policies moving forward with the Trump Administration. Census crush from Jan-25 scheduled for release after the close on Monday is expected to show 211 mil. bu. of beans processed during the month, down from a record of 217.7 mil. in Dec-24. Oil stocks are expected to rise to 1.757 bil. lbs. up from 1.696 bil. at the end of Dec-24.

WHEAT

Prices were $.07-$.13 lower across all 3 classes today with KC the downside leader. New monthly lows across all 3 classes for the May-25 contracts with losses approaching $.50 for the week. No telling where Ukraine/Russian peace talks go from here however the uncertainty will likely keep volatility high. Russia’s Ag. Ministry lowered their wheat export tax 21% to 2,178 roubles/mt in the period ending March 11th. Ukraine exports since July-24 at 11.9 mmt are still up 3% YOY. The central US will see little precip. over the weekend except for a lite mix of snow/rain in the Great Lakes region. The next storm event will begin to form in the SE plains early next week. As this system slides NE, it’s expected to bring 1-2” of rain for much of the central and ECB. Lighter amounts for the WCB with little precip. for the Northern plains. Following 3 weeks of short covering the speculative trade appears to be reloading on the short side of the market as US weather is currently non-threatening.

Charts provided by QST.

>>See more market commentary here.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.