Written Commentary

CORN

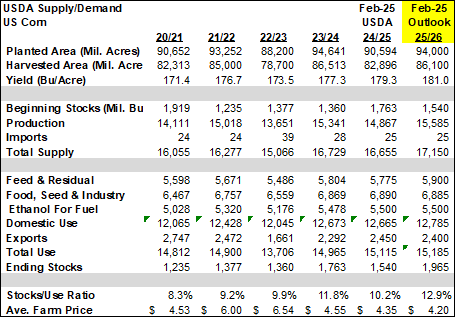

Prices were $.06-$.13 lower today with spreads also weakening. Mch/May dropped to a new low at $.16 ¾ ahead FND. May-25 dropped to a new low for the month while also plunging thru its 50 day MA support at $4.84 ½. Exports at 31 mil. bu. were at the low end of expectations. Old crop commitments at 1.916 bil. up 28% from YA, vs. the USDA forecast of up 7%. Current commitments represent 78% of the USDA forecast, above the historical average of 71%. Noted buyers were Mexico – 15 mil. while Japan and Colombia bought 7 mil. each. The USDA Outlook Conf. pegs 2025 corn acres at 94 mil. up 3.4 mil. from YA. With a trendline yield at 181 bpa production would reach 15.585 bil. with ending stocks building to 1.965 bil., roughly 50 mil. above expectations. US corn acres in drought surged 11% this past week to 56%, well above the 31% from YA. Bulls would agree 2025 drought watch is on, bears would argue spring plantings will go quickly. Today’s price action would suggest the market is attempting to switch some corn acres back to soybeans.

SOYBEANS

Prices gave way to the sharply lower trade in the feed grains finishing lower across the board. Beans were down $.02-$.05, meal was $2.50 lower while oil was off 25 points. Spreads were steady to firm across the complex. May-25 bean carved out a fresh low for the month with next support at its 100 day MA at $10.32. May-25 meal was consolidating near $300 ton. May-25 oil rejected trade above yesterday’s high before pulling back. Exports at 15 mil. bu. were in line with expectations. YTD commitments at 1.622 bil. are up 14% from YA vs. the USDA forecast of up 8%. Commitments represent 89% of the USDA forecast, above the historical average of 87%. For now still thinking exports are on hold at 1.825 bil. bu. Outstanding sales to China/unknown fell to 164 mil. vs 146 mil. YA. Meal sales at 177k tons were below expectations. YTD commitments are up 12% from YA, vs. USDA up 8%. Bean oil sales at 18k mt (41 mil. lbs.) were in line with expectations. YTD commitments at 1.563 bil. lbs. represent 98% of the USDA forecast. The USDA Outlook Conf. pegs 2025 bean acres at 84 mil. down 3.1 mil. from YA. With a trendline yield at 52.5 bpa production would reach 4.370 bil. with ending stocks falling to 320 mil., roughly 60 mil. below expectations. The Outlook Conf. is projecting 2025 US farm exports will reach $170.5 bil. down from $174.4 bil. in 2024. This year’s exports include $30.2 bil. to Mexico, $28.4 bil. to Canada and $22 bil. to China. Ag. imports are expected to rise 6.5% to 219.5 bil. US bean acres in drought surged 10% to 46%, well above the 28% from YA. The BAGE reports Argentine crop ratings jumped 7% LW to 24% G/E while poor/VP ratings fell 1% to 33%.

WHEAT

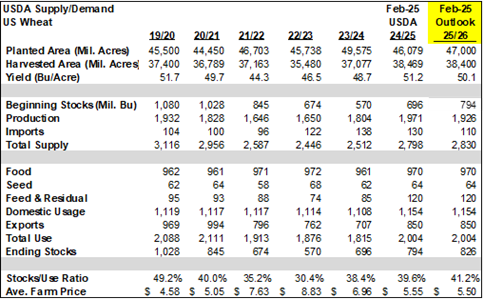

Prices plunged $.13-$.19 across all 3 classes today with Chicago the leader to the downside. All 3 May-25 contracts fell to fresh lows for the month. SRW spreads in Chicago plunged with Mch/May reaching a new los at $.16 ½. Exports at 10 mil. bu. were at the low end of expectations. YTD commitments at 733 mil. bu. are up 10% from YA, vs. the USDA forecast of up 20%. Commitments represent 86% of the USDA forecast vs. the historical average of 88%. By class commitments vs. the USDA forecast are HRW up 47% vs. USDA up 57%, SRW down 35% vs. down 21%, HRS up 6% vs. up 15% and white up 45% in line with the USDA forecast. The USDA Outlook Conf. showed 2025 wheat acres at 47 mil. up .9 mil. from YA. With a trendline yield at 50.1 bpa production would reach 1.926 bil. with ending stocks rising to 826 mil. all near trade expectations. The CME held the maximum storage rate unchanged for CGO SRW wheat at $.00265 per day, or roughly $.08 per month. The maximum rate for KC HRW wheat was also left unchanged at $.00165 per day, or roughly $.05 per month. Following 3 weeks of short covering the speculative trade appears to be reloading on the short side of the market as US weather is currently non-threatening. Pres. Trump today stated talks to end the Ukraine/Russia war are going well and believes that if a peace deal is struck, Russian Pres. Putin would honor the agreement and not attempt another invasion.

Charts provided by QST.

>>See more market commentary here.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.