Written Commentary

by market analysts Stephen Platt and Mike McElroy

Price Overview

WTI Crude oil prices fell sharply settling off 3.04 at 70.77. The weakness appeared to be in response to news that Saudi Arabia had cut the Official Selling Price of its Arab Light crude to Asian customers to its lowest level in 27 months by over $2 a barrel from January to 1.50 a barrel over Dubai quotes. Although a price cut was generally expected due to weak demand for Saudi wet barrels and inventory increases in Asia, the size of the cut raised questions over how effective the most recent OPEC agreement is at supporting prices. Production increases by some OPEC members such as Nigeria and Iraq along with continued expansion in output levels by non-OPEC members including the US, Guyana, Canada and Brazil has cut into demand for Saudi cargoes limiting the effectiveness of OPEC+ production cuts. The Non-OPEC increases also continues to weigh on OPEC+ market share which has fallen to levels not seen since late 2020. The situation has been exacerbated by an increase in Iranian availability which has also been competing with Saudi cargoes in Asia and particularly China. With spring refinery maintenance beginning to get underway, refinery throughput is unlikely to get better given the high stock in Asia and uncertain demand prospects in China due to the economic outlook.

The market will continue to be watching for additional supply threats in the Mid East but will remain cautious reflecting other macro influences related to the ability of OPEC to further support prices and the appearance that demand growth will continue to soften, particularly in China as EVs gain a larger market share. Production growth in areas outside of OPEC+ also is providing a headwind to values. Overall, stocks in 2024 look poised to build modestly limiting upside initiatives to around the 76 level For the most part some support should be apparent below 70.00 given the force majeure in Libya at the Sharara field, prospective action by OPEC in response to lower prices and the risk premium associated with Mid East tension. The appearance the US is interested in rebuilding the Strategic Petroleum Reserve also should provide support. For the most part, we see values still holding to a consolidative pattern between 72 and 76 basis February in the coming weeks.

The Doe report is expected to show crude inventories fell 1.2 mb, gasoline +4.0 and distillate +4.0. Refineryt utilization is expected -1.0 at 92.5 percent.

Natural Gas

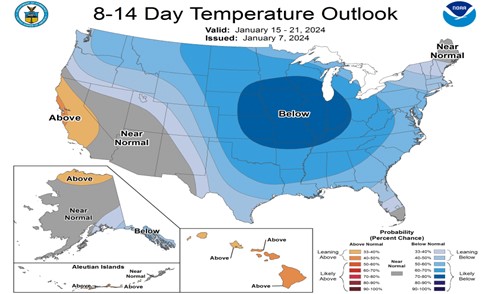

The market came under substantial selling pressure early falling over 20 cents basis Feb Nat Gas before recovering to show a strong gain of 8,7 in Feb while the back months showed modest losses. Early pressure on values reflected a weaker crude oil market along with the appearance that above normal storage levels still suggest adequate supply availability in the months ahead. Nevertheless, renewed short-covering and fresh buying developed on the prospect for below normal temps into the Martin Luther King holiday along with the prospect for Nat Gas production, which has fallen sharply, might be influenced by the colder than normal temperatures due to freeze offs at producing wells. For now, the lower production levels and good demand due to strong exports to Mexico and strong LNG shipments should help underpin values particularly with the colder than normal temps forecast in the 8-14 day forecasts. Given the prospect for a larger than normal withdrawal in this weeks EIA report of over 110 bcf, underlying support to values should be maintained with overhead resistance above the 3.05-3.10 level basis Feb due to the large storage overhang on the upside and the approaching end of winter for the back months.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.