Written Commentary

by market analysts Stephen Platt and Mike McElroy

Price Overview

Crude oil prices were initially on the defensive, falling to a low of 67.35 basis August before recovering to settle at 69.16 for a decline of 35 cents. Strength to the dollar, interest rate increases in the UK, and the potential for further rate hikes in the US to calm inflationary trends continued to provide a headwind to values. Support at the lower levels was based on the possibility of inventory declines as we move into the summer and Asian demand improves.

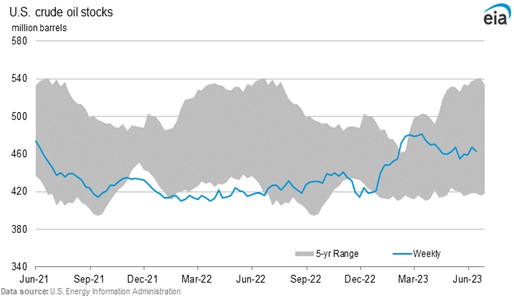

The DOE report yesterday showed commercial crude inventories falling by 3.8 mb despite an SPR draw of 1.7. Gasoline and distillate stocks rose by .5 and .4 mb respectively. A surge in exports of crude and a decline in imports precipitated the draw in crude inventories despite a decline in refinery utilization to 93.1 percent from 93.7 last week. Total disappearance of products improved to 20.9 mb with gasoline at 9.4 compared to 9.2 the prior week. Distillate disappearance rose to 4 mb from 3.6. Total exports of crude and products were 2 mb compared to 1.2 previously.

A stable outlook from OPEC, an expansion in oil demand, and marginal increases in supply for the remainder of the year should provide support to values. Steady growth in demand from key non-OECD consumers such as India and China should offset the lackluster demand in OECD countries. Supplies from Russia and Iran will also remain a focus given reports of good availability and the possible reopening of discussions between the US and Iran aimed at limiting their nuclear program. Saudi efforts to support values with additional production cuts could also help limit downside pressures. Look for stock declines to gain momentum with support in the 67-68 range. An accommodative monetary policy in China and strength to India’s economy will help tighten inventory levels and underpin valuations later this summer with potential to push values toward the 75-76 level basis prompt crude.

Natural Gas

After some back and forth action the market managed to press higher and maintain recent upside momentum. The August contract added 13.9 cents today to end the week at 2.843. Yesterday’s storage report came in on the high side with a 95 bcf build, and the market reacted quickly, losing 10 cents after the release, but gained it all back by the end of the session. Support continued to be offered by intense South Central heat that is likely to set demand records in Texas in the coming days along with hopes for improving demand from an expected increase in temperatures across a larger swath of the US early next week. Production dropped below 101 bcf over the last three days, adding background support. A slip in LNG flows back below 11 bcf/d over the last two days surprised the market, as Sabine Pass saw further reductions, but the selling pressure was short lived as trade continues to assume an imminent end of seasonal maintenance. The strong close and settlement well through the 100-day moving average could portend follow-through action early next week if forecasts can remain warm. The May high at 2.885, which also comes in near a 50 percent retracement of the break since early March, would be the next target on the upside, with resistance beyond there at 3 dollars. The 100-day moving average near 2.77 now offers initial support without much below there until the 2.61 area.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.