Written Commentary

by market analysts Stephen Platt and Mike McElroy

Price Overview

Crude oil attracted good buying interest, settling 1.09 higher at 78.26 basis December. Strength came from the OPEC Monthly report downplaying consumption concerns and suggesting that fundamentals remain strong. It attributed recent weakness in prices to speculative interests. Support was also linked to reports the US Treasury is investigating 30 ship managers for violations of Western sanctions on Russian oil, which helped offset reports the Turkish pipeline could open to Kurdish exports in three days.

The OPEC Monthly report revised 2023 demand forecasts marginally higher to 2.5 mb/d as Chinese demand outpaced declines from the OECD. On the supply side the growth forecast was revised up to 1.8 mb/d with the main drivers being the US, Brazil, Kazakhstan, Guyana, Mexico, and China. The report indicated that countries participating in the Declaration of Cooperation will maintain their commitment to achieve and sustain a stable market in line with the decision to extend the agreement until the end of 2024 in combination with the Saudi and Russian voluntary cuts of 1.3 mb/d which also could be extended into 2024. Forecasts by the IEA and OPEC are diverging, with OPEC maintaining an optimistic view, estimating demand growth rising 2.25 mb/d in 2024 while the IEA is expecting an increase of only 880 tb/d.

Look for crude values to retest the 80-81 area. Weakness to the Chinese economy remains in the background although crude oil import quotas being increased to independent refiners remains a distinct possibility, allowing the government to support export levels of all goods, which have been weak. OPEC+ policy is also being watched closely as Iraq’s oil ministry indicated it was committed to the agreement two weeks ahead of a key meeting of the producer group on November 26th. Better supply availability from the Middle East has been noted due to a seasonal decline in domestic demand typical in October-November as weather cools. Demand in other areas should begin to recover as refinery utilization rises following seasonal maintenance in developed countries. Market participants will be watching the delayed DOE report to see if it validates the sharp increase in inventories reported by the API last week. Crude stocks are still low and are drawn down in the months ahead on winter’s arrival and refinery utilization increases to meet demand for middle distillates. Key to further strength will be Saudi policy and production trends in and outside OPEC.

The DOE will be releasing reports for November 3rd and 10th this week. In the latest reporting period crude inventories are expected to have increased by 1.4 mb, with distillates indicated lower by 1.8 and gasoline estimated higher by 1.3 mb. Refinery utilization is expected to be up .6 to 86 percent.

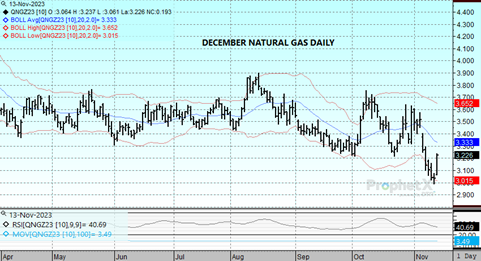

Natural Gas

Weather model updates over the weekend signaled increased demand expectations and the market ran with the news to gain over 16 cents, settling at 3.197 on the December contract. Most of the cooling was back end loaded, so revisions will be watched closely to see that the trends are maintained. LNG flows assisted the rebound, coming in near 15 bcf over the weekend, but were offset by continued strong production. Short covering also contributed to the reversal following last weeks substantial sell-off. Despite the cooler forecasts, expectations have only recovered to normal levels in the back end of the outlook. A continuation and intensification of the cold trend will be needed to maintain the recovery. Resistance will surface at the 9 and 20-day moving averages at 3.25 and 3.33 respectively, with the gap from last week at 3.452 the target if those levels can be taken out. Lower trade will find 3.20 and 3.10 offering minor support, with 3 dollars the key level that needs to be maintained to avoid another leg down.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.