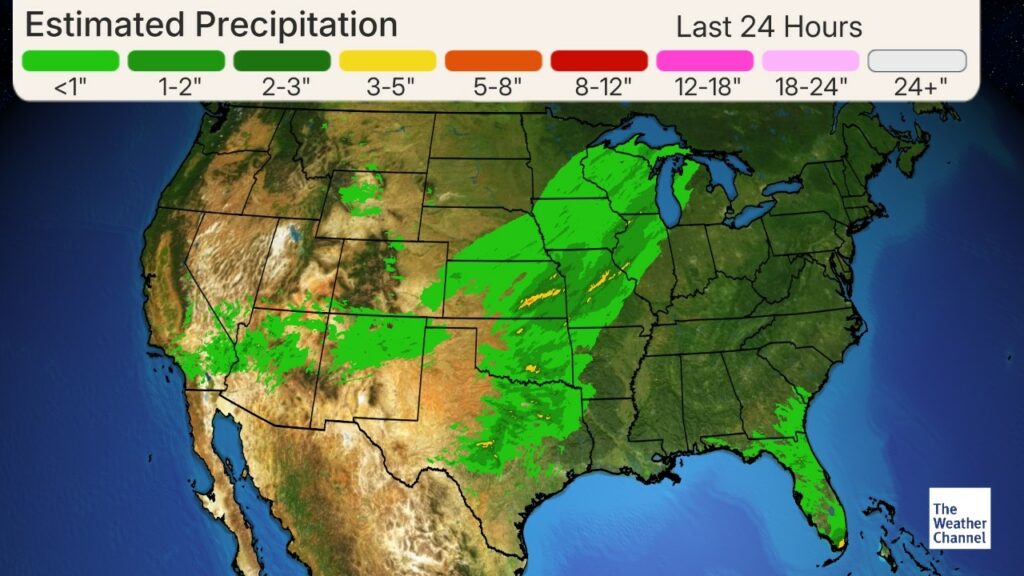

Geopolitics: Chinese leader Xi Jingping is “very tough and extremely hard to make a deal with” according to posts from President Trump overnight. The two leaders could talk as soon as this week. The China’s foreign minister Wang Yi has asked the US to meet China halfway. We are nearly 1/3 of the way through the 90-day pause that was established on May 12th. Aside from trade, the two countries are addressing fentanyl and illegal immigration issues as well. Macroeconomics: The ISM Manufacturing PMI report on Monday showed the US manufacturing sector is contracting. For the last 31 Manufacturing PMI prints ONLY 3 reports have shown slight expansion. This is the longest stretch of contraction in my lifetime, more so than the dot com crash, the 2008 financial crisis and COVID. US manufacturing started to decline rapidly from it’s peak in April 2021, went negative in November 2022 and has basically remained in contraction ever since. Even if US companies could manufacture goods here cheaper, I don’t think American’s care if the box says “made in USA”. The JOLTS job report yesterday came in better than expected, but we are still in a down trend from the peak openings in May of 2022. The report found 7.39M job openings vs. the 7.11M expected and the 7.20M they reported last month. We have the ISM services PMI report out later today and another major job (unemployment and earnings) report out on Friday morning. Ag Fundamentals: Normal to above normal rainfall would normally be the major story today, but the market wants to focus on the potential trade agreement between the US and China and the possibility some areas of the corn belt did not get all their intended acres planted. Some of that seed will make its way back to the dealer if it’s not in the ground in time to establish crop insurance requirements. These missed corn acres are likely planted with beans in the next few weeks. Most of these acres are in the eastern corn belt,, southern Illinois and parts of Iowa that received too much rain. Ethanol numbers out later today and export sales out tomorrow morning. The next WASDE report is just over a week away, on Thursday June 12th. Not hearing any major shifts in the estimates. If we see lower ethanol production today, we may see reductions in corn usages next week, but exports remains strong and I doubt they change the acres planted until the July report.

Export & World News

Algeria is looking to purchase up to 240K Mt of animal feed corn. Bangladesh is in the market to purchase up to 50K MT of milling wheat. China’s customs approve imports of Russian coarse ground wheat, rye flour.

Malaysian palm oil futures were up 15 ringgit, at 3949.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.