Written Commentary

CORN

Prices were $.03-$.06 higher today led by old crop. Yesterday’s pullback over disappointment US stocks were cut trimmed was short lived. Spreads were steady to slightly firmer as we near the completion of the Goldman roll. Mch-25 rejected trade into new lows for the week. The USDA announced the sale of 130k mt (5 mil. bu.) of corn to an unknown buyer. Ethanol production slipped to 1,082 tbd, or 318 mil. gallons, down from 327 mil. the previous week and steady from YA. Production was at the low end of expectations. There was 109 mil. bu. used in the production process, or 15.5 mil. bu. per day, above the 14.9 needed to reach the USDA forecast of 5.50 bil. bu. In the MY to date there has been 2.450 bil. bu. used, or 15.3 mbd, an annualized pace of 5.588 bil. Ethanol stocks fell to 25.7 mil. barrels, below expectations, and below YA at 25.8 mb. As expected, the USDA made no change to their corn usage est. in yesterday’s WASDE report. Implied gasoline usage last week jumped 3% to 8.576 mil. barrels per day and was up 5% YOY. Export sales tomorrow are expected to range from 32-66 mil. bu. Although global stocks were cut 3 mmt yesterday, all the declines came from China. Stocks among major exporting countries held steady at 7.6% of usage, a 4 year low. Good demand should keep spot corn in a $4.70-$5.10 range. A breakout of this range will likely be determined how large Brazil’s 2nd crop shapes up.

SOYBEANS

Prices were lower across the complex today with beans $.12-$.16 lower also led by old crop, meal was down $2-$3 while oil was off 45-55 points. Mch-25 beans made a new low for the month however held support just above the 100 day MA at $10.23 ¼. Nearby bean spreads traded out to new lows. Mch-25 meal traded to its lowest level in 2 months with next support is the contract low at $285.10. Next support for Mch-25 oil is LW’s low at 44.64. Spot board crush margins did rebound $.05 today to $1.21 ½ bu., matching the higher for the month, while bean oil PV held steady at 43.7%. The USDA announced the sale of 120k mt (4.4 mil. bu.) of soybeans to an unknown buyer. A much more active weather pattern is expected across Argentina over the 2nd half of Feb. with several opportunities for rain. Along with cooler temperatures, crops ratings and yield expectations should level off, however some irreversible damage from January heat and dryness will still be felt. In Brazil an above normal precipitation pattern is expected for the most southern state of RGDS. Much of the central and center south region including MGDS, Parana and Sao Paulo will see a dryer pattern allowing bean harvest and 2nd crop corn plantings to accelerate as we hit mid-Feb. The USDA’s failure to increase soybean production in Brazil (holding at 169 mmt) didn’t stop the market from discounting a crop above 170 mmt. ABIOVE kept their production forecast unchanged at 171.7 mmt and exports at 106.1 mmt. They did however raise their crush forecast .4 mmt to 57.5 mmt, vs. the USDA’s est. of 56 mmt. Conab will release their updated Brazilian production est. tomorrow. Export sales tomorrow are expected to range from 10-30 mil. bu. for beans, 200-600k tons of meal, and 0-25k tons of oil. Stocks among global soybean exporters slipped just over 1% to 19.6% of usage

WHEAT

Prices were $.01-$.04 lower across all 3 classes today with MGEX leading the declines. Mch-25 Chicago held support just above the 100 day MA at $5.71 ¼. Mch-25 KC rejected early trade above $6.00. The Mch wheat/corn spread traded to a fresh 2 month high in early trade only to collapse closing down $.09 at $.84. Overnight and morning snow across KS and NE should provide a protective layer of snow ahead of this weekend’s frigid temperatures. Similar story in the Black Sea region. Major Feedmill Group reportedly purchased 115k mt of Australian wheat around $265/mt CF. Japan’s Ag. Ministry is seeking 124k mt of US, Canadian or Australian wheat in a tender closing tomorrow. Algeria has reportedly bought between 550-600k mt of milling wheat with prices ranging from $262-$264/mt CF. Wire services are reporting at midday that Pres. Trump spoke via phone with Russian Pres. Putin on a number of issues including the war with Ukraine, the middle east, Energy and AI. Export sales tomorrow are expected to range from 8-22 mil. bu. While global wheat stocks declined just over 1 mmt in yesterday’s WASDE report, this was entirely due to a 3 mmt drop in China. Stocks among global exporters actually rose to 14.1% of use, up from 13.4% in January.

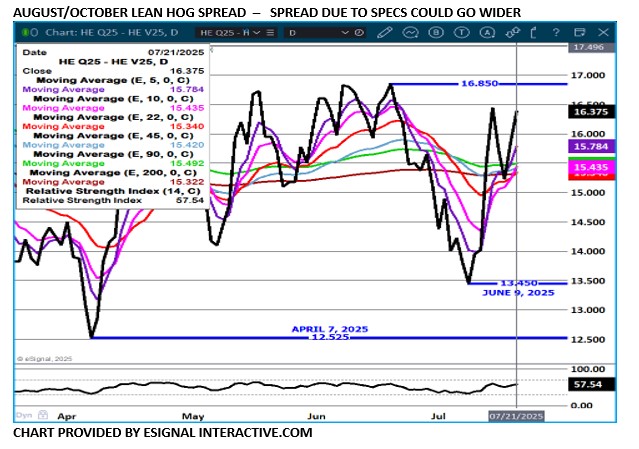

Charts provided by QST.

>>See more market commentary here.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.