Written Commentary

by market analysts Stephen Platt and Mike McElroy

Price Overview

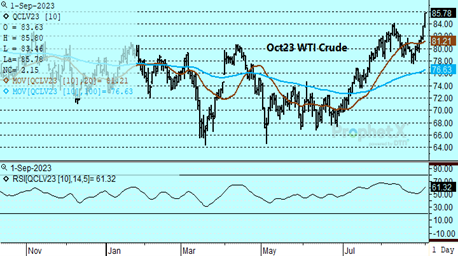

The crude oil traded firm with ULSD continuing to lag the up move. The underlying support to the complex was linked to concern over declining stock levels in crude, and growing anticipation that Saudi Arabia and Russia will carry over their voluntary production cuts into October. Economic concerns in China and Europe appeared to ease following reports that a downturn in euro zone manufacturing had stabilized last month as their Purchasing Manager’s Index rose to a three-month high of 43.5 in August compared to 42.7 in July. While a reading below 50 still indicates a contraction in activity, the improvement does suggest some stabilization despite higher European interest rates. In China, the Caixin PMI rose unexpectedly following the official survey releases yesterday showing a contraction giving some comfort that the economy has begun to stabilize and that official efforts to stimulate the economy are beginning to work. In the US, the payrolls report and rise in unemployment rate has helped soften concern over further interest rate hikes helping limit further strength in the dollar.

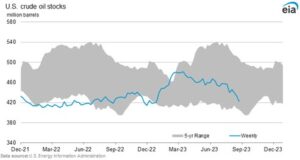

The key consideration next week will be the level of US and global inventories. US crude stocks remain at historically low levels and the recent decline in Cushing stocks has heightened its importance. Progress has been made in expanding production and availability from both non-OPEC and OPEC producers. However, it still appears to be short of demand in the fourth quarter and with the prospect of voluntary cuts of close to 1.3 mb/d by Saudi Arabia and Russia further declines are likely. Prospects for 2024 point to a more balanced supply/demand environment which could ease upside pressures. In the absence of additional SPR sales, further declines in commercial crude stocks are likely without the Saudis backing off from their 1 mb/d production cut, with today’s breakout above 84.00 likely signaling a move toward the 88-90 level basis October.

Natural Gas

After reaching an intraday high at 2.865 early in yesterday’s session, prices have seen minor weakening, ending the week at 2.765 basis October. Hurricane Idalia ran its course through Florida with minimal effects on gas infrastructure and less demand destruction than expected, resulting in a neutral effect on values. The pullback in production to under 101 bcf/d over the second half of the week was only partially attributed to Gulf of Mexico evacuations, as trade continues to look for output to show signs of retreating in response to the steady drop in rigs. Weather remains supportive with the first half of September forecast to produce record demand for this time of year. Australian LNG worker strikes remain a background support as unions have authorized action starting on September 7th, but those moves are likely to initially be minor. Yesterday’s storage report showed a higher than expected 32 bcf build as prices swung in both directions following the release before ultimately turning lower. The 2.87 level held up yesterday and remains key resistance to upside momentum. A settlement through there would signal a test of 3 dollars. A move lower will find minor support at 2.75 and then at the convergence of the 9 and 100-day moving averages currently at 2.69.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.