Written Commentary

CORN

Prices finished near session lows down $.06-$.07 ½ on old crop while down only $.01 on new crop. Spreads widened with today being day 3 of the Goldman roll, 2 days left. Mch/May traded out to a new low at $.14 bu. Despite today’s weakness Mch-25 held above yesterday’s low. If violated this may open the door for a test of the February low at $4.72 ½ as speculative traders pare back on recently added long positions. The USDA left ending stocks unchanged at 1.540 bil. Bu. vs. expectations for a 15 mil. bu. drop. The Ave. US Farm Price was raised $.10 to $4.35 bu. Global stocks were cut 3 mmt to 290.3 mmt, below the range of estimates. Production in both Argentina and Brazil was cut 1 mmt. Chinese imports were cut 3 mmt to only 10 mmt. Once again spot Mch-25 stopped just shy of the $5 level in early strength. The EIA set to release weekly ethanol production tomorrow at 9:30 AM.

SOYBEANS

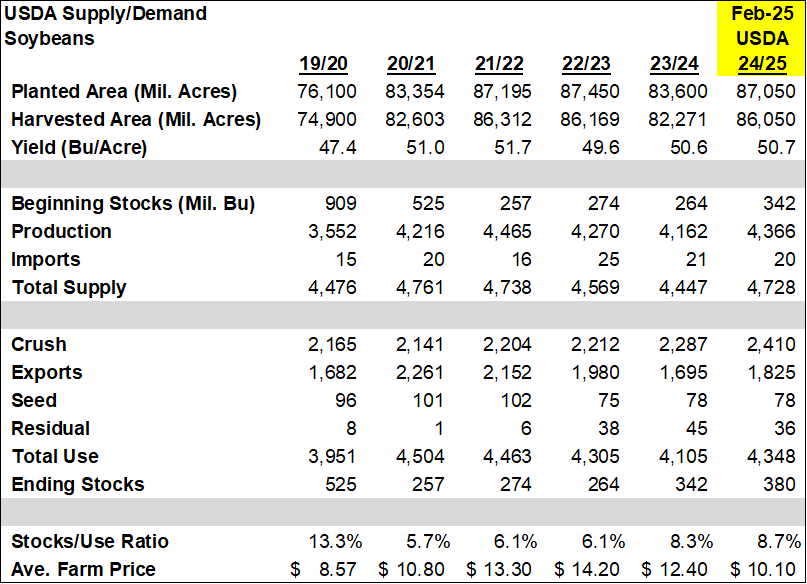

Prices were mixed across the complex with beans down $.02-$.06 led by old crop, meal was off $3-$4 while bean oil rebounded 35-40 points. Bean and meal spreads weakened while oil spreads were mixed. Mch-25 beans had an outside day however closed within yesterday’s range. 1st support below the market is LW’s low at $10.31 ¾ followed by the 100 day MA at $10.23 ½. Mch-25 meal held support just above LW’s low at $295.30. The USDA left ending stocks unchanged at 380 mil. Bu. in line with expectations. The Ave. US Farm Price was lowered $.10 to $10.10 bu. The balance sheet on products was also left unchanged. Global stocks were cut 4 mmt to 124.3 mmt, below the range of estimates as Argentine production was cut 3 mmt and Paraguay cut .5 mmt. Production in Brazil was surprisingly left unchanged at 169 mmt. Chinese imports were cut 2.5 mmt to 8 mmt. Mch-25 can’t seem to get too far away from $10.50. Bean oil outperforming meal drawing support from higher palm oil. Little change with SA weather as extreme heat is expected to impact central and northern Argentina a few more days before scattered showers are expected to provide relief. Additional rains moved across northern Buenos Aires overnight. A much more active weather pattern is expected the 2nd half of Feb. with several opportunities for rain. In Brazil an above normal precipitation pattern is expected in the deep south in RGDS and in the far north in northern Mato Grosso however much of the central portion of the country, including MGDS, Parana and Sao Paulo will see a much dryer pattern allowing bean harvest and 2nd crop corn plantings to accelerate as we hit mid-Feb.

WHEAT

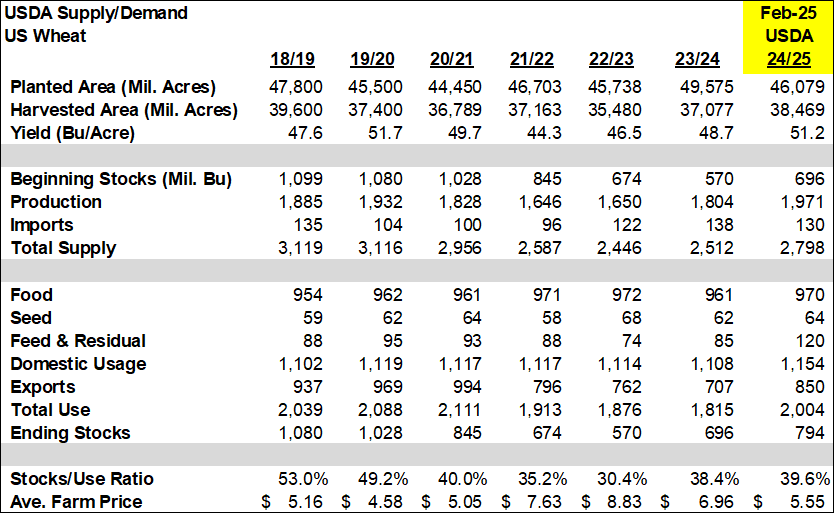

Prices finished $.02 1/2-$.07 lower with MGEX futures leading the declines. An active jet stream in the US will bring a healthy mix of rain, sleet and snow for much of the nation’s midsection this week ahead of a frigid outbreak this upcoming Holiday weekend. The USDA cut ending stocks cut 4 mil. bu. to 794 mil. due to increased usage for food. They kept the Ave. farm price unchanged at $5.55 bu., $1.40 below the Ave. price from the 23/24 MY. Global stocks were cut 1.2 mmt to 257.6 mmt vs. expectation for no change. Global inventories remain at a 9 year low. Russian and Ukrainian exports were trimmed .5 mmt each while they were lower 1 mmt in the EU. Chinese imports cut 2.5 mmt to 8 mmt. The USDA made no changes to Australian production, perhaps waiting for an update next month from ABARE. Argentine production was raised only .2 mmt to 17.7 mmt. Tighter global supplies should continue to bode well for US exports. IKAR lowered their Russian production forecast for 2025 2 mmt to 82 mmt.

Charts provided by QST.

>>See more market commentary here.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.