Written Commentary

CORN

Prices range from down $.04 in old crop to up $.02 in new crop. Next support for July-25 is the 50 day MA at $4.83 ½. Inside trade for Dec-25. The July/Dec spread broke $.05 ½ today to just over $.25 bu. I’d be a buyer here looking for a move back up to $.40. The USDA announced the sale of 110k mt (4.3 mil.) of corn to Portugal. Healthy rains will continue to move across key 2nd crop corn areas in WC and SC Brazil keeping production prospects elevated. Lighter amounts in the far southern state of RGDS. US corn plantings advanced 2% LW to 4% complete, below the 6% pace from YA and the 5-year Ave. of 5%. Better than expected progress in AR with plantings advancing 11% to 42% complete, well above the historical average of 30%. Most noted delays in KY and TN with plantings at only 3% and 7% respectively. As of last Tues. April 8th, CFTC data shows money managers have shed just over 310k contracts from their long position over the past 2 months down to just under 54k contracts. Tomorrow’s EIA report is expected to show ethanol production range from 275-310 mil. gallons last week, vs. 300 mil. the previous week.

SOYBEANS

The soybean complex was mixed today with beans ranging from $.06 lower in spot May to up $.01 in new crop. Meal was $2-$3 lower while oil jumped a full penny. Bean and meal spreads weakened while oil spreads firmed up. July-25 beans held support above its 100 day MA at $10.38. July-25 meal for now rejected trade below $300 per ton. Early strength in bean oil likely from the oilseed industry group Abiove suggesting Brazil reconsider raising its biodiesel blend rate 1% to 15% with the global decline in vegetable oil prices. This measure was shot down by their national energy council in Feb-25 amid fears it would push up food costs. Argentina’s exchange rate overhaul that resulted in a 12% decline in their Peso has so far not triggered heavy farmer selling. Except for southern and far western Argentina, dry conditions will prevail for much of the next week to 10 days, allowing crops to dry down and harvest to accelerate after a slow start. US plantings were reported at 2% in line with the 5-year Ave. and just below YA at 3%. NOPA members crushed only 194.6 mil. bu. in Mch-25, below expectations of 197.6 mil. and below the 196.4 mil. bu. processed in Mch-24. Implied census crush for March would fall around 206 mil. bu. bringing YTD crush to 1.438 bil. up 4.7% from YA, vs. the recently revised USDA forecast of up 5.8%. Oil stocks fell to 1.498 bil. lbs., just below the 1.503 bil. at the end of Feb., however well below expectations of 1.62 bil. NOPA member were holding 1.85 bil. lbs. of oil at the end of Mch-24. Spot board crush margins were up $.09 ½ today to $1.32 bu., rebounding nicely after the lower than expected crush. Bean oil PV rebounded to 44.6%.

WHEAT

Prices were down $.02-$.06 across all 3 classes today with SRW (CGO) futures the downside leader. Forecasts for improved rains across key growing areas of the Southern plains continue to weigh on wheat valuations. July-25 KC was able to hold support above this month’s low at $5.62 ¾. MGEX July-25 dipped below support at its 100 day MA at $6.18 ½. US winter wheat ratings slipped 1% to 47% G/E, however poor/VP also fell 2% to 19%. Fair increased by 3%. 8% of the crop is headed, in line with the 5-year average however below the 10% pace from YA. Spring wheat plantings have reached 7%, also in line with the 5-year average and above the 6% pace from YA. The CBOT has declared Force Majeure along the Ohio River as high water levels have prevented commercial handlers from loading out grain. The BAGE projects Argentine wheat production at 20.5 mmt, a 4 year high and above the USDA 24/25 forecast at 18.5 mmt.

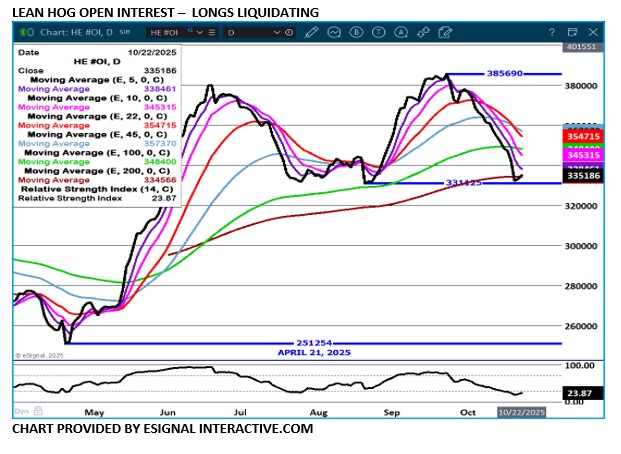

Charts provided by QST.

>>See more market commentary here.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.