Written Commentary

CORN

Prices were $.01-$.04 ½ lower with losses being led by old crop. After trading to a fresh 9 month high in early trade, old crop futures turned lower with spot Mch-25 dipping back below the $5.00 level. Key resistance for spot futures rests between $5.08-$5.10. Spreads also weakened with Mch/May trading to a new low at $.14 ¾ on a likely pickup in farmer selling. New crop Dec-25 had traded to a fresh 8 month high as it works to buy in additional US acres this Spring. In Brazil good rains over the past 24 hours have slowed soybean harvest and 2nd corn plantings in SC regions of Parana, Sao Paulo and MGDS. Good progress is likely being made in Mato Grosso before the next wave of rain late this upcoming weekend. Areas in the EC and NE along with RGDS in the deep south are expected to remain in a dry pattern for the next week. US demand remains stout with yesterday’s export inspections a MY high. EIA ethanol production is delayed until tomorrow due to Monday’s holiday. Production is expected to fall within a range from 309-317 mil. gallons, down from 318 mil. last week. Export sales and cattle on feed on Friday.

SOYBEANS

Prices were mostly lower with beans down $.06-$.08, meal was steady to $1 higher, while oil was down 80-100 points. Bean and meal spreads were steady to higher while oil spreads weakened. Technical support for Mch-25 beans rests just below the market where the 50 and 100 day MA’s converge just above $10.20. Mch-25 meal held support above LW’s low at $291.60 setting up today’s bounce. Mch-25 oil jumped out to a 3 ½ month high overnight however rejected trade above $.48 lb. while falling back to close just above $.46. Spot bean oil PV closing at a 3 month high yesterday at 44.6%, falling back to 44% today. Spot board crush margins slipped $.02 ¼ to $1.26 bu. Brazil keeping their mandatory biodiesel blend rate at 14%, rather than increase to 15% as previously expected, provided the fundamental reasoning for today’s pullback. Despite yesterday’s NOPA crush coming in below expectations at just over 200 mil. bu., it was the 2nd highest ever. In Argentina rainfall over the next week will favor the south, bringing relief to areas that missed out on recent rain activity. Following weekend rains the central and northern growing areas will see dry conditions for the next week to 10 days which may reignite dry concerns. ANEC is forecasting Brazilian soybean exports in Feb-25 will reach 9.72 mmt, while down from their previous forecast of 10.1 mmt it would still be a record high for the month, well above last year’s record of 6.6 mmt. AgroConsult lowered their Brazilian production forecast by 1.1 mmt to 171.3 mmt, just above the USDA forecast of 169 mmt.

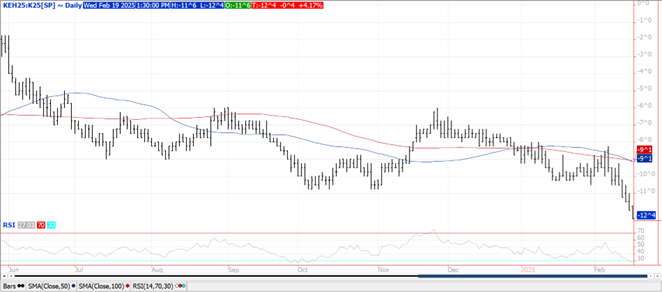

WHEAT

Prices were sharply lower today however managed to bounce a bit off session lows. Chicago and KC led the declines down $.10-$.13 while MGEX was down $.07. Concern of damaging cold for US winter wheat seemed to have greatly diminished. While temperatures dipped to sub-zero readings as far south as the TX panhandle, much of the winter wheat growing areas were insulated from the potential damaging cold with the snow cover. The TX and OK panhandles along with SW corner of KS are the most vulnerable to some winterkill. The Mch-25 contracts for both CGO and KC broke support at yesterday’s lows while new crop July-25 futures held above yesterday’s low at the close. Nearby spreads also recorded new lows. While speculative traders were actively buying wheat yesterday, open interest fell just over 7k contracts in CGO while plunging nearly 13k in KC suggesting yesterday’s trade was short covering in nature. It will be months before the true extend of any damage to the US winter wheat crop is shown. The lowest offer for Bangladesh’s 50k mt tender for wheat was just over $295/mt CF, no purchase has been finalized. Winter wheat conditions in TX fell 3% to 33% G/E. The percentage of the crop rated fair also fell 3% while poor increased 6%.

Charts provided by QST.

>>See more market commentary here.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.