Written Commentary

by market analysts Stephen Platt and Mike McElroy

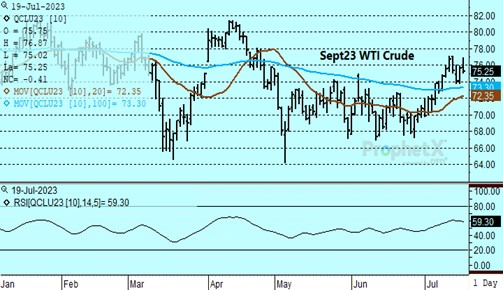

Price Overview

Prices failed to follow-through on early strength, with crude values losing 40 cents to settle at 75.35. Early support was traced to ideas that the Chinese economy might not be as weak as previously thought as authorities focus on reviving consumer demand. In addition, tightening availability of Russian shipments given recent strengthening in differentials to levels above the price ceiling raised concerns. In the background was the EIA forecast for monthly WTI crude prices advancing up toward the 80.00 level on persistent inventory drawdowns as demand exceeds supply. They indicated that expected production cuts from OPEC members and increasing consumption will lead to an inventory drawdown averaging .4 mb/d between July 2023 and the end of 2024.

The DOE report failed to live up to expectations for a crude draw of 2.3 mb as inventories fell by .7 mb despite the absence of sales from the SPR. Cushing stocks dropped to 38.3 mb, a decline of 1.9, which was slightly supportive. Gasoline stocks fell 1.1 against expectations for a decline of 2.1, while distillates were unchanged. Total stocks of crude and products fell 1.1 mb. Refinery utilization rose to 94.3 percent from 93.76 last week. Total disappearance rose to 20.8 led by strong gains in distillate and other oils from the prior week. Net export levels of crude and products remained light at 1.3 mb.

Despite the constructive bias from the EIA, downward revisions in global demand will provide hesitancy on the long side from the 76-77 level basis September crude. In addition, caution is likely ahead of the end of the month awaiting signs of whether the voluntary production cuts by Saudi Arabia will be extended into September. We expect stocks to decline in the second half of the year, but due to consumption issues in China, good availability from Iran, and issues with payments from India to Russia, the decline might not be as dramatic as currently predicted. Near term look for a retracement toward the 72.00-73.00 area basis September crude as demand prospects tied to the economy in the US and China are watched closely.

Natural Gas

The current heat wave across the US has underpinned the market to start the week, but has been unable to convincingly push prices higher. Yesterday’s 11 cent gains were followed by two-sided trade today with the active September ending 3.3 cent lower at 2.585. Fundamental inputs were neutral today, with early signs of a pullback in production to under 100 bcf/d offset by steadily improving LNG flows. Tomorrow’s storage report is expected to show a 48 bcf injection, slightly above the 5-year average build of 45 as inventories look to remain elevated even as extreme heat is being experienced across much of the country. Despite the negative bias, the market has managed to settle above the 9-day moving average for the past two sessions, which is a minor positive development. With storage levels likely to be drawn down in the coming weeks, the 100-day moving average currently near 2.68 will be the next upside target if bulls want to maintain the recent recovery. Failure to maintain upside momentum will find initial support near 2.68 and then at 2.50.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.