Written Commentary

Price Overview

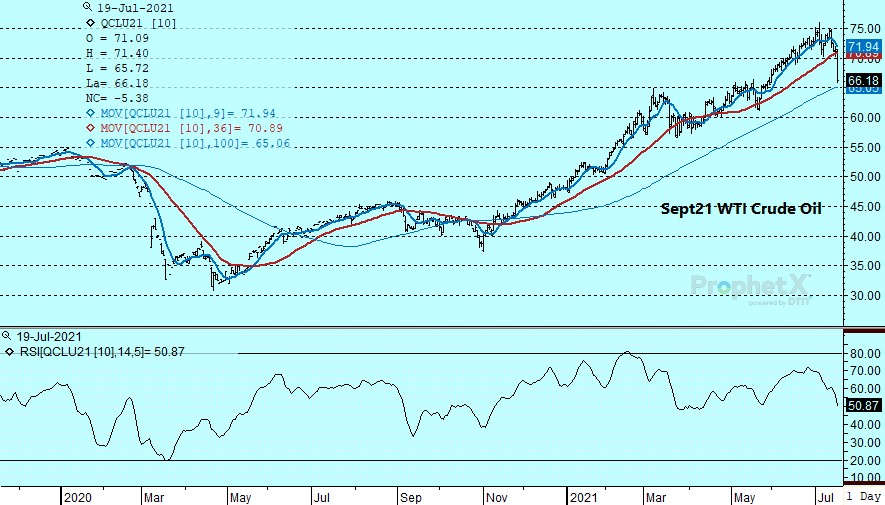

The petroleum complex traded sharply lower, falling over $5.00 per barrel following news that OPEC+ had agreed over the weekend to end output cuts in late 2022. The deal allows the UAE an increase in its baseline production to 3.5 mb/d from 3.168 currently. The deal will allow production to increase for OPEC+ by 400 tb/d per month for a total of 2 mb/d from August to December of 2021. They aim to fully phase out cuts by around September 2022. Along with the increase in baseline for the UAE, the agreement also stipulates increases for both Saudi Arabia and Russia by 500 tb/d beginning in May of 2022, putting their baselines at 11 mb/d. Iraq and Kuwait also received adjustments in their quotas of 150 tb/d.

At face value the news did not seem as negative as the market suggested given the decline of over 5.00 in crude and the penetration of support near the 70.00 area basis September. Instead, other influence appeared to exacerbate the selloff including a sharp decline in equity values. Questions have developed over the pace of the global recovery given the rising infections from the Covid Delta variant. The idea that the recovery is uneven is evident by the slowing oil demand rates in the top importing region of Asia. The slow vaccination and rising infection rates appear to be reducing import levels for this key area, with Refinitiv Oil Research indicating that in July they will fall to 22.59 mb/d from 23.78 in June and 23.04 mb/d in May. On the plus side is the ability of OPEC+ to come up with an agreement which was in doubt following the early July meeting, as it still appears that they are a viable force but also suggests that they were not willing to hurt demand as WTI reached above the 75.00 area.

While the OPEC+ agreement eliminates some of the uncertainty over supplies, the production quotas still suggest a moderate inventory deficit will develop into the end of the year. How large these deficits become will remain a key consideration for the market. The strength of the OECD economies has been a bright spot but the uncertainty on how quickly a return-to-work progresses is being raised amid rising infection rates in some areas.

The DOE report on Wednesday should provide support. Expectations for another sharp decline in crude inventories of 4.2 mb and in gasoline of 1.4 is likely to limit selling interest, particularly against the 100-day average at 65.06 basis September. Resistance near 70.00 is likely to be formidable given the extent of the breakdown and uncertainty over the economic impact of the rise in infection rates.

Natural Gas

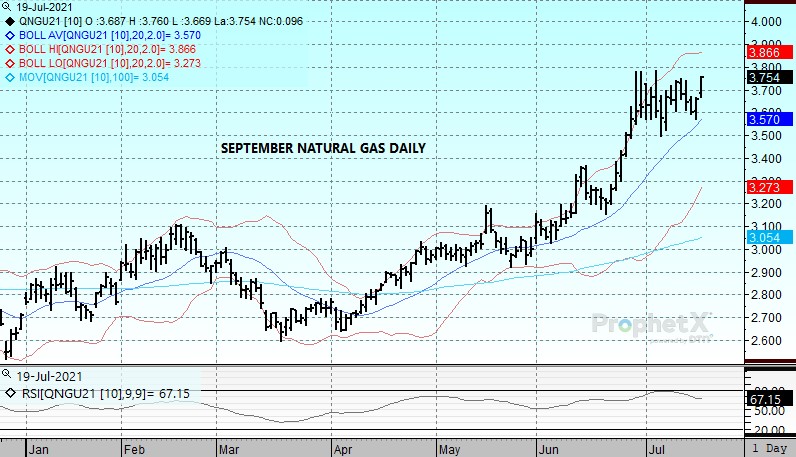

The natural gas seemed intent on trading higher today despite a lack of any decidedly bullish fundamental signals and a selloff in equity and commodity markets stemming from fears of the Delta variant spread. The September contract added 9 1/2 cents to end the the session at 3.754, a new high settlement. Forecast revision coming out of the weekend were slightly bullish, indicating increased CDD demand in the second half of the 15 day outlooks, but were countered by increasing production levels and a drop in LNG flows. In the background Mexican exports have continued to retreat, coming in at 6.2 this morning verses the 6.7 area a week ago. Overseas prices offered underlying support as they continue to press higher, which is supportive of LNG exports and has created a steady demand stream that the market has not experienced previously. If the warmup into the end of the month is maintained over the next few days, the highs near 3.80 will likely be tested soon, and if it ultimately materializes the 4.00 level remains a potential target as we move into August. Initial support now looks to be in the 3.66 area.

Charts Courtesy of DTN Prophet X, EIA, Reuters

The authors of this piece do currently maintain positions in the commodities mentioned within this report.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.