Written Commentary

by market analysts Stephen Platt and Mike McElroy

Price Overview

WTI Crude oil prices strengthened to settle +1.62 at 73.81 on short-covering ahead of the weekend on continued concern Mid-East hostilities might broaden to include Hezbollah and Lebanon. Maersk announced that due to ongoing attacks against shipping in the Red Sea they would be diverting shipping from the Red Sea for the foreseeable future. The market might also have responded to the stronger than expected jobs report which suggested the economy continues to perform better than expected helping to assuage demand concerns following yesterdays DOE report and the larger than expected build in both gasoline and distillate stocks reflecting weaker disappearance levels.

The DOE report showed crude stocks declining by a larger than expected 5.5 mb while gasoline inventories rose 10.9 mb and distillate increased by 10.1 mb with total stocks of crude and products rising by 8.9 mb. Refinery utilization was indicated at 93.5 percent an increase of .2 percent. Net export levels of crude and products totalled 2.9 mb compared to 3.0 mb last week. Total disappearance levels slowed dramatically falling to 19.1 mb compared to 21.4 last week. Gasoline disappearance fell to 8.0 mb/d from 9.2 mb in the prior week while distillate disappearance fell to 2.7 mb from 4 mb in the prior week. We would expect a recovery in these disappearance levels as we move into January and commuter traffic picks up following the holiday.

The market will be looking for additional supply threats in the Mid_East but will remain cautious reflecting other macro influences related to the ability of OPEC to further support prices and the appearance that demand growth will continue to soften, particularly in China as EVs gain a larger market share. Production growth in areas outside of OPEC+ also is providing a headwind to values. The uncertain environment and fear of a broader conflict should limit selloffs despite weaker consumption trends on a seasonal and outright basis, suggesting a consolidative trend between 72 and 76 basis February might be apparent in the coming weeks. Signs that OPEC+ is taking more coordinated action to support values or an expansion in Red Sea hostilities could carry values up toward the 78-79 range.

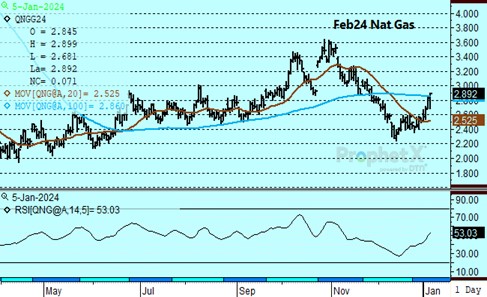

Natural Gas

The market saw strong follow-through yesterday, gaining over 15 cents despite the storage report that showed a 14 bcf draw when expectations had been near 40. The bulls continued to be emboldened by colder forecasts into the middle of January. Today’s action saw some exhaustion of the buying interest as prices retrenched early in the session, but strength returned into the close as February contract ended 7.2 cents higher at 2.893. The next upside target is the psychological 3 dollar area which would also mark a 50 percent retracement of the early winter break. A push above that area will be difficult considering the current storage situation, strong production and short term nature of the impending cold stretch. With RSI elevated, the market could retrench significantly at any time, with support at 2.68 followed by the 2.57-2.60 range. 7.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.